- HRC offers to Middle East decline w-o-w

- Export offers to Nepal remain steady

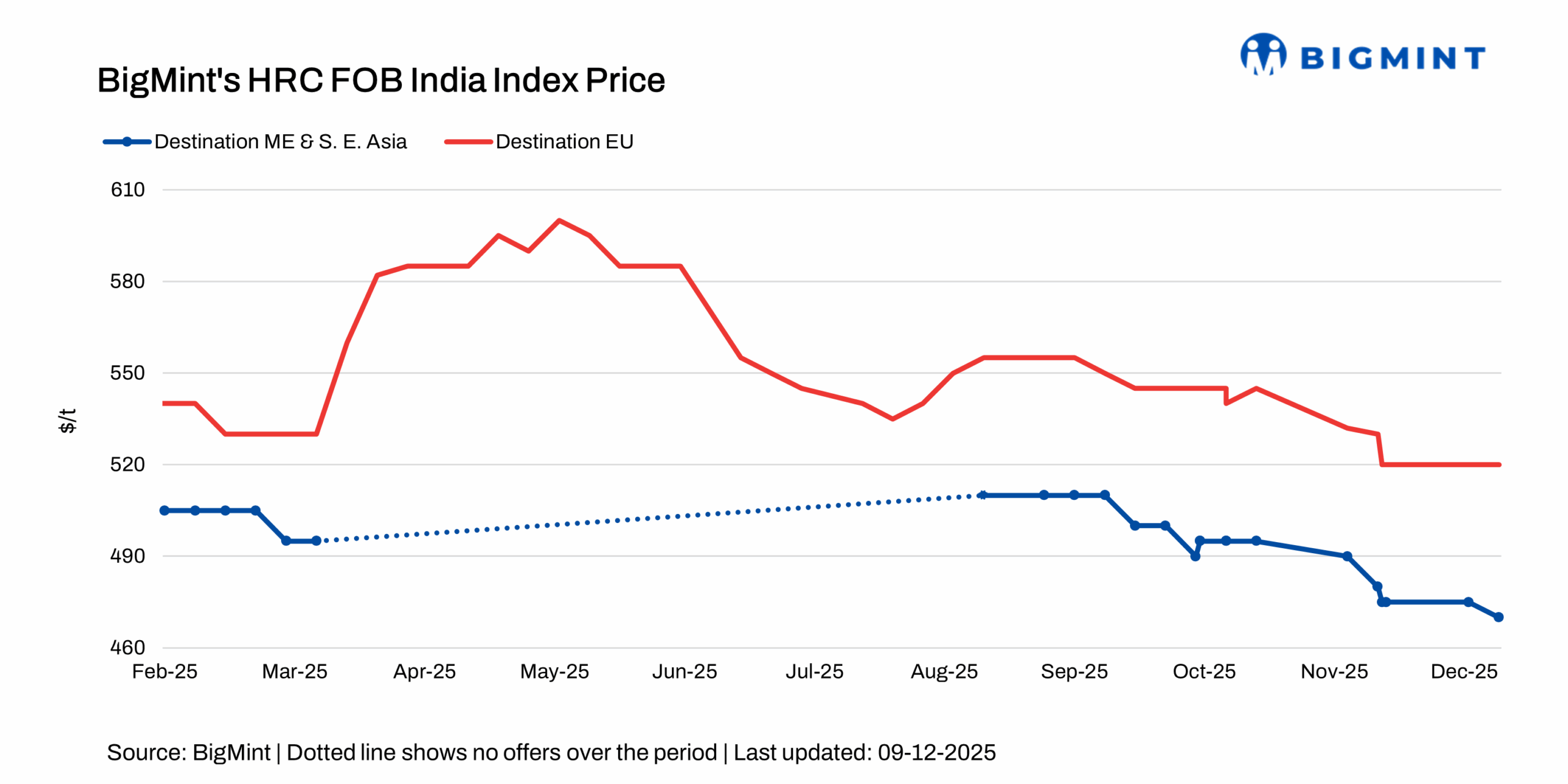

BigMint’s Indian hot-rolled coil (HRC, S275) export index for the European Union (EU) remained unchanged w-o-w at $520/t FOB main port, with mills refraining from issuing new offers after fully exhausting their October-December export quota.

Uncertainty around the EU’s Carbon Border Adjustment Mechanism (CBAM) continues to weigh on HRC exports, with many mills holding back lower-margin offers and still waiting for official guidelines to be released. A gradual rebound is expected only once CBAM rules become clearer, particularly for mills supplying compliant or higher-value products, leaving the market cautious in the meantime.

However, the Indian HRC (SAE 1006) export index for the Middle East slipped by $5/t w-o-w to $470/t, as trading activity remained subdued amid weak demand driven by the slowdown in construction activity and global oversupply.

1. HRC offers to EU remain steady w-o-w: Indian HRC export offers to EU remained flat for the week, as mills have largely pulled back from issuing new offers as mills has already exhausted their allocated quota for Q4CY’25. The last heard indicative offers were around $570/t CFR Antwerp.

European domestic steel demand remains subdued, with trading activity muted amid high inventories and lingering uncertainty around CBAM. Even with clarified rules, the market lacks clear direction as market participants maintain a wait-and-watch stance ahead of January. A more defined shift is expected only in early 2026, when CBAM begins to translate into actual cost structures and provides greater transparency to market dynamics.

2. HRC offers to Middle East: Indian HRC export offers to ME dropped by $5/t w-o-w to $495/t CFR UAE against $500/t last week. In contrast, China’s HRC export offers to ME increased by $5/t w-o-w to $485/t CFR UAE, as compared to $480/t a week ago. A BigMint source indicates, “the recent slowdown in both sales and customer interest is creating pressure in the market. Meanwhile, futures prices are holding steady”. Another BigMint’s reliable source says, “uncertainty is prevailing in the market, leading to a noticeable slowdown. Major regional bookings are currently absent”.

HRC futures on the Shanghai Futures Exchange (SHFE) January 2026 contracts fell by 1.7% w-o-w to RMB 3,267/t ($462/t) on 9 December 2025, from RMB 3,325/t ($471/t) on 2 December.

3. HRC offers to Nepal: India’s HRC export offers to Nepal remains stable w-o-w, with offers hovering around $485/t CFR Raxaul. Moreover, a deal of 21,000 t was reportedly booked at $480–484/t CFR levels for December shipments. “Weak regional demand is prompting buyers to seek lower offers, though firm bookings remain unconfirmed at lower levels”, says a BigMint source.

Outlook

Indian HRC export offers are likely to remain largely stable in December. With EU mills having already exhausted their October–December quotas and CBAM-related uncertainty deterring buying, fresh offers to Europe are expected to be limited, keeping activity muted amid high inventories. Weak construction demand and global oversupply may weigh on Middle East sentiment, while Nepalese buyers remain cautious. Overall, exports are likely to stay subdued until global steel demand shows a clearer recovery.

Leave a Reply