- Holiday closures restrict global scrap flows

- Domestic tightness lifts casting scrap prices

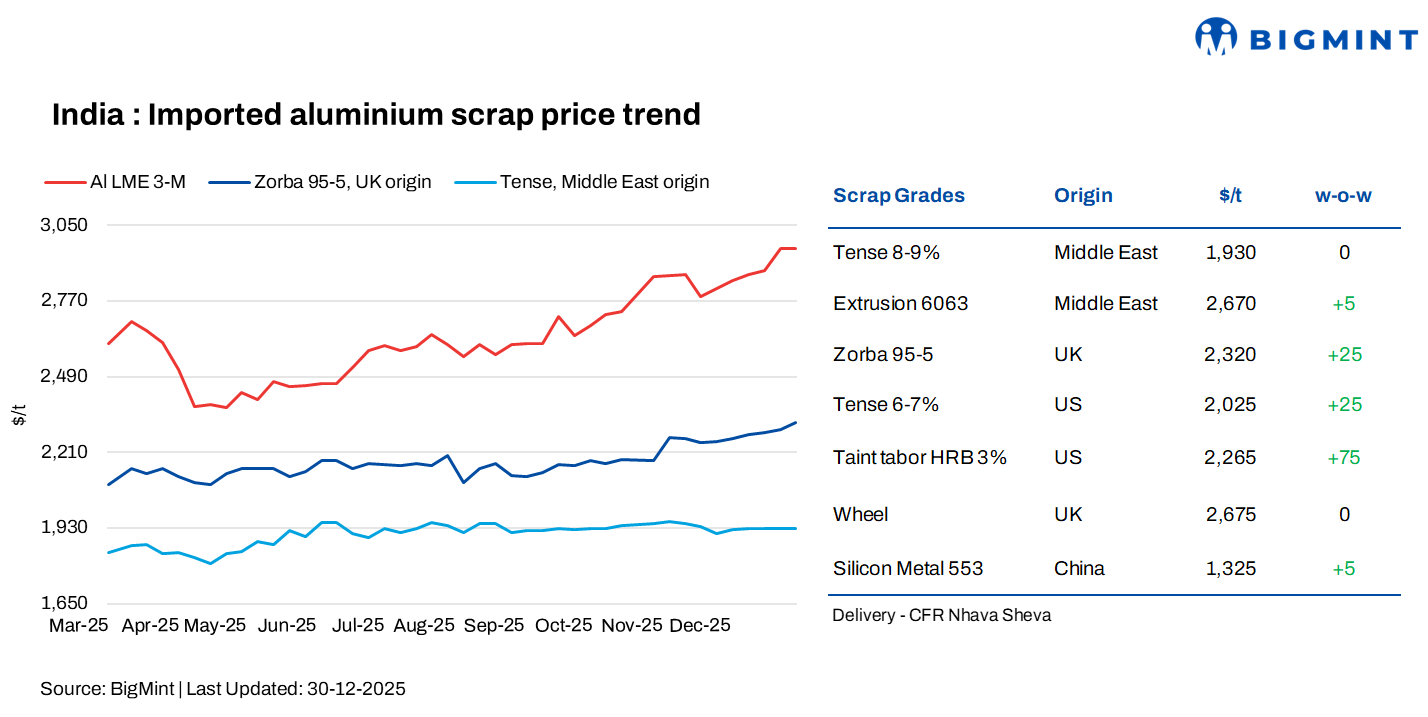

India’s imported aluminium scrap prices showed a firm-to-mixed trend in the week ended 30 December, supported by selective buying, with gains seen across several key grades. BigMint assessed Middle East-origin Tense (8-9%) at $1,930/t CFR Nhava Sheva, unchanged w-o-w, while Middle East-origin Extrusion 6063 edged up $5/t to $2,670/t.

Meanwhile, UK-origin Zorba 95/5 rose by $25/t to $2,320/t, and US-origin Tense (6-7%) increased $25/t to $2,025/t. Prices of US-origin Taint Tabor HRB (3%) recorded a notable jump of $75/t to $2,265/t, whereas UK-origin Wheel remained stable at $2,675/t.

LME aluminium prices rise, stocks stable

At close of trading on 29 December, LME aluminium three-month prices increased to $2,958/t, up $16/t w-o-w from $2,942/t on 22 December. Meanwhile, aluminium inventories at LME-registered warehouses edged down marginally by 350 t to 519,250 t, indicating broadly stable visible supply levels.

Prices were underpinned by confirmed smelter disruptions, declining inventories across key regions, falling Japanese port stocks, and firmer physical premiums, which outweighed lingering demand concerns. However, trading activity was limited as the LME remained closed on 25 and 26 December for Christmas holidays. Prices rose in the early part of the week before stabilising toward the end amid thin liquidity.

Market scenario

In India’s aluminium scrap market trading activity was muted during the holiday period despite strength in the global aluminium complex. LME aluminium continued to trade above $2,950/t, lending price support to scrap markets, though this firmness failed to translate into stronger buying interest for imported material. Market participants reported quiet conditions, with only modest demand for Taint Tabor and Extrusion, while overall buying remained cautious.

Demand for imported aluminium scrap stayed weak, as elevated price levels discouraged fresh bookings. Unfavourable exchange rate movements further pushed up landed costs, making imports less attractive for Indian buyers. In addition, holiday closures across key regions, including the US, Europe, and parts of the Middle East, led to limited offers, keeping liquidity thin and trade activity restricted.

Despite sluggish demand, imported scrap prices remained elevated and are not expected to soften in the near term, remaining supported by a firm LME environment and constrained availability. In contrast, the domestic scrap market showed greater strength, with prices rising across several casting grades due to tight supply conditions. Secondary aluminium producers increasingly favoured domestic material over imports, citing quicker availability and lower logistical risks. Tense scrap, in particular, remained tight in the domestic market, underpinning prices.

Overall, while demand for imported scrap continues to face pressure from high prices, currency headwinds, and seasonal factors, both domestic and imported scrap markets remain well supported. The outlook stays stable, with price support expected to persist as long as LME aluminium prices remain firm and domestic scrap availability stays constrained.

China silicon

According to BigMint, China-origin Silicon Metal 553 prices rose by $5/t w-o-w to $1,325/t on a CFR Nhava Sheva basis.

Outlook

In the near term, India’s aluminium scrap prices are expected to remain firm supported by strong LME aluminium prices, tight domestic scrap availability, and limited import offers due to supply-side constraints. While imported scrap demand may stay subdued due to high prices, currency pressures, and lingering seasonal slowdown, downside risks appear limited. The domestic market is likely to stay better supported, especially for Tense and casting grades, as secondary producers continue to prefer local sourcing. Overall, price support is expected to persist as long as LME aluminium remains elevated and scrap availability stays constrained.

Leave a Reply