- Quota clarity remains insufficient to improve EU buying sentiment

- Hormuz uncertainty continues to constrain Middle East trade activity

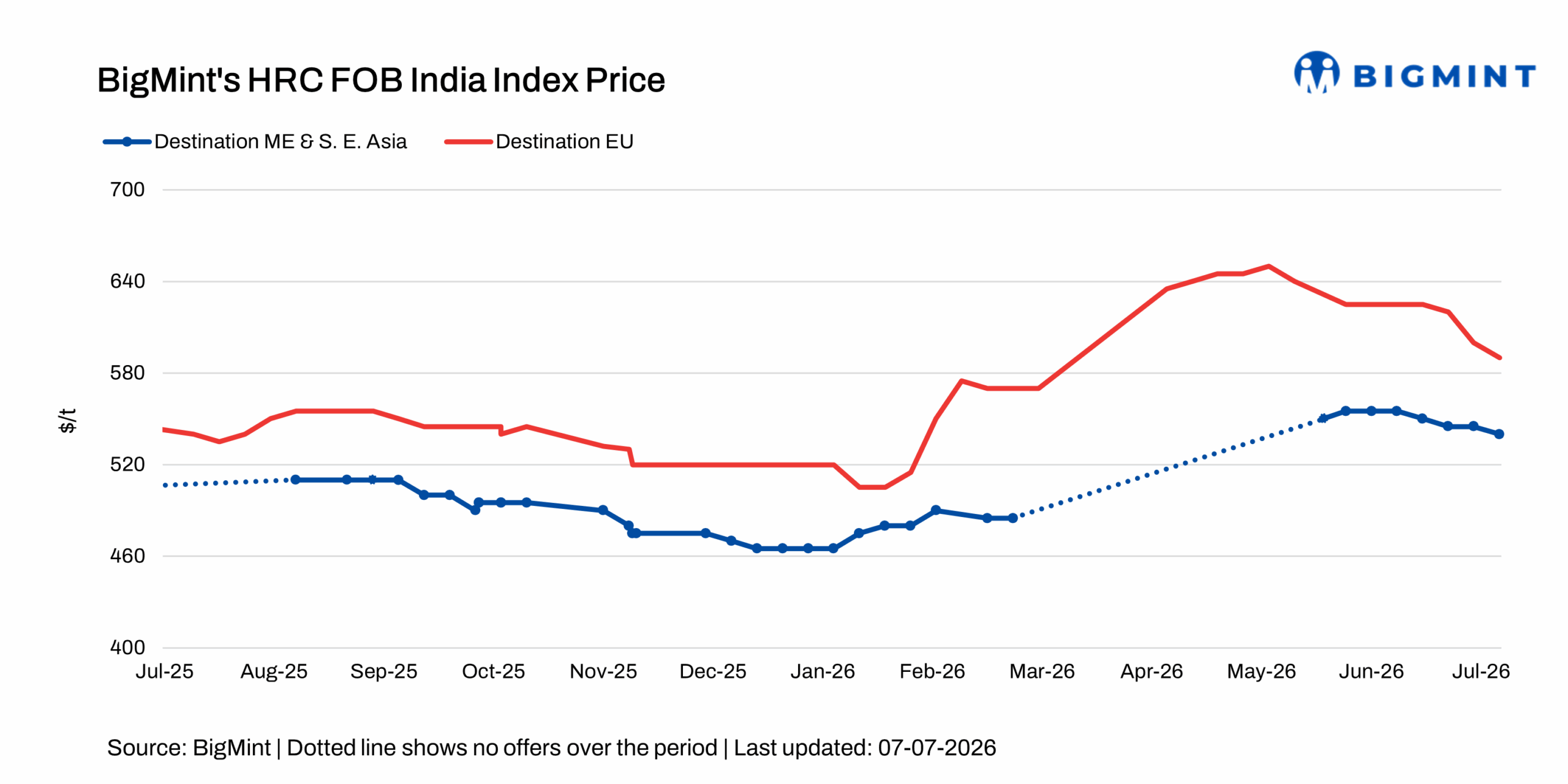

Indian HRC export activity remained subdued during the assessment week ended 7 July 2026, as cautious buying sentiment across key export destinations continued to weigh on trading activity.

HRC export offers to the EU decline w-o-w: Indian HRC export offers to the EU declined by $10/t w-o-w to around $590/t FOB, compared with $600/t a week earlier, amid lack of buying interest from European buyers, with no fresh bookings reported during the assessment period.

An EU-based source stated, “While the introduction of country-wise quota allocations has removed much of the previous uncertainty, it has not translated into a meaningful improvement in market sentiment. Market participants continue to assess the practical implications of the new quota distribution, as the allocated volumes are viewed as insufficient, with buyers continuing to adopt a cautious approach.”

At the same time, the EU has announced the Q2 CBAM certificate price at $75.28/t of CO2, marginally lower than the Q1 price of $75.36/t of CO2. As the quarterly certificate price is derived from the weighted average of EU ETS auction clearing prices, the marginal decline indicates that carbon prices remained broadly stable during the quarter, leaving CBAM compliance costs for importers largely unchanged.

HRC export offers to the Middle East, Southeast Asia drop w-o-w: Indian HRC export index for the Middle East and Southeast Asia fell by $5/t w-o-w to around $540/t FOB from $545/t in the previous week.

HRC offers to the Middle East were heard at around $545/t FOB, down by $5/t w-o-w from $550/t a week earlier, with freight to Jeddah estimated at approximately $60/t. Meanwhile, Chinese HRC export offers to the region fell sharply by $15/t w-o-w to approximately $560/t CFR Jeddah from $575/t in the previous week.

Indian HRC export offers to Vietnam decreased by $15/t w-o-w to around $535/t CFR Ho Chi Minh City from $550/t a week earlier, amid weak demand and muted buying interest in the region.

A Middle East-based source stated, “While some vessels have managed to transit through the Strait of Hormuz, the operational situation remains uncertain, as there has been no official confirmation of unrestricted navigation or a formal agreement ensuring the free flow of maritime trade. As a result, market participants continue to exercise caution, with the lack of clarity surrounding shipping operations sustaining freight uncertainty and weighing on overall trading sentiment.”

Another UAE-based source said, “Vessel owners are still reluctant to transit through the Strait of Hormuz, with many shipowners continuing to adopt a cautious stance despite some reported vessel movements. Many remain unwilling to resume regular transits until there is greater confidence in the sustainability of normal shipping operations.”

Outlook

Indian HRC export activity is expected to remain under pressure in the coming days, as weak demand across key overseas markets and cautious procurement strategies continue to limit fresh bookings.

In the EU, although country-wise safeguard quota allocations have provided greater regulatory clarity, the allocated volumes have yet to meaningfully improve buying interest, while broadly stable CBAM compliance costs are unlikely to materially alter import economics.

Meanwhile, in the Middle East, persistent uncertainty surrounding vessel transits through the Strait of Hormuz is expected to keep freight costs and shipping risks elevated, discouraging aggressive procurement.

Leave a Reply