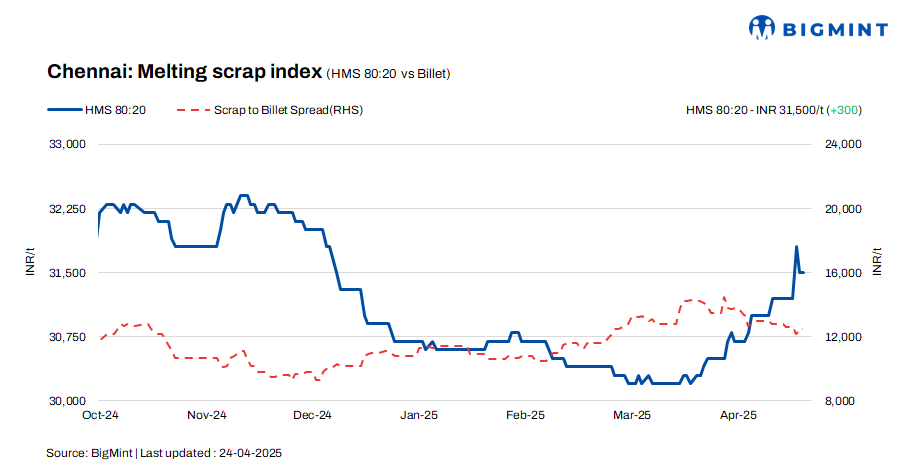

HMS (80:20) scrap prices in Chennai recorded a w-o-w increase of INR 300/t, reaching INR 31,500/t, according to BigMint’s latest assessment. However, prices remained stable on a d-o-d basis. Billet prices held steady at INR 44,000/t, with no changes observed d-o-d or w-o-w. Rebar prices declined by INR 300/t d-o-d, now assessed at INR 48,500/t. A similar drop of INR 200/t was noted w-o-w.

These shifts point to a firm scrap market amid weakening sentiment in the long products segment, suggesting varied momentum across the value chain.

Imported, domestic price trends

According to a scrap trader, indicative prices for Australian-origin containerised shredded scrap are currently at $370-375/t CFR Chennai, while HMS 1 is at $360-365/t. However, workable levels are slightly lower by $5-10/t. Suppliers are refraining from floating fresh offers amid the ongoing sharp decline in deep-sea scrap prices, reflecting growing caution in the global scrap market.

Domestic HMS (80:20) scrap is currently trading at INR 31,500-32,000/t for buyers opting for immediate payment. For transactions involving extended credit terms, pricing is slightly higher, in the range of INR 32,000-32,500/t. The majority of offers and concluded deals are concentrated within the INR 31,500-32,000/t range, reflecting a stable pricing environment and a preference for prompt-payment terms.

Buyer-supplier sentiments

A mill representative informed BigMint that sponge iron prices in Chennai have witnessed a slight increase, supported by price trends in neighbouring markets. Despite a modest supply shortfall, semi-finished steel prices remained largely stable. The large mills focused on rolling finished products like rebars, benefiting from favourable margins. Market demand for rebars remains moderate, though buyer sentiment is cautious due to prevailing uncertainty. The arrival of imported bulk vessels on the east coast this week and next is expected to ease current supply constraints in the ferrous segment.

As per a local scrap supplier, domestic HMS (80:20) scrap prices are trading in the range of INR 31,500-32,500/t, with slight adjustments based on payment terms. The onset of summer and ongoing heatwave conditions have led to labour shortages, disrupting scrap collection and supply chains. Constrained supply is pushing market participants to increase scrap procurement prices to ensure consistent material flow.

Regional comparison

The Jalna steel market continues to show stability, with rebar and HMS (80:20) scrap assessed at INR 49,500/t and INR 33,000/t, respectively. Billet prices edged down slightly by INR 200/t to INR 43,100/t. Market sentiment remains steady, supported by moderate trade volumes. Scrap inflows into mills are well-aligned with production requirements, reinforcing stable supply dynamics at existing price points.

Outlook

Market sources suggest that scrap prices are likely to remain within a narrow band, with potential variations of INR +/- 500/t in the short term. This is attributed to persistent uncertainty surrounding finished steel trade.

Leave a Reply