- HZL SHG zinc prices continue to command premium over domestic spot market

- Supply disruptions, refined zinc deficit outlook support market sentiment

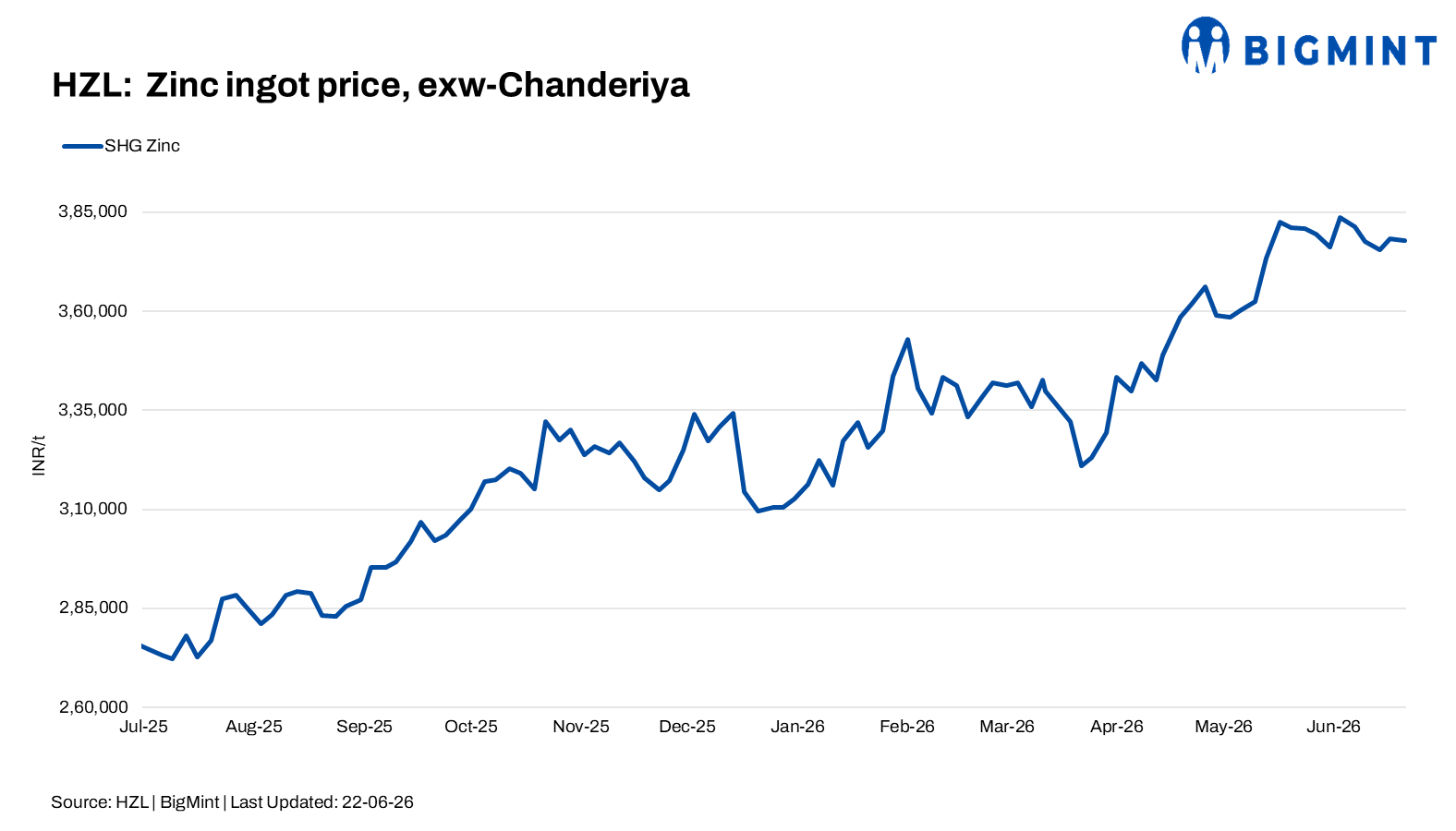

Hindustan Zinc Ltd (HZL) on 25 June 2026 reduced zinc ingot prices by INR 4,000/t ($47/t) and lead ingot prices by INR 1,900/t ($22/t) compared with its previous revision announced on 22 June.

Following the revision, HZL’s benchmark Special High Grade (SHG) zinc ingot prices were lowered to INR 373,800/t ($4,365/t), while lead ingot prices declined to INR 216,500/t ($2,528/t).

Other revised zinc grades were:

Special High Grade-Continuous Galvanising Grade (SHG-CGG): INR 375,300/t ($4,383/t)

Special High Grade Jumbo (SHG-Jumbo): INR 374,300/t ($4,371/t)

High Grade (HG): INR 373,300/t ($4,359/t)

Prime Western (PW): INR 371,800/t ($4,342/t)

On the London Metal Exchange (LME), zinc prices were trading at $3,421/t, up 0.38% as of 12:30 PM IST. However, zinc futures remained under pressure and hovered near seven-week lows amid a stronger US dollar. Expectations of higher US interest rates have boosted the greenback, making dollar-denominated commodities less attractive for buyers using other currencies and weighing on broader metals sentiment.

Despite the latest reduction, HZL’s SHG zinc prices remained above domestic spot market levels. According to BigMint’s assessment, SHG zinc ingot prices were assessed at INR 369,600/t ex-Delhi on 24 June, placing HZL’s benchmark SHG prices at a premium of around INR 4,200/t. Market participants indicated that procurement activity remained largely need-based, with buyers maintaining cautious purchasing strategies amid ongoing volatility in international prices.

The broader zinc market continues to receive support from supply-side disruptions at several major operations. Glencore’s Kazzinc facility in Kazakhstan remains affected by reduced operating rates following an explosion, while Nexa’s Cajamarquilla smelter in Peru continues recovery efforts after fire-related damage. In addition, a seismic event earlier this year at Boliden’s Garpenberg mine has raised concerns over the possibility of prolonged lower output.

At the same time, easing geopolitical tensions following progress in US-Iran discussions have helped improve expectations for industrial activity and demand recovery, partially offsetting the negative impact of the stronger US dollar on metals prices.

Fundamentally, the zinc market remains relatively tight. The International Lead and Zinc Study Group (ILZSG) has projected a refined zinc deficit of 19,000 tonnes in 2026, reinforcing expectations of constrained metal availability despite recent price corrections.

Overall, global zinc prices may remain supported by ongoing supply disruptions, low inventories and expectations of a refined market deficit. However, a stronger US dollar and uncertainty surrounding global economic growth could continue to limit upside momentum. In the domestic market, buying activity is expected to remain measured, with consumers closely monitoring international price trends and downstream demand conditions.

Leave a Reply