- India aims for 37 MTPA production capacity by 2047

- Target to increase per capita consumption to 12 kg

India is setting its sights on an ambitious future for the aluminium sector. As part of its Vision 2047 plan unveiled recently, the Ministry of Mines aims to increase the country’s aluminium production capacity to 37 million tonnes per year (MTPA) by 2047 from the current 4.2 MTPA. This bold strategy is designed to position India as a global leader in aluminium production while meeting the country’s rapidly growing demand across a wide range of industries. The ambitious roadmap also envisions achieving 100% self-reliance in both primary and secondary aluminium production, reducing import dependency and enhancing India’s position in the global market.

India’s aluminium production targets, timeline

By FY’30, India’s aluminium production capacity – comprising 4.2 million tonnes (mnt) of existing primary capacity, 2.0 mnt of secondary capacity, and an announced addition of 3.0 mnt primary and 1.5 mnt secondary – is expected to total 10.7 mnt. While this may be sufficient to meet domestic demand, it still falls 1.6 mnt short of the 12.3-mnt projected requirement. To close this gap and achieve a 5% share in global aluminium exports, the government must incentivise new capacity creation, especially in the secondary segment, which needs urgent investments in scrap collection infrastructure to ensure at least 50% self-sufficiency.

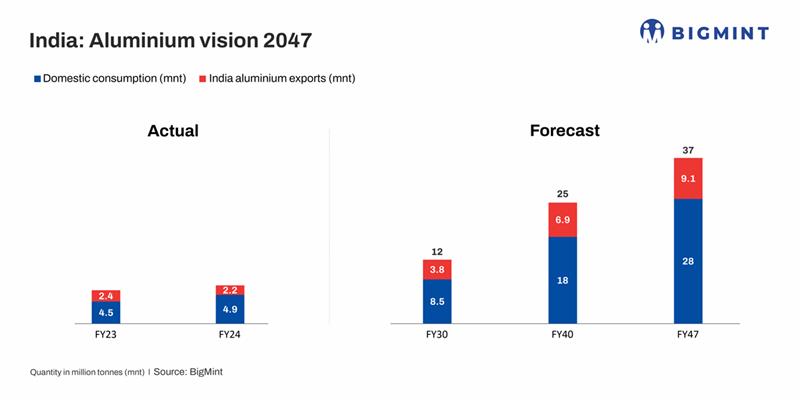

As India strives to strengthen its position as a global industrial powerhouse, aluminium is central to this transformation. The aluminium sector will be crucial in supporting sectors such as electric mobility, renewable energy, green infrastructure, and defence. To achieve this, India’s aluminium production needs to scale significantly, from its current level of 4.2 MTPA to 37 MTPA by 2047.

The target production timeline is as follows:

- 2030: Target production of 12 MTPA.

- 2040: Target production of 25 MTPA.

- 2047: Final target of 37 MTPA, achieving a nearly 800% increase in capacity from 2025.

This ambitious goal will require substantial investments in technology, infrastructure, and a skilled workforce. It is projected that the country will need an investment of over INR 20 lakh crore to achieve these targets, with a focus on increasing both primary and secondary aluminium capacities.

How can India close its 7-mnt aluminium supply gap by 2047?

By 2047, planned increases from new and existing bauxite mines, along with better use of resources and recycling, could add up to 30 mnt. However, there is still a 7-mnt shortfall. To close this gap, India needs to improve its scrap collection system and invest more in bauxite exploration so that most of the future aluminium needs can be met domestically without relying heavily on imports.

Per capita consumption to surge

India’s aluminium consumption is expected to surge dramatically in the coming decades. In 2023, India’s per capita aluminium consumption stood at 3.5 kg – well below the global average of 13 kg. By 2047, India aims to more than triple its per capita consumption, targeting 12 kg per person.

This increase in consumption will be driven by sectors such as automotive manufacturing, renewable energy, construction, and electronics, all of which are expected to experience massive growth.

Self-reliance in bauxite, alumina

A critical element of India’s aluminium vision is self-reliance in the raw materials required for aluminium production – bauxite and alumina. At present, India imports a significant amount of both resources, but the government plans to shift towards domestic self-sufficiency by 2035.

- Bauxite: In 2024, India produced 24 mnt of bauxite, but imports stood at 3.8 mnt, a number that has increased steadily over the past decade. The target is to meet 100% of India’s bauxite needs domestically by 2035.

- Alumina: India’s alumina production reached 7.6 mnt in 2024, but it imported 2.5 mnt. The vision for 100% domestic alumina production aligns with the broader goal of self-reliance and minimising the country’s dependence on external sources for critical raw materials.

By increasing domestic production of both bauxite and alumina, India aims to not only become self-sufficient but also reduce its carbon footprint associated with transportation and mining.

Reducing scrap import dependency

India currently relies heavily on imports of aluminium scrap to meet domestic demand. Imports account for 85-95% of India’s aluminium scrap needs. To achieve greater self-reliance, India plans to reduce its dependence on aluminium scrap imports over the coming decades.

The goal is to foster a circular economy by improving scrap collection and recycling systems. Enhancing scrap recycling infrastructure will contribute to reducing India’s dependency on imported metal and improve its environmental footprint by minimising waste.

Value-added aluminium exports: Moving beyond primary aluminium

India’s current export mix is heavily skewed towards primary aluminium, with 76% of volume and 65% of value coming from this segment. In contrast, China’s aluminium exports are dominated by value-added products, with 95% of China’s aluminium exports consisting of higher-value products such as extrusions, foil, and alloys.

India aims to move away from this reliance on primary aluminium exports and focus on increasing the share of value-added aluminium products in its exports. By doing so, India hopes to enhance its global competitiveness and capture higher margins in the international market. This shift will also create new opportunities for technology development, skills enhancement, and innovation in the Indian aluminium sector.

India’s value-added products export strategy is as follows:

- Target: Shift towards a higher share of value-added aluminium products in exports, emulating China’s success in this domain.

- Goal: Increase exports of extrusions, rolled products, alloys, and other high-performance aluminium materials.

This will require investments in technology, R&D, and infrastructure to build a competitive edge in producing premium aluminium products that meet international quality standards.

Investment, policy support for industry growth

Achieving these ambitious goals will require a concerted effort from both the government and the private sector. India’s aluminium industry must be supported by decisive policy reforms, financial incentives, and a focus on environmental sustainability. The government has already signalled its commitment by promoting ease of doing business, improving infrastructure, and introducing incentive schemes such as the Production-Linked Incentive (PLI) scheme for the sector.

The government aims to undertake the following measures for industry growth:

- Policy reforms: Streamlined permissions, land acquisition processes, and fiscal incentives.

- Production-linked incentives: Encourage innovation, efficiency improvements, and capacity expansion in the sector.

- Sustainability initiatives: Fostering green aluminium production and promoting low-carbon technologies.

Conclusion: A sustainable future for India’s aluminium industry

India’s aluminium sector is at a turning point. With a clear vision for 2047, the country has the potential to become a global leader in aluminium production while achieving self-reliance in critical materials. By significantly ramping up production capacity, fostering domestic raw material supply, and transitioning towards value-added aluminium exports, India can not only meet its growing domestic demand but also strengthen its position in the global aluminium market.

The road ahead will require substantial investment, collaboration, and policy support, but if executed well, India’s aluminium sector will play a critical role in achieving the nation’s vision of a $30 trillion economy and a sustainable, developed India by 2047.

Leave a Reply