- Spread triples to INR 1,800 from INR 600 in July

- Weighted average BF rebar prices fall by INR 700/t in Aug

- Domestic demand robust but global downturn weighs on prices

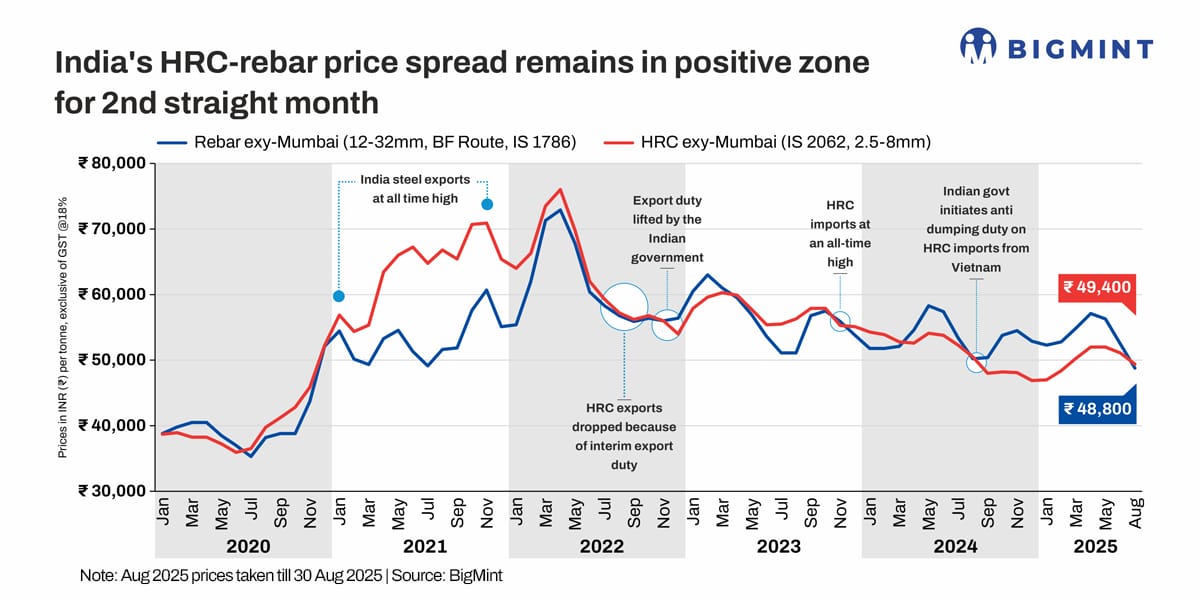

Morning Brief: Domestic steel prices in India see-sawed for much of August 2025, declining towards the latter half of the month due to seasonal and festive slowdown affecting trade sentiment. The spread, or gap, between domestic HRC (IS 2062, 2.5-8mm) and blast furnace-origin rebar (12-32mm, IS 1786) prices remained in positive zone for the second consecutive month in August. In fact, compared with July, the spread tripled m-o-m to INR 1,800 in August.

This was due to HRC prices actually increasing by INR 500/t m-o-m to settle at a weighted average of INR 49,900/t in August, while BF rebar prices declined INR 700/t m-o-m failing to hold on to gains made in early-August.

Notably, after remaining in reverse territory for 10 consecutive months since September 2024, the HRC-rebar spread had finally turned positive in July. Under normal market conditions, HRC commands a premium of around INR 4,000-5,000 over BF rebar. However, persistent weakness in global steel prices from end-2024 onwards eroded domestic flat steel prices and pushed the spread into reverse zone.

Factors affecting steel prices

HRC market movements: Leading Indian steel manufacturers officially raised the list prices of HRC and CRC by INR 1,000-2,000/t ($11-23/t) for August compared to the net sales price in end-July.

Prices increased as global market sentiments improved. The India hot-rolled coil (HRC, S275) export index rose by $5/t w-o-w to $540/t (FOB main port), supported by improved global sentiment and higher Chinese export offers. This upward movement in Chinese prices lent support to domestic sentiment. Steel prices also received support from NMDC hiking iron ore prices for August by up to INR 450/t.

However, after the Independence Day break the market witnessed a slowdown, with demand remaining weak and inquiries limited. Market participants attributed the sluggish scenario to the festive period which extended for 10-12 days towards the latter half of the month and dampened trading momentum.

BigMint’s benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) fell by INR 300/t ($3/t) w-o-w to INR 49,700/t ($567/t) on 26 August against INR 50,000/t ($570/t) on 19 August. Monsoon and festive holidays impacted trade activity, with prices remaining rangebound in the trade segment. Market participants cited labour shortages across key regions as weighing on sentiments and delaying restocking decisions, not to mention the availability of sufficient stocks in the trade channel.

HRC imports & trade measures: India’s bulk imports of HRCs touched 290,767 t as of 23 August, based on vessel line-up data. Around 229,139 t of additional cargoes are expected by the second week of September.

The Directorate General of Trade Remedies (DGTR) has recommended staggered duties of 11-12% on imports of alloy and non-alloy flat steel products for three years. The investigation, initiated in 2024, established that rising imports were causing serious injury to domestic producers and safeguard duties were required to provide relief.

Moreover, DGTR has recommended an anti-dumping duty of $121.5/t on imports of hot-rolled flat products of alloy or non-alloy steel from Vietnam, following the final findings of its investigation, as announced on 13 August. The DGTR has recommended a fixed anti-dumping duty for imports from Vietnam for five years.With landed HRC prices from China and Japan remaining higher than domestic prices, it is clear that the safeguard duty has stablised the market condition for domestic players.

BF rebar market in August: The primary mills increased rebar prices by up to INR 2,000/t ($23/t) for early-August deliveries as against end-July. Rebar inventories dropped by 5% from end-July levels in the first week of August as mills liquidated material in the projects segment. A general anticipation of a surge in construction after monsoon, as well as positive property registration data in key markets, and the shrinking spread with IF rebar tags propelled BF rebar prices amid overall recovery in the steel market.

However, trade prices started declining from mid-August. In the project segment, too, prices trended down and festive week slowdown in the trade channel weighed on market sentiment. Some primary mills reduced rebar list prices by INR 1,000/t, while others offered discounts due to slow lifting of material. Inventories with the primary mills edged down slightly.

In the last week of August, trade-level prices dropped INR 600/t w-o-w. Market activity was muted, as buyers stayed cautious during the monsoon season and the Ganesh Chaturthi festive week. Construction momentum dampened due to logistical challenges, leading to project delays and subdued procurement. Therefore, rebar prices lost much of the gains made in early August.

Outlook

BigMint’s flagship domestic steel index fell to nearly five-year lows in the last week of August and the downturn in global steel production and prices will affect domestic prices. After a brief rally in August, Chinese steel prices appear to be softening again, with the China Iron and Steel Association (CISA) forecasting a rangebound price outlook in the last few months of 2025. So, it would be unrealistic to expect price support from the global market, especially China.

On the domestic front, consumption remains on a growth trajectory and pickup in construction activity after monsoon and steady growth in demand from the automotive and appliances sectors during the approaching festive season are expected to keep steel prices supported. It appears that the HRC-rebar spread could narrow a bit in September if rebar prices gain momentum.

However, as in previous years, if the monsoon extends till mid- to late-September, price recovery prospects will remain dim.

Leave a Reply