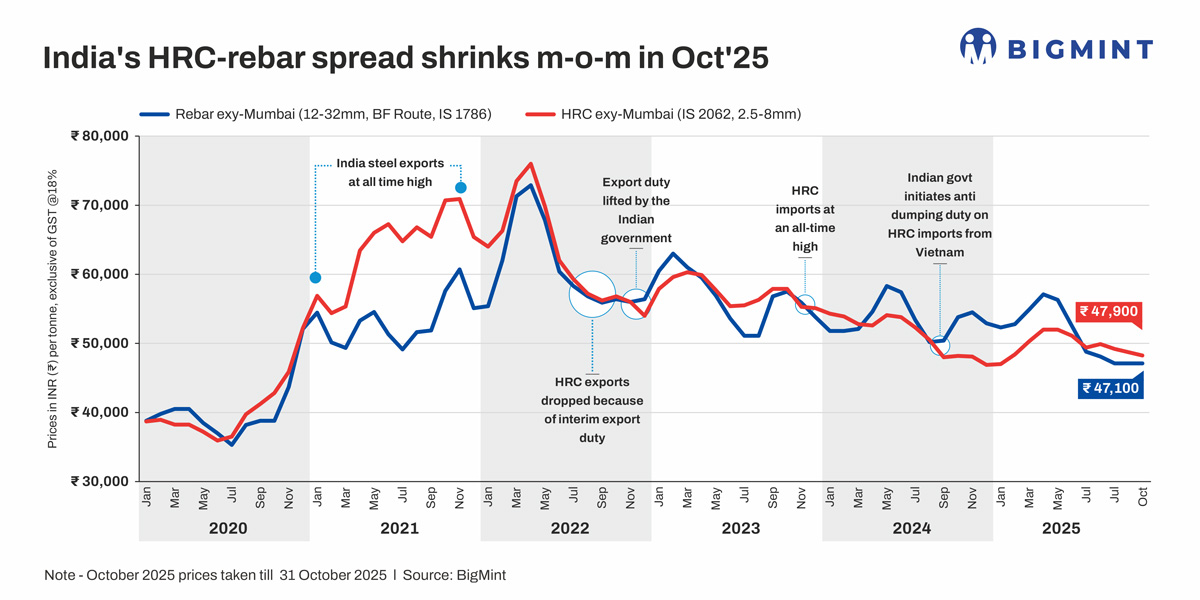

- Spread contracts to INR 800/t in Oct from INR 2,000/t in Sep

- Weighted average HRC prices drop INR 1,200/t m-o-m

- BF rebar prices flat, IF steel market sees post-festive rebound

Morning Brief: Indian steel prices in October 2025 showed a downward trend amid slowdown in trade momentum and the rapid buildup of inventories ahead of the festive season, although a trend reversal in the form of gradual resurgence in market momentum after the festive holidays was witnessed toward the end of the month.

The spread, or gap, between domestic HRC (IS 2062, 2.5-8mm) and blast furnace-origin rebar (12-32mm, IS 1786) prices remained in positive zone for the fourth consecutive month in October. However, in contrast with the INR 2,000/t expansion in September, the spread narrowed to INR 800/t in October. While weighted average HRC prices declined by INR 1,200/t m-o-m in October (or 2.5% m-o-m), rebar prices stayed flat.

After remaining in reverse territory for 10 consecutive months since September 2024, the HRC-rebar spread had finally turned positive in July this year. Under normal market conditions, HRC commands a premium of around INR 4,000-5,000/t over BF rebar. However, persistent weakness in global steel prices from end-2024 onwards eroded domestic flat steel prices and pushed the spread into reverse zone.

Steel price scenario in Oct’25

HRC market movements: The leading steel manufacturers decreased prices of hot-rolled coils (HRCs) and cold-rolled coils (CRCs) by INR 750-1,500/t ($8-17/t) for October sales as compared to the list prices of early-September in the first week. However, from the net sales prices of end-September, prices were raised by INR 500/t ($6/t) for October.

The HRC market remained sluggish as slow demand, oversupply, and high inventories pressured prices. Buyers limited purchases to immediate needs, avoiding bulk bookings. Thin margins, heavy stocks, and the Navratri and Durga Puja holidays further dampened trading activity.

HRC trade prices edged lower in the last week of October due to demand staying subdued amid limited trading interest. A source informed Bigmint, ”Market participation remains thin as post-festive sentiment is still soft, with many participants yet to return fully to active trading”, resulting in a slow and quiet market mood.

On the other hand, India’s HRC export prices to the EU declined in October and remained well below Chinese steel export prices for Southeast Asia and the Middle East. Therefore, weakness in global steel prices had a direct impact on domestic flat steel prices.

BF rebar market: The primary mills increased rebar prices by up to INR 1,000/t $11/t) for early-October deliveries as against levels prevailing in end-September. It should be noted that mills had offered discounts/rebates to augment sales in September.

However, prices in the IF steel market fell in the range of INR 200-1,000/t across regions in mid-October. Finished long steel prices fell on selling pressure due to high inventory levels and subdued demand. As a result, trade-level BF rebar prices declined w-o-w in mid-October. The major primary mills either offered discounts or reduced list prices due to subdued sentiment ahead of Diwali.

Trade prices edged down w-o-w across major markets in end-October as some primary mills either increased their discounts or reduced list prices owing to subdued market sentiments after Diwali. Inventories at mills rose slightly by around 15% in end-October, compared with levels seen at the beginning of the month, as per sources. This was majorly due to a slow domestic market during the festive season.

This was despite the fact that the IF rebar market witnessed a positive trend in end-October supported by improved buying activity and better sales momentum. The market reflected positive vibes post-Diwali, with increased participation from traders and increased momentum in major projects which strengthened overall sentiment.

Outlook

With the safeguard duty in place, trade remedial measures have offered support to domestic producers amid market slowdown. Landed cost of imports from key countries are higher than domestic prices, which are at a 5-year low.

Domestic steel prices will most likely remain rangebound in the near term, with a slight rebound likely. Flat steel export offers may stay under pressure in the short term, driven by cautious market sentiment and the approaching CBAM. This will be a drag on domestic prices too. Liquidity constraints and uncertain market conditions may limit demand amid softening global prices.

In the longs segment, the post-Diwali resurgence in market momentum and expectations of a pickup in infrastructure and construction activities will drive steel demand and trade. Market participants are largely in a wait-and-watch mode. The upcoming monthly price revisions expected to be announced by the leading mills will guide sentiment and set the trajectory for the domestic market.

Leave a Reply