- Supply bottlenecks continue to disrupt import shipments

- Casting-grade scrap shortage persists in India

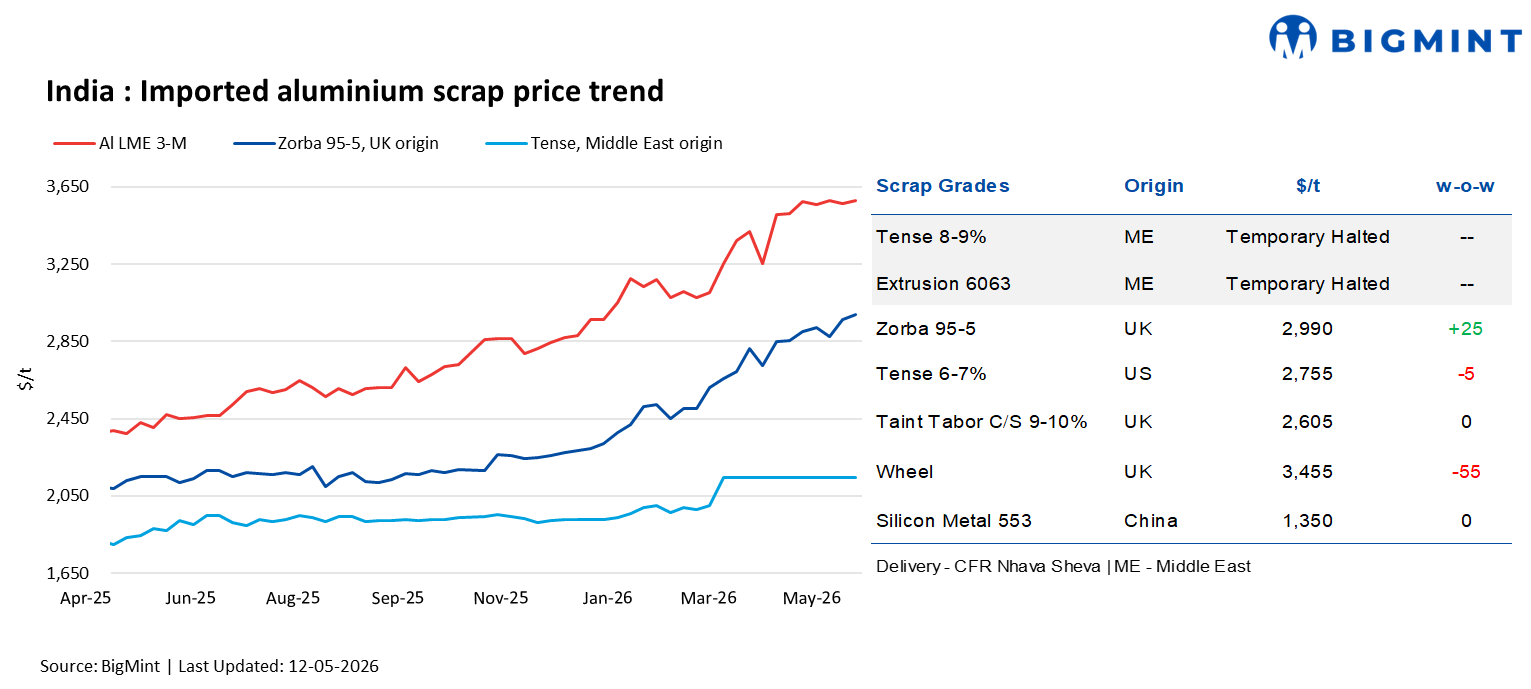

India’s imported aluminium scrap prices showed mixed trends w-o-w as of 12 May 2026, amid marginally higher London Metal Exchange (LME) aluminium prices and cautious spot market activity.

According to BigMint’s latest assessment for CFR Nhava Sheva deliveries, UK-origin zorba 95-5 scrap increased by $25/t w-o-w to $2,990/t from $2,965/t previously, supported by firm shredded scrap availability.

Meanwhile, US-origin tense 6-7% scrap declined marginally by $5/t w-o-w to $2,755/t from $2,760/t last week, reflecting balanced buying activity in the imported scrap market.

LME aluminium rises marginally w-o-w

Three-month aluminium prices on the London Metal Exchange (LME) increased marginally w-o-w, reaching $3,580/t on 12 May 2026, up by $17/t from $3,563/t on 5 May 2026. Prices declined during the middle of the week to $3,510/t on 7 May before recovering in subsequent sessions amid persistent supply concerns and declining exchange inventories.

Market sentiment remained supported by tightening visible stocks, continued declines in cancelled warrants, and growing concerns over supply disruptions linked to geopolitical tensions in the Middle East. Higher LME cash prices and narrowing near-term availability also reflected ongoing tightness in the physical aluminium market.

Meanwhile, LME aluminium inventories decreased by 6,950 t w-o-w to 355,775 t from 362,725 t over the same period, indicating continued stock drawdowns across exchange warehouses.

Market scenario

Imported aluminium scrap market sentiment remained subdued, with limited trading activity across regions despite a w-o-w increase in LME aluminium prices. Demand conditions stayed weak and uncertain, while domestic rates continued to remain firm amid tight market availability, preventing any significant correction in prices.

Buying activity remained cautious, with market participants largely postponing fresh procurement amid expectations of further price adjustments and continued uncertainty surrounding LME direction. Market participants expect market conditions to weaken further from June onwards as the broader impact of the ongoing geopolitical conflict begins to reflect more visibly on industrial demand and trade flows.

Supply-side disruptions and logistical bottlenecks continued to weigh on sentiment, particularly due to restricted cargo movements through the Strait of Hormuz, which tightened import availability. In the Middle East, heavy congestion at the Oman-UAE border disrupted physical cargo movement, especially for export shipments. While Jeddah-bound cargoes were reported to be moving relatively smoothly, Khorfakkan shipments remained significantly disrupted and unreliable, whereas Jebel Ali operations continued to remain offline.

On the domestic front, aluminium prices remained firm, while scrap availability stayed tight across both northern and southern India, especially for casting-grade Tense scrap amid acute supply shortages. Secondary producers continued to face procurement challenges, resulting in cautious buying behaviour and subdued operating rates across the industry.

Chinese silicon metal prices stable w-o-w

According to BigMint’s latest assessment, China-origin silicon metal 553 prices remained stable w-o-w at $1,350/t on a CFR Mundra basis as of 12 May 2026, amid balanced market activity and steady import offers.

Outlook

Imported aluminium scrap prices in India are likely to remain firm in the near term. Tight scrap availability, logistics disruptions, and firm LME prices may support the market, while cautious buying activity could limit sharp upside. Supply constraints are expected to keep downside risks limited.

Leave a Reply