- HRC prices seen falling since last six months

- CRCs benefit from higher downstream, auto usage

- Prices likely to stay range-bound in short term

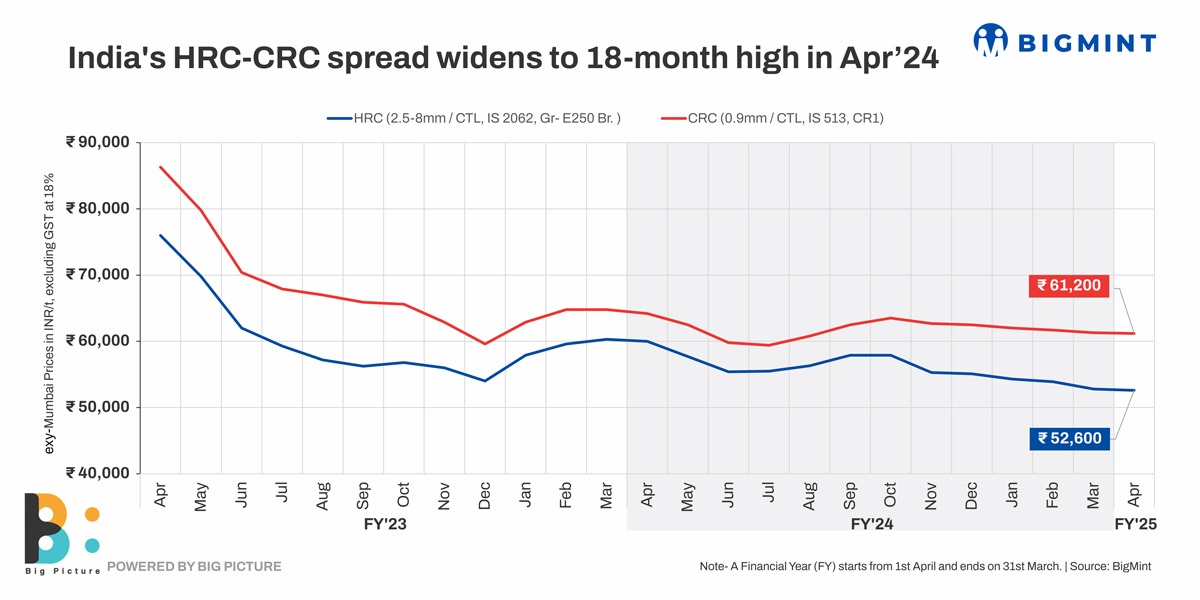

Morning Brief: The spread between benchmarked hot rolled and cold rolled coils widened to an 18-month high of INR 8,600/tonne ($103/t) in April 2024, reveals data maintained with BigMint. Such levels were last seen in October 2022.

Traditionally, CRCs are sold at a premium to HRCs. However, the spread has been widening since July 2023 – mainly on account of the steady price erosion in HRCs since September-October 2023. Prices have fallen from around INR 57,900/t ($693/t) in these two months last year to INR 52,600/t ($630/t) in April 2024. CRCs, on the other hand, have moved in a narrow range in this period, navigating from INR 63,500/t ($760/t) to INR 61,200/t ($733/t).

HRCs have fallen 9% in the last six months against CRCs’ 4%.

On a m-o-m basis, HRCs fell by a marginal INR 200/t ($2/t) and CRCs by INR 100/t ($1/t) while the spread upped a negligible INR 100/t.

Factors that widened the spread

HRCs

The price drop in HRCs was higher when pitted against CRCs mainly because of the following factors:

Higher output pressures down prices in Q1CY’24: HRC production increased 6% to 14 million tonnes (mnt) in Q1 (January-March, 2024) against 13 mnt in Q4CY’23 (October-December) and 13% from 12.55 mnt in Q1CY’23. This was mainly on account of increased supplies in the market. NMDC’s Nagarnar Steel Plant starting commercial production from late last year while JSPL commissioned its 5.5 mntpa hot strip mill at Angul. But demand lagged behind supply which pressured down prices.

Increased HRC imports put mills on backfoot: The barrage of HRC imports from China and FTA countries in Q1CY’24 drove tier-1 mills further up the wall. They were already fighting weak domestic demand against excess supply. In Q1CY’24, imports rose 10% to 1.92 mnt against 1.74 mnt in Q4CY’23 and a whopping 79% compared to 1.07 mnt in Q1CY’23.

Weak exports trend: The third whammy came in the form of weak exports trend. China took away chunks of the Middle East and Vietnam markets with cut-throat pricing while Europe remained weak after flickering to life for a short span in early 2024. Export offers dropped m-o-m further to $562/t FOB India in April from $583/t in March, and averaged $685/t in Q1CY’23. In October-December 2023, mills were forced to hold back offers because of the price unviability factor.

CRC

CRCs were more comfortably faced with downstream demand comparatively higher:

Maintenance shutdowns limits CRC availability: Tier-1 mills, challenged by the triple whammy of low domestic and overseas demand and excess supply, eventually resorted to maintenance shutdowns. Some put their hot strip mills (HSMs) on maintenance shutdown to reduce HRC production especially from April. This impacted availability of the base material for cold rolling and led to tighter CRC supply. This, in turn, kept CRC prices supported with a marginal m-o-m drop.

Higher HRC diversion for CRC downstream use: Mills also resorted to diverting their HRCs towards coated flat steel production in-house, and this averaged an astounding around 90%. Downstream CRC utilisation averaged 8.83 mnt in January-March 2024 against 7.98 mnt in Q4CY’23 and 7.52 mnt in Q1CY’23. Naturally, saddled with HRC inventory, mills evolved a good way to utilise the same. This also kept CRC prices propped-up especially since galvanised exports rose q-o-q to 667,000 t in Q1 against 323,000 tonnes in October-December 2023.

Accelerated CRC demand from auto makers: India’s automobile production rose 9% in Q1CY’24 to 7.39 million units (MU) against 6.75 MU in Q4CY’23 and 31% compared to 5.66 MU in Q1CY’23, as per SIAM data. Thus, after robust downstream utilisation, the balance CRC volumes were being swept up by automotive manufacturers, giving another reason to sustain prices of the same. Auto demand is expected to maintain the momentum amid good forward bookings for delivery around Diwali.

It may be mentioned CRC is a key input in making suspension systems, automotive frames and engine components amongst others.

Outlook

Prices of both HRCs and CRCs are likely to stay range-bound in the near term. The reason can be attributed to lower demand amid the general election process that is under way and will end on 1 June. Not much activity is expected until a stable government is in place.