- Tight supply and weak demand keep market cautious

- Wheel scrap shortage deepens supply concerns

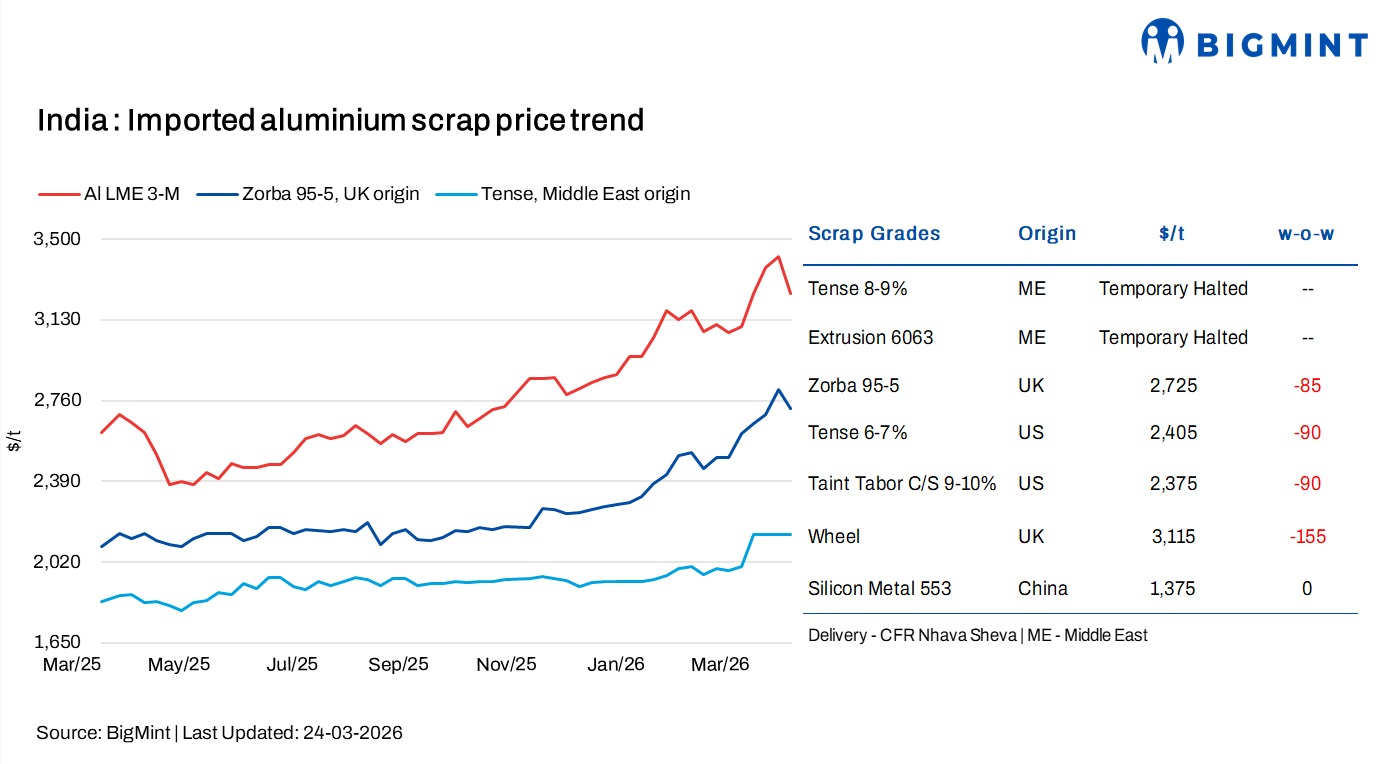

India’s imported aluminium scrap prices recorded a week-on-week decline as of 24 March 2026, tracking weakness in London Metal Exchange trends amid ongoing geopolitical tensions, which have tightened global supply conditions.

As per market assessment for CFR Nhava Sheva deliveries, UK-origin Zorba 95-5 scrap fell by $85/t w-o-w to $2,725/t, while US-origin Tense 6-7% scrap declined by $90/t w-o-w to $2,405/t, reflecting continued pressure on imported aluminium scrap prices despite constrained global supply.

LME aluminium declines w-o-w

Three-month aluminium closing prices on the London Metal Exchange declined by 5.7% w-o-w to $3,222/t on 23 March, down from $3,417/t on 16 March. Meanwhile, LME aluminium inventories also fell by 3.4% or 15,150 t over the same period, easing from 442,825 t to 427,675 t.

Meanwhile, Aluminium prices on the London Metal Exchange plunged over 8% on 19 March 2026, the sharpest drop since 2018, as the Iran conflict triggered a broad market sell-off. Weakening global economic sentiment, profit booking, and macro uncertainties weighed on prices, despite tight supply fundamentals and declining inventories, keeping the near-term outlook volatile.

Market scenario

Imported scrap prices declined week on week, tracking the downtrend on the London Metal Exchange, though the correction fell short of buyer expectations.

Supply side constraints remain severe, with a notable shortage of wheel scrap, especially from the UK, as volumes are increasingly diverted to Europe, while Australia continues to supply limited quantities. The situation has been further aggravated by reduced scrap inflows from the Middle East, leading to overall market tightness and concerns over potential cash flow pressures.

Logistical challenges have intensified the situation. Elevated freight costs and War Risk Surcharges amid ongoing tensions have increased landed costs and discouraged fresh bookings. Additionally, the absence of new offers from key Middle East hubs such as the UAE has effectively stalled regional trade flows.

In the domestic market, scrap prices remain elevated and out of sync with softer LME trends, driven by acute shortages of casting grade scrap. Secondary producers are facing difficulties in procuring key inputs like Tense scrap, leading to cautious buying and reduced operating rates.

Overall, the market remains firm but sluggish, with supply shortages outweighing demand. Sentiment is cautious, and near-term activity is expected to stay subdued until supply visibility improves and geopolitical uncertainties ease.

Chinese silicon prices

According to BigMint, China-origin silicon metal 553 prices remained stable w-o-w at $1,375/t on a CFR Nhava Sheva basis.

Outlook

In the near term, imported aluminium scrap prices are expected to remain under pressure in line with volatile LME trends. However, persistent supply constraints, particularly shortages of wheel and casting grade scrap, limited inflows from key regions, and ongoing geopolitical disruptions, are likely to provide a floor to prices. Market sentiment is expected to stay cautious, with subdued trading activity and range bound price movements until there is clearer direction in LME trends and improvement in global supply conditions.

Leave a Reply