- HRC offers to Middle East, too, decline w-o-w

- CBAM uncertainty keeps EU buyers cautious

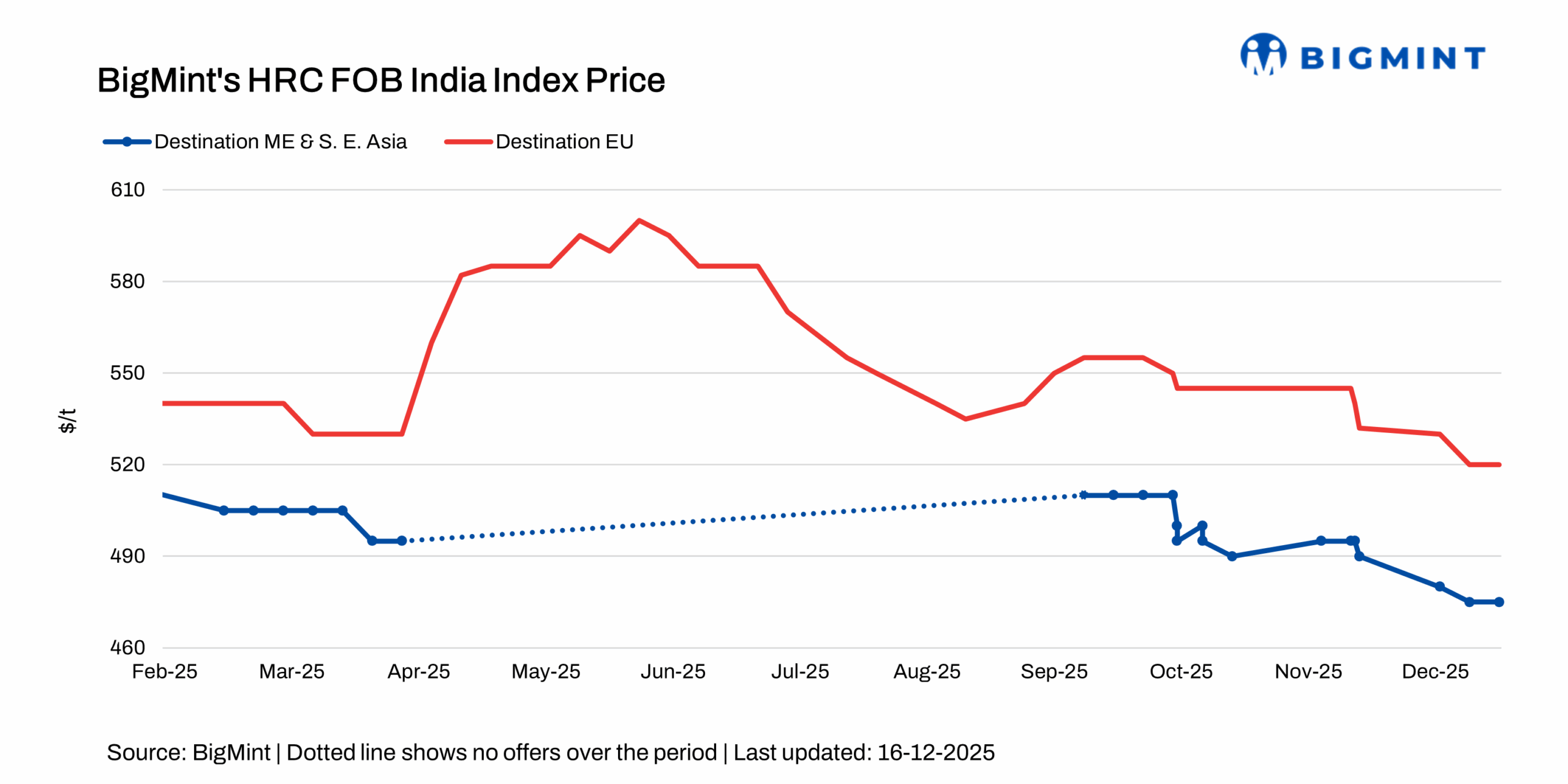

BigMint’s India HRC (S275) export index for the European Union (EU) held stable at $520/t FOB main port, with mills largely stepping back from issuing new offers amid CBAM-related uncertainty.

BigMint’s India hot-rolled coil (HRC, SAE 1006) export index for the Middle East declined by $5/t w-o-w to $465/t compared with $470/t the previous week, as demand stayed weak ahead of the upcoming Christmas holidays in the region. A source told BigMint, “Following recent news on steel export licence requirements for Chinese companies buyers are holding back and closely monitoring the potential implications for regional supply.”

European steel buyers are increasingly adopting a cautious, wait-and-watch approach, which has kept transaction volumes subdued despite broadly stable prices. While import offers remain competitive, high inventories and potential compliance costs are discouraging buying, keeping the overall market muted.

1. HRC offers to Middle East: Indian HRC export offers to the Middle East declined by $5/t w-o-w to around $490/t from $495/t the previous week. Demand in the region was subdued, reflecting a cautious stance adopted by market participants ahead of the Christmas holidays.

China’s HRC export offers declined by $5/t w-o-w to $480/t CFR UAE from $485/t. China’s Ministry of Commerce and General Administration of Customs has declared steel products need export licences, updating the 2025 License Catalogue per the Foreign Trade Law. Exporters must submit contracts and quality certificates; licences are issued by national, provincial and city authorities.

HRC futures on the Shanghai Futures Exchange (SHFE) January 2026 contracts declined by RMB15/t (2/t) or 0.5% w-o-w to RMB 3,252/t ($462/t) on 16 December from RMB 3,267/t ($464/t) on 9 December.

2. HRC offers to EU remain stable w-o-w: Indian HRC export offers to the EU remained stable w-o-w, as mills have largely stepped back from issuing new offers amid CBAM-related uncertainty. The last reported indicative offers were around $570/t CFR Antwerp.

Market sentiment in Europe remains cautious. Ample inventories and year-end inactivity are prompting buyers to delay purchases.

Outlook

Indian HRC export offers are expected to remain largely stable in December. In Europe, CBAM, weak demand, and high inventories are likely to limit fresh offers, keeping market activity subdued. In the Middle East, weak demand ahead of the Christmas holidays may further constrain export momentum. Overall, exports are expected to remain subdued.

Leave a Reply