- Shipments from UAE, India’s leading finished longs supplier, stall in Mar-May’26

- Higher cathode availability supports domestic copper processing growth

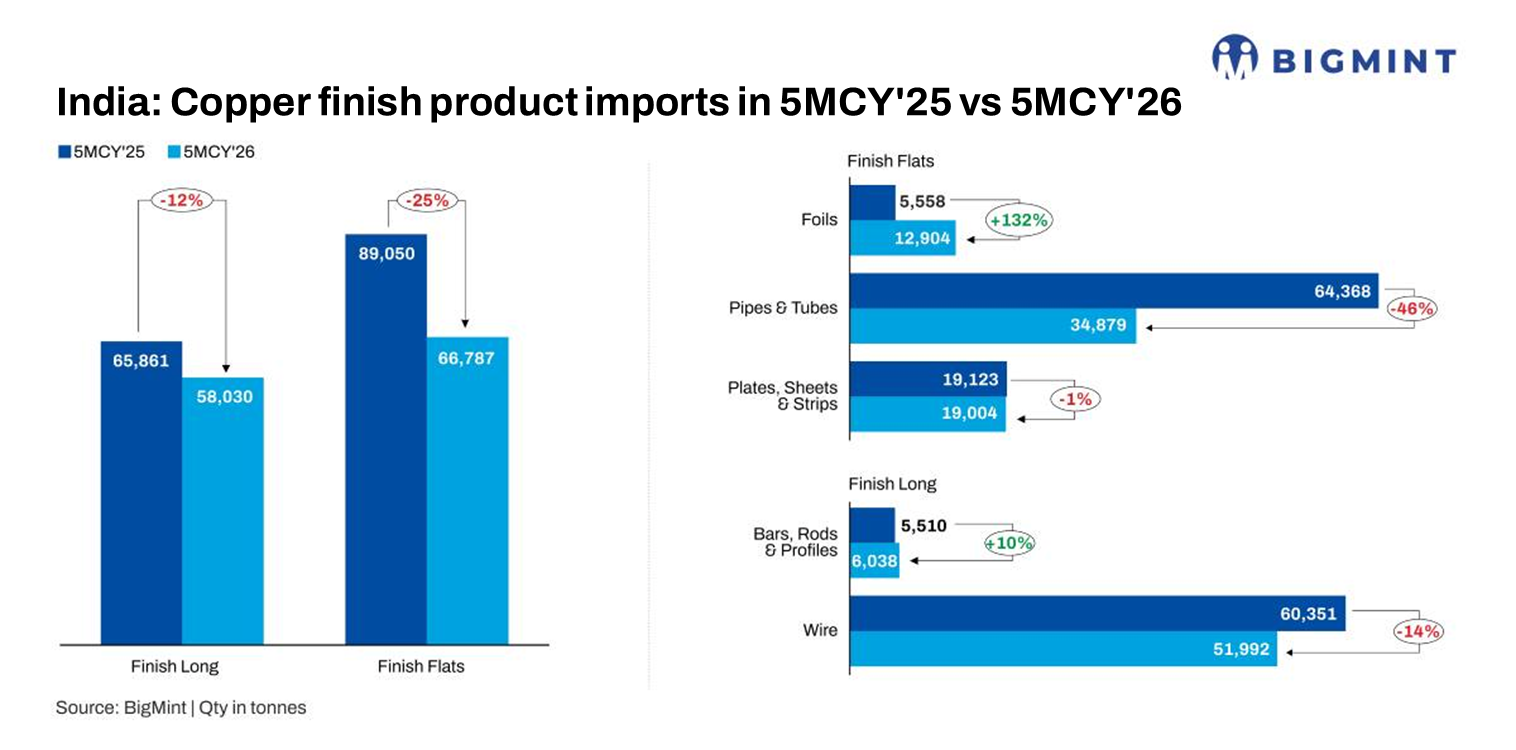

India’s imports of finished copper products weakened during the first five months of CY’26, with finished long imports declining 12% y-o-y to 58,030 t and finished flat imports falling 25% to 66,787 t. The decline reflects improving domestic downstream processing, shifting global trade flows driven by the Middle East conflict, and supply disruptions from key exporting regions due to stricter regulatory scrutiny. The decline comes despite steady expansion in India’s overall copper consumption on the back of growing electric vehicle sales and renewable energy and power infrastructure.

Additionally, improved availability of refined copper also supported lower finished imports. India’s refined copper cathode production increased 8% y-o-y during January-April 2026, while cathode imports climbed 37%, significantly expanding the availability of feedstock for domestic processors. This enabled manufacturers to increase production of standard finished products, partially substituting imported material.

India’s finished longs imports drop amid Middle East tensions

India’s finished long imports declined 12% y-o-y to 58,030 t during the first five months of CY’26. Among the product categories, wire imports fell 14% y-o-y to 51,992 t.

The decline was primarily influenced by disruptions in Middle Eastern trade flows. The UAE remained India’s largest supplier of finished long products, exporting 20,030 t during January-May 2026. However, nearly 84% of these shipments had already arrived during January-February, before geopolitical tensions in the Middle East intensified.

Imports from the region dropped sharply from 16,823 t during January-February to just 3,207 t during March-May. Compared with 28,882 t imported during March-May 2025, imports during the same period in 2026 declined by 89%, highlighting the severe impact of the conflict on regional trade.

The supply gap was partially offset by increased shipments from Asian suppliers. Malaysia more than doubled its exports to 12,951 t, while China and South Korea recorded increases of 21% and 13%, respectively. The shift highlights India’s growing reliance on ASEAN suppliers, supported by preferential tariff benefits under the India-ASEAN Free Trade Agreement (FTA), which has enhanced the competitiveness of Malaysian exports compared with suppliers from other regions.

Finished flat imports slide as ASEAN shipments hit regulatory hurdles

Imports of finished flat products declined more sharply, by 25% y-o-y to 66,787 t during January-May 2026. Among all sub-products, pipes and tubes witnessed the largest decline, falling 46% y-o-y to 34,879 t, while plates, sheets, and strips remained broadly stable with only a 1% decline.

In contrast, copper foil imports surged 132% y-o-y to 12,904 t, driven by robust demand from India’s rapidly expanding electric vehicle and lithium-ion battery sectors, where limited domestic production of battery-grade copper foil continues to support import dependence.

The divergence seems to stem from differing end-use patterns. With no major government projects currently in the pipeline, traditional plumbing and construction activities have slowed, thereby reducing demand for pipes and tubes. At the same time, EV adoption has increased significantly, supporting demand for foils and plates, sheets, and strips.

Imports from major ASEAN suppliers declined sharply, with Vietnam’s exports falling 54% y-o-y, while Malaysia and Thailand recorded declines of 44% each. The decline coincided with increased scrutiny by Indian customs authorities over the eligibility of certain copper products for preferential duty benefits under the India-ASEAN FTA. Enhanced verification of Rules of Origin (RoO) and stricter compliance requirements increased uncertainty and processing time for some ASEAN-origin shipments, making imports relatively less attractive.

China emerged as the only major supplier to register higher exports during 5MCY’26, with shipments rising 53% y-o-y to 25,169 t from 16,485 t a year earlier. The increase was supported by competitive pricing, ample product availability and China’s well-established downstream copper processing industry, particularly in high-value products such as copper foils.

Outlook

India’s copper demand is expected to strengthen steadily through FY’30, driven by capacity additions in renewable energy, power transmission, electric vehicles (EVs), battery manufacturing, and data centre infrastructure. According to the Centre for Social and Economic Progress (CSEP), demand from conventional sectors is projected to reach 3.24 mnt by FY’30, while energy transition-related consumption is expected to increase to 274,000 t, led by accelerating EV adoption and renewable power installations.

On the trade side, India’s import profile is expected to shift over the next 3-5 years. Rising domestic refining and downstream processing capacities should gradually reduce imports of conventional refined copper products and semi-finished materials. However, imports of high-value specialised products, particularly battery-grade copper foil and other advanced copper components required for lithium-ion batteries, are likely to remain elevated until large-scale domestic manufacturing capacities are commissioned and commercial production stabilises.

As a result, India’s dependence is expected to increasingly shift from bulk copper products towards technology-intensive copper materials required for the clean energy value chain.

Leave a Reply