- Rebar rides production cuts, higher procurements

- HRCs resort to maintenance despite low demand

- Export offers may remain low, weigh on flats

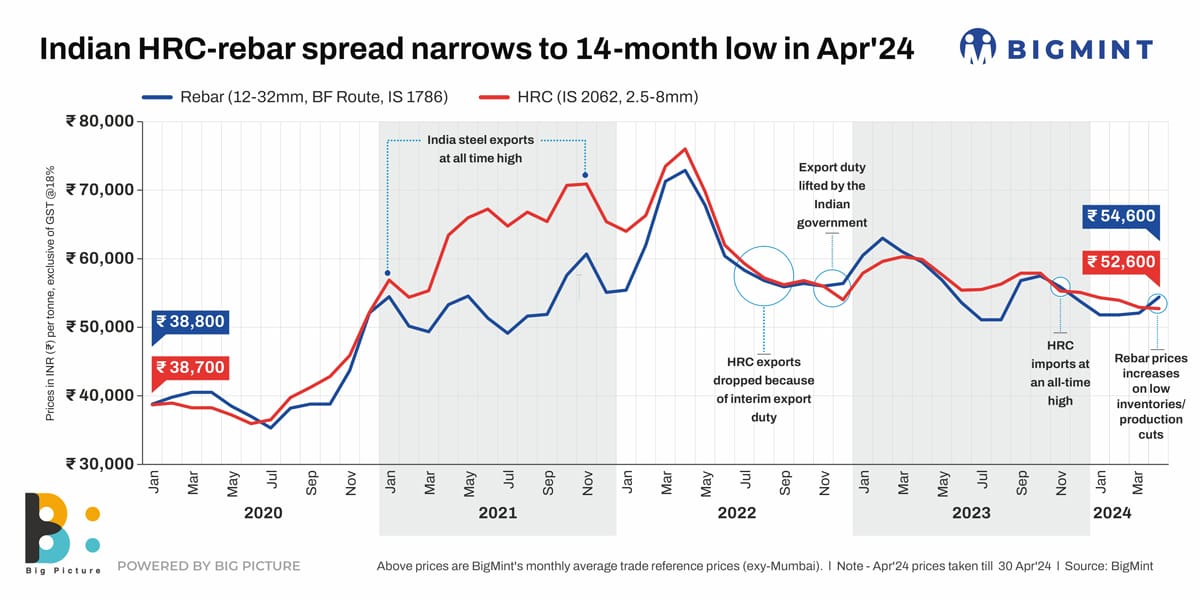

Morning Brief: In a reverse trend, benchmarked hot rolled coils (HRCs) became cheaper than rebars again after a five-month gap. Usually HRCs are sold at a premium of around INR 4,000/tonne ($48/t) to rebars. However, with this reversal, the spread between HRCs and blast furnace-route rebar narrowed in April 2024 to a 14-month low of INR 2,000/t ($24/t), reveals data maintained with BigMint. In February 2023, the spread had tightened to INR 3,400/t ($41/t).

BF rebars, ex-Mumbai, rose 5% or INR 2,500/t ($30/t) to INR 54,600/t ($654/t) in April against INR 52,100/t ($624/t) in March. On the other hand, trade-level HRCs, ex-Mumbai, decreased a marginal INR 200/t ($2/t) to INR 52,600/t ($630/t) against INR 52,800/t ($632/t).

After remaining muted in January-February, rebars showed a steady uptrend over March-April while HRCs have been consistently falling since September-October, 2023 till April 2024, buffeted by excess supply, and dull home and away demand.

Factors that reversed the spread

Rebars

Production cuts by tier-1 mills: Saddled with inventory from earlier in the year, mills undertook production cuts from January to restore the supply-demand imbalance. April saw 70,000-80,000 t of production loss in rebars.

The excess supply from tier-1 mills thus reversed. Volumes held with them dropped around 25% in early April. From levels of 500,000 t in early March, 2024, these fell to 350,000-375,000 t in early April. The tight supply allowed prices to gain further momentum and hit a five-month high in April.

Good projects demand in end-March: After remaining dull for the better part of Q4FY’24 (January-March), the market saw a resurgence in buying in March. Project segment buyers were eager to stock up ahead of the fiscal year-end and also because they wanted to beat election-related supply disruptions. Thus, mills were busy in April, supplying orders placed in March.

Higher discounting incentive for distributors: With the fiscal year-end approaching, many large mills also increased their discounts with distributors as an incentive for the latter to lift larger volumes. Last fiscal was no exception and the increased discounts led to a spurt in offtake from distributors around March. The good demand helped to deplete inventories at the trade level, giving a good reason for the price increase.

IF mills’ rebar prices rise m-o-m: IF mills too saw decent pre-election demand pull which lessened the inventory idling time from 8-10 days in March to 5-7 days in April. Plus, some mills undertook maintenance for 2-3 days, which also helped to rationalize production and keep demand firm. As a result, prices, ex-Mumbai, rose around 3% m-o-m to INR 50,500/t ($605/t) in April. Since IF mills enjoy 65-70% of the rebar market, a price increase here usually keeps BF prices supported as well.

HRCs

Maintenance supports nominal price hikes: In flats, HRCs were not so lucky. Mills and trade-level players raised prices nominally throughout April despite continued dull demand amid a supply glut. In fact, the pre-election liquidity crunch hit flats quite hard. The price hikes were more due to the maintenance shutdowns undertaken by some tier-1 mills at their hot strip and cold rolling mills. The shutdowns were expected to keep prices supported despite the lack of domestic and export demand. Because the price increases were nominal, overall benchmark HRC prices were still down by INR 200/t m-o-m.

Export offers fall m-o-m: The export scene was quite dismal. The HRC export index started the month with a w-o-w fall of $8/t at $567/t FOB, and decreased further to $560/t, tailing off with no offers in the month-end. M-o-m, the index fell to $562/t FOB from $583/t in March.

Mills were in no mood to export because of two factors. One was the stiff competition from China whose offers were lower at $537/ FOB in April. Secondly, because of the maintenance shutdowns, mills did not have enough to offer in the export market.

Outlook

Both rebar and HRC prices may see further upticks – rebar because of the inventory depletion, and flats, thanks to maintenance schedules. However, there is a question mark on their absorption in the market. This may encourage imports yet again.

Export offers may continue to remain dull which will weigh on HRCs.