- Tight domestic scrap supply supports prices

- Billet prices drop by INR 200/t d-o-d

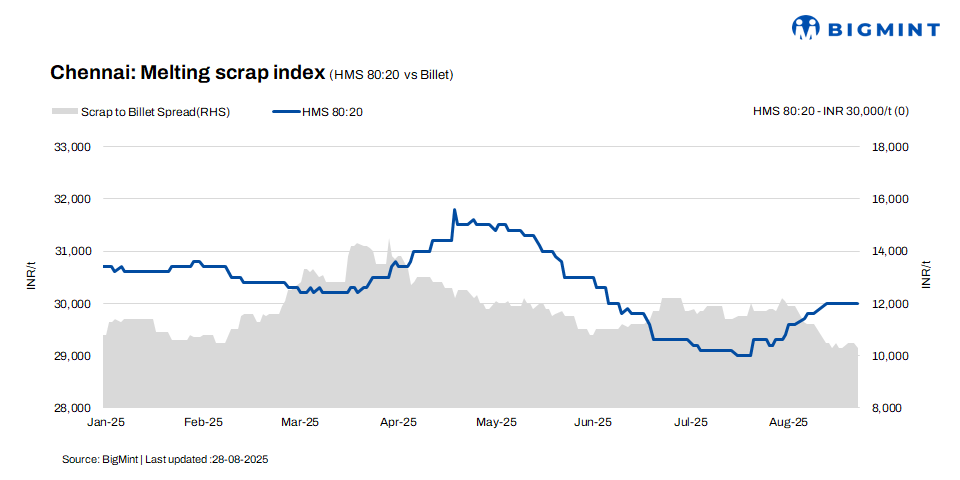

According to BigMint’s latest assessment, HMS (80:20) scrap prices in Chennai remained steady at INR 30,000/t, showing no movement on a day-on-day (d-o-d) or week-on-week (w-o-w) basis. While rebar prices held steady at INR 45,500/t on both d-o-d and w-o-w evaluations. Conversely, billet prices registered a decline of INR 200/t to INR 40,300/t, reflecting uniform downward movement on both daily and weekly terms. The overall market sentiment indicates a mixed trend, with price stability dominating daily trades and only marginal fluctuations seen over the course of the week.

Imported, domestic price trends

A scrap trader reported that offers for shredded scrap from Australia are currently in the range of $365-370/t CFR Chennai, while HMS 80:20 is being quoted at $345-350/t. According to market sources, two vessels has been beached in Chennai port, containing imported scrap in recent days. While heard that Malaysia origin 500 t of NTP bales booked at $370/t CFR Chennai.

In the Chennai market, domestic HMS (80:20) scrap is currently trading at INR 30,000-30,500/t for spot transactions involving immediate payment. For trades with extended credit terms, prices are slightly higher, ranging between INR 30,500-31,000/t. The market trend indicates that most offers and concluded deals fall within the broader INR 30,000-31,000/t range, highlighting the influence of liquidity preferences and credit-based pricing dynamics.

Buyer-supplier sentiments

According to a mill representative, billet offers have remained largely stable over the past few days, with sellers holding back material instead of accepting lower bids. This price firmness is primarily due to the fact that many large billet suppliers also operate re-rolling mills, allowing them to prioritize internal consumption over selling at discounted rates. Additionally, rebar demand has weakened recently, affecting overall trade activity in the steel sector.

On the raw material front, sponge iron prices have remained relatively unchanged, with buyers increasingly preferring locally sourced sponge due to concerns over the quality of material from neighboring states. This stability in billet and sponge iron prices, combined with lower rebar demand, signals a cautious market sentiment, which could impact future trading patterns.

According to a local scrap supplier, domestic HMS (80:20) scrap prices are currently ranging between INR 30,000 and INR 31,000/t, with slight fluctuations depending on payment terms. Despite a slight shortage in domestic scrap supply, the slowdown in finished steel trade activity over recent days has led market participants to anticipate that scrap prices will remain range-bound in the near term. This range-bound outlook suggests a relatively stable pricing environment for scrap, though external factors like steel demand may influence longer-term trends.

Regional comparison

In the Jalna market in western India, rebar, and HMS 80:20 prices remained steady at INR 43,500/t, and INR 30,800/t, respectively. While billet prices inched up by INR 200/t to INR 39,500/t. Recent days have seen a slowdown in trade activities for finished steel in the region. On the raw material side, scrap arrivals at mills remain moderate, with suppliers showing resistance to lower price levels, limiting supply.

Outlook

Market sources indicate that scrap prices are expected to remain range-bound, with likely fluctuations of INR +/- 500/t in the short term. This stability is being driven by continued uncertainty in finished steel trade, where both buyers and sellers are taking a cautious approach. The resulting sentiment is limiting volatility and keeping the market within a narrow pricing band.

Leave a Reply