- Rebar prices increase by INR 200/t w-o-w

- Imports remain soft as buyers resist higher offers

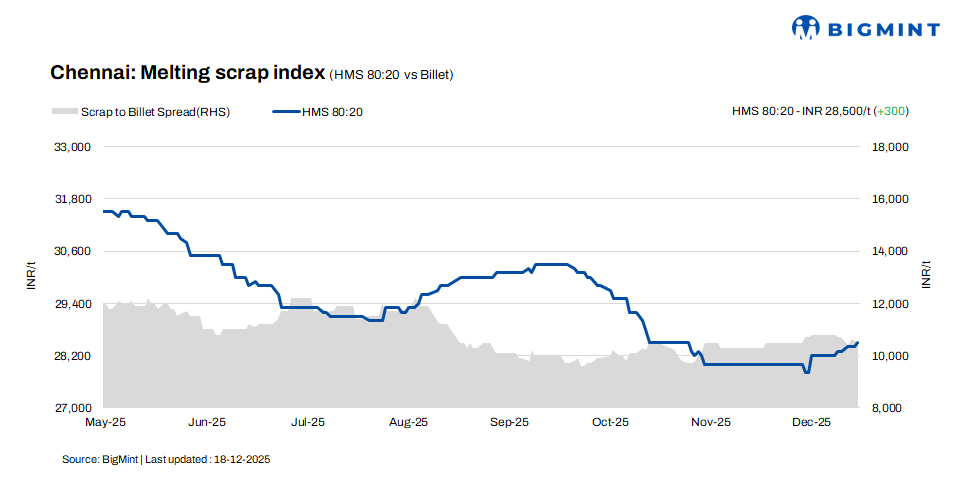

According to BigMint’s latest assessment, HMS (80:20) scrap prices in Chennai increased by INR 300/t w-o-w, reaching INR 28,500/t, supported by a mild d-o-d rise of INR 100/t. Billet prices stayed stable at INR 39,000/t on both daily and weekly bases, indicating balanced market conditions. Meanwhile, rebar prices edged up by INR 200/t d-o-d to INR 43,000/t and remained firm w-o-w. Overall, the market reflected a mixed trend, with stable scrap prices providing support, while moderate billet demand limited upside momentum.

Imported, domestic market trends

Market participants indicated imported shredded scrap offers at $340-345/t CFR Chennai, with buyers bidding around $330-335/t. HMS (80:20) scrap was offered at $320-322/t, while bid levels stood at $315-318/t. Buying interest stayed subdued, as domestic scrap prices continued to offer better cost viability compared to imported material, limiting fresh bookings.

In the Chennai market, domestic HMS (80:20) scrap is trading at INR 27,500-28,500/t for spot deals with immediate payment, while extended credit transactions are fetching higher levels of INR 28,500-29,500/t. Most market activity remains concentrated within the INR 28,000-29,000/t range, underlining the impact of liquidity pressures and the prominence of credit-driven pricing in the scrap market.

Buyer-supplier sentiments

According to a mill representative, sponge iron availability in the merchant market remains limited, as major producers continue to prioritise captive consumption. Billet prices have stayed stable, however, demand has improved compared to the past couple of weeks. Mills are gradually increasing project-based supplies, supported by bulk volume bookings, which is aiding in lowering finished steel inventories and providing mild stability to the market.

According to a scrap supplier, HMS (80:20) scrap prices are currently trading in the range of INR 28,000-29,000/t, largely influenced by payment terms and mill-wise quantity requirements. Persistent liquidity constraints continue to weigh on market sentiment, leading to moderate trade volumes. However, with the monsoon season nearing its end, demand for steel materials is expected to improve in the coming weeks.

Regional comparison

HMS (80:20) scrap prices in the Jalna market of western India were assessed unchanged at INR 29,500/t. Meanwhile, rebar prices increased by INR 200/t to INR 44,200/t. Conversely, billet prices registered a decline of INR 100/t to INR 39,200/t. Market sources noted improved finished steel trade activity in recent days. Stable scrap inflows are supporting mill operations, allowing producers to align output with steady regional demand.

Outlook

With monsoon conditions gradually easing, finished steel trade activity is expected to improve in the near term. However, scrap prices are likely to remain range-bound, with limited fluctuations of around INR +/- 500/t, influenced by prevailing market conditions and cautious buying sentiment.

Leave a Reply