- Rebar demand weakens amid slow infrastructure activity

- Ongoing liquidity constraints continue to dampen trade

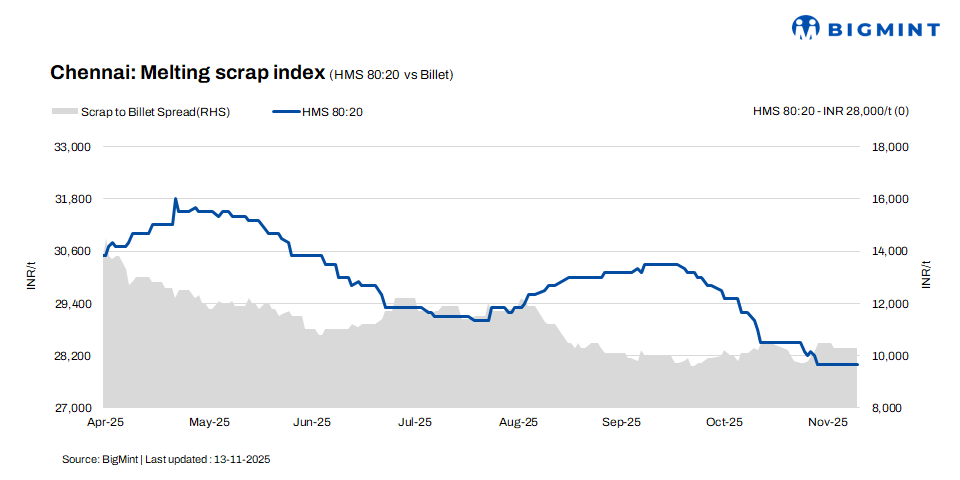

According to BigMint’s latest assessment, HMS (80:20) prices in Chennai remained unchanged at INR 28,000/t, with stability observed on both d-o-d and w-o-w bases. Billet prices also held firm at INR 38,300/t. In contrast, rebar prices slipped by INR 200/t to INR 42,800/t across both d-o-d and w-o-w assessments.

The market reflected a mixed sentiment, dominated by steady trading trends and limited price fluctuations through the week, indicating cautious buying amid subdued demand conditions. Overall, finished steel trade remained subdued, pressuring scrap demand.

Imported, domestic market trends

Imported shredded offers were in the range of $350-355/t CFR Chennai, while bids were slightly lower at $340-342/t, reflecting a $5-10/t bid-offer gap. HMS (80:20) was quoted at $325-330/t, with bids of around $316-320/t. Market participants highlighted that a deal was closed for Costa Rica-origin HMS (60:40) at $298/t CFR Chennai, along with another one for UK-origin HMS (80:20) concluded at $320/t CFR Chennai.

In the Chennai market, domestic HMS (80:20) was traded at INR 28,000-28,500/t for spot transactions with immediate payment. Deals involving extended credit terms fetched slightly higher prices in the range of INR 28,500-29,000/t. Market participants noted that most offers and concluded trades were concentrated within the INR 28,000-29,000/t band, reflecting the prevailing liquidity conditions and the growing influence of credit-based pricing in scrap trade.

Buyer-supplier sentiments

According to a mill representative, sponge iron prices softened in the market amid moderate demand, with only some mills actively offering material in the merchant market. Billet manufacturers are currently facing narrow or breakeven margins on billet conversion, prompting them to divert production towards finished steel instead.

Rebar demand was sluggish, as most government infrastructure projects have either been completed or are nearing completion, while no significant new projects have been announced ahead of the upcoming state assembly elections next year.

According to a leading scrap supplier, HMS (80:20) was traded in the range of INR 28,000-29,000/t, with price realisations largely influenced by payment terms. Ongoing liquidity constraints continued to dampen market sentiment, resulting in moderate trade volumes. Meanwhile, most mills held finished steel inventories equivalent to 15-20 days of sales, reflecting muted demand and cautious procurement activity in the near term.

Regional comparison

In the western India-based Jalna market, rebar, and HMS (80:20) prices remained unchanged d-o-d at INR 42,200/t, and INR 29,000/t, respectively. Meanwhile billet prices rose by INR 200/t to INR 37,200/t.Trade activity improved in today’s session, though most deals were concluded at lower offers as buyers remained hesitant to accept higher quotes. Scrap inflows at prevailing prices continued to adequately meet mills’ production requirements, keeping overall supply conditions stable.

Outlook

Market participants expect domestic scrap prices to remain largely stable in the near term, as suppliers continue to resist lower offers amid steady procurement needs. Minor price fluctuations of INR 200-500/t may occur, keeping overall market sentiment range-bound and cautious.

Leave a Reply