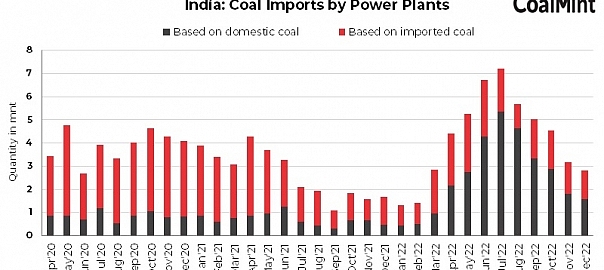

Imported coal procurement by India’s thermal power plants has gradually slowed down after the utilities received ample coal from the domestic market. However, the government’s preparedness for upcoming peak summer season is expected to trigger a fresh surge in demand.

Latest data provided by the power ministry shows that coal imports by plants decreased 12% m-o-m to 2.8 million tonnes (mnt) in December 2022, dropping to their lowest in FY23.

Notably, imports are steadily falling since July when purchase of seaborne coal was at its peak to compensate for the shortfall in domestic supplies. Higher imports were, in fact, driven by the government’s mandate as it had asked utilities to import coal for blending with domestic material.

Since then the two factors that have lowered the demand for imported coal have been robust performance from the domestic coal miners and comparatively lower growth trajectory of power consumption post summer.

Nevertheless, the country is likely to witness a similar jump in imports this year which will be again supported by the government’s flexible approach.

Fresh guidelines supporting imports

Reinstating its stance towards imports, the power ministry has instructed power plants to resort to imports by procuring 6% (by weight) of their needs for blending with domestic coal till September, 2023 failing which curtailment in domestic supply has been proposed.

Last year, the blending ratio was kept at 10%, which was later lowered in view of supply normalcy.

Moreover, the ministry has intended to procure electricity from imported coal-based (ICB) plants for April-May when power availability is expected to be less than demand. A tender has already been floated to this effect.

This provision would provide ICBs an avenue for power sale, due to which these utilities will need to explore the global market for running their operations.

Low inventory a threat

Coal inventory at power plants have gradually improved to 33.13 mnt at end of January, 2023 against the lows of 26.11 mnt seen in September, 2022.

The current stock is in a better position compared to previous year’s level of 25.31 mnt, but comparatively lower compared to 37.04 mnt in January 2021 and 39.16 mnt in January 2020.

Given the logistics bottlenecks and domestic supplies not being commensurate with demand, many plants are expected to push for imports to maintain adequate inventories and avert possible outages resulting from the above-average temperatures during summer.

Leave a Reply