- Asian NPI prices surge to one-year high

- US tariff impact minimal on Europe prices?

Prices of Indian domestic stainless steel finished flat and long products remained largely stable for the week, with market activity subdued due to Mahashivratri celebrations in the Mumbai region.

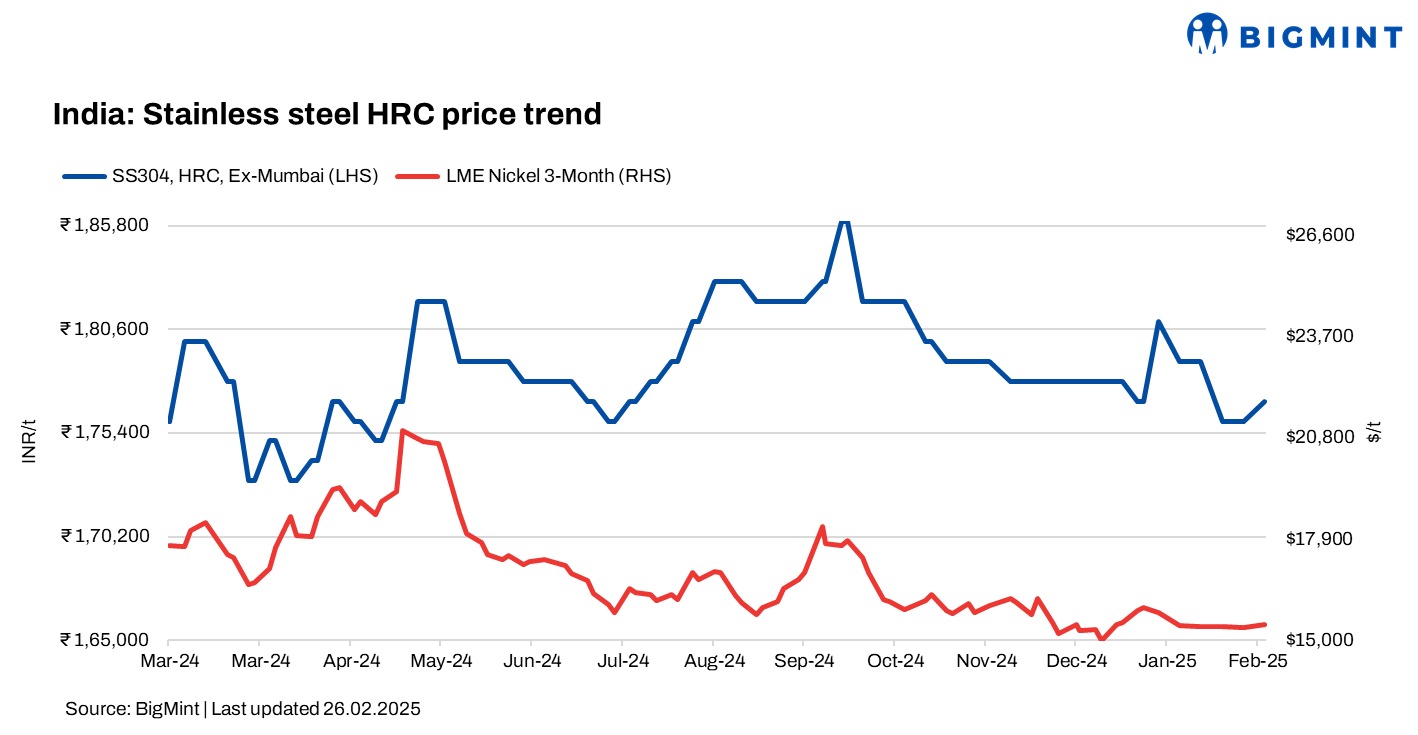

BigMint’s benchmark assessment for stainless steel (304 series) hot-rolled coils (HRCs) stood at INR 177,000/t, up by INR 1,000/t, while SS 304L (25-100 mm) black round bars stood at INR 160,000/t, both ex-Mumbai.

LME nickel & NPI price movements

At the time of reporting, three-month London Metal Exchange (LME) nickel prices stood at $15,460/tonne (t), reflecting a marginal increase of 1% from last week’s $15,325/t. Nickel stocks in LME-registered warehouses inched up by 2% to 192,642 t compared to 189,516 t in the previous week.

Additionally, Asian NPI prices have been on a steady rise since the start of the year, reaching a year-high of $135.18/t as of today.

Chinese portside cargo prices for NPI (grade 13%>Ni>10%) also witnessed an increase of RMB 10/t ($1/t) w-o-w to RMB 970-980/t ($133-135/t). Meanwhile, Indonesia FOB prices for NPI (grade 13%>Ni>10%) stood at $115/t, unchanged w-o-w.

The quality of nickel ore in Indonesia continued to decline. The recent surge in NPI prices has been partly driven by production curtailments in key Indonesian regions in attempts to lower operating costs. Additionally, high-grade nickel ore stocks remained limited, and nickel content in major mining areas is reportedly depleting.

Freight rates for small handysize vessels were as follows: from Bahudopi (Indonesia) to Ningde (China) at $20/t, from Weda to Tianjin at $24/t, and from Weda to Ningde at $22/t.

Finished flats range-bound w-o-w

This week, finished flats prices remained steady amid limited market movement and subdued demand, further impacted by the Mahashivratri holiday. Additionally, it was heard, HRC imports were continuing to flow into India.

As per BigMint’s assessment, SS 316 HRCs were up by INR 500/t w-o-w to INR 321,000-322,000/t ex-Mumbai.

A trade source informed BigMint, “Stainless steel imports into India continue to be dominated by Vietnam and Indonesia. Vietnamese suppliers are offering 304 2B material at $1,860/t for narrow and $1,980/t for broad width, CFR India. Indonesian material is priced at $1,900/t CFR India. Meanwhile, South Korean HRCs remain expensive at $1,980/t CFR India, making these less competitive.”

Finished longs hold steady w-o-w

BigMint’s assessment of SS 316L (25-100 mm) black round bars stood at INR 269,000-271,000/t ex-Mumbai. Prices of SS 316L (25-100 mm) bright bars stood at INR 287,000-289,000/t ex-Mumbai, stable w-o-w.

According to BigMint sources, “Demand for finished goods remained sluggish in the market with no signs of improvement. Due to month-end pressures, buyers have adopted a wait-and-see approach before making further bookings.”

Additionally, the price levels for SS 304 wire rod (5-16 mm) also held steady at INR 155,000/t, ex-Mumbai.

China SS prices dip

In China, domestic stainless steel prices of 304-grade CRCs stood at RMB 13,700/t ($1,887/t) exw, down by RMB 50/t ($60) w-o-w, while FOB prices of 304-grade CRCs were at $1,890/t.

Europe market inert to US tariffs?

The impact of US tariffs on the European stainless steel market has been minimal so far. Major European producers believe the tariffs will have little effect on their operations and may even open new market opportunities by reducing Asian exports to the US.

The 25% US tariffs have led to price stabilisation in Europe amid demand uncertainty, posing short-term pricing challenges for sellers. While no major market shift is expected, the EU exports significant volumes of long products, particularly round bars, to the US. However, most European stainless steel sales consist of specialised grades with limited alternatives.

Raw materials overview

Ferro molybdenum: Indian ferro molybdenum prices witnessed an increase of INR 75,000/t ($860/t) w-o-w as compared to the previous assessment. Prices went up as some increase was seen in LME futures and inquiries for the material also increased in the latter part of the week.

As per BigMint’s assessment on 25 February, ferro molybdenum prices in India were at INR 2,635,000/t ($30,242/t) exw on a 60% pro rata basis.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 100,400/t ($1,152/t) , increasing by INR 900/t exw-Jajpur.

At Vedanta-FACOR’s ferro chrome auction yesterday, the larger lot of 10-150 mm fetched an H1 price of INR 99,750/t exw, up by INR 550/t from the 6 January auction. The price rise is likely driven by limited domestic supply, stronger bids at OMC’s chrome ore auction, and positive market sentiments from China.

Outlook

In the near term, prices are expected to remain stable within a range, with buying activity likely to stay at low-to-moderate levels. Additionally, upcoming festivals like Holi are expected to further limit market activity.

Leave a Reply