- Bid-offer gaps remain wide across grades

- Domestic Tense scrap remains particularly scarce

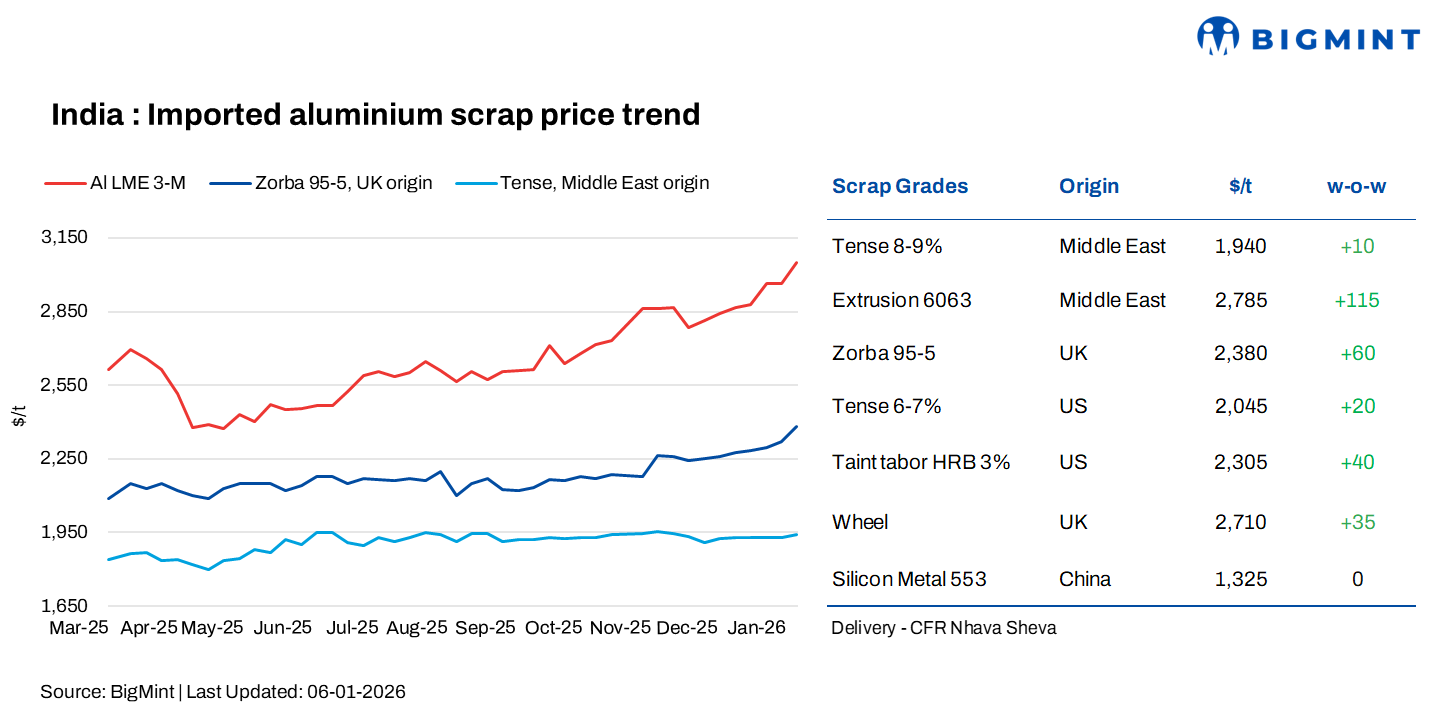

India’s imported aluminium scrap prices rose in the week ended 6 January, supported by selective buying and stronger global aluminium sentiment. BigMint assessed Middle East-origin Tense (8-9%) at $1,940/t, up $10/t w-o-w, while Middle East-origin Extrusion 6063 jumped $115/t to $2,785/t, led by improved interest in higher-grade material.

Meanwhile, UK-origin Zorba 95/5 increased by $60/t to $2,380/t, and US-origin Tense (6-7%) rose $20/t to $2,045/t. Prices of US-origin Taint Tabor HRB (3%) climbed $40/t to $2,305/t, while UK-origin Wheel scrap gained $35/t to $2,710/t. Overall, the market remained firm, with gains across most grades amid cautious but steady buying interest.

LME aluminium climbs sharply as stocks edge lower

At the close of trading on 5 January 2026, LME aluminium three-month prices rose to $3,051/t, up $93/t w-o-w from $2,958/t on 29 December 2025. Meanwhile, aluminium inventories at LME-registered warehouses declined by 12,500 t to 506,750 t, signalling a drawdown in visible stocks alongside the price increase.

LME aluminium prices touched the $3,000/t mark primarily due to tight global supply outlook and resilient demand expectations. The price surge reflects concerns over constrained output, including production caps in China, energy-related smelter disruptions, and supply deficits, which have limited availability of primary aluminium worldwide. At the same time, inventories on exchanges have remained relatively low, reinforcing the perception of a tightening market and supporting higher futures prices. These factors combined with firm industrial demand have propelled aluminium above $3,000/t for the first time in more than three years.

Market scenario

India’s imported aluminium scrap market entered the post-New Year period on a cautious footing as prices opened sharply higher, closely tracking the rally in LME aluminium, which crossed the $3,000/t mark. While the surge in global benchmarks initially lifted sentiment, it simultaneously curbed buying appetite, as many market participants turned cautious amid elevated prices and heightened volatility.

Trading activity remained subdued during the week, with a wide bid-offer disparity of $40-50/t prevailing across several grades. Buyers largely refrained from aggressive spot purchases, opting instead to wait for prices to stabilise before committing to fresh volumes. Market participants noted that rapid day-to-day movements in the LME increased price risk, prompting most consumers to restrict buying to need-based requirements. US-origin Tense (5%) was heard around $2,080/t, although transactions remained limited.

Demand trends diverged across origins and product categories. Middle East-origin Taint Tabor and Extrusion 6063 continued to witness slow buying interest. Sellers remained firm at elevated offers, reflecting higher replacement costs, while buyers showed reluctance to chase prices higher, resulting in minimal deal closures. Several participants indicated that suppliers were positioned at higher levels, but buyer resistance prevented meaningful upward price movement in these grades.

That said, Middle East-origin Extrusion scrap showed early signs of strengthening, supported by firmer downstream demand and tightening availability. Supplier offers were reported around $2,820/t, while buyer bids stood at $2,760-2,770/t, suggesting narrowing bid-offer gaps, though negotiations were still ongoing and trades were limited.

In contrast, the domestic scrap market displayed comparatively stronger momentum, with prices increasing week-on-week across multiple casting grades due to tight supply conditions. Secondary aluminium producers increasingly favoured domestic scrap over imported material, citing faster availability, reduced logistical uncertainties, and greater flexibility in procurement. Tense scrap remained particularly scarce in the domestic market, sustaining firm demand and providing strong price support.

Additionally, prices of domestic extrusion and taint tabor scrap also edged higher, tracking the upward movement in the LME and improving local market sentiment. Participants noted that while the market remains active and prices continue to rise in line with global benchmarks, overall trade volumes remain constrained, as buyers continue to balance operational needs against heightened price volatility.

Overall, the market is being driven by LME-led price strength and tight domestic scrap availability, while cautious buying behaviour, wide bid-offer gaps, and uncertainty over near-term price direction continue to temper spot trading activity.

China silicon

According to BigMint, China-origin Silicon Metal 553 prices remained stable w-o-w at $1,325/t on a CFR Nhava Sheva basis

Outlook

In the near term, imported aluminium scrap prices are expected to remain firm but volatile, closely tracking movements in the LME amid tight global supply and low exchange inventories. However, buying activity is likely to stay cautious, with market participants preferring need-based purchases until prices show clearer stability. While domestic scrap prices may continue to find support due to tight availability, imported scrap demand could remain selective as wide bid-offer gaps and elevated price risk limit aggressive spot buying.

Leave a Reply