- Interest in imported scrap remains low

- Uncertainty in steel segment affects scrap market

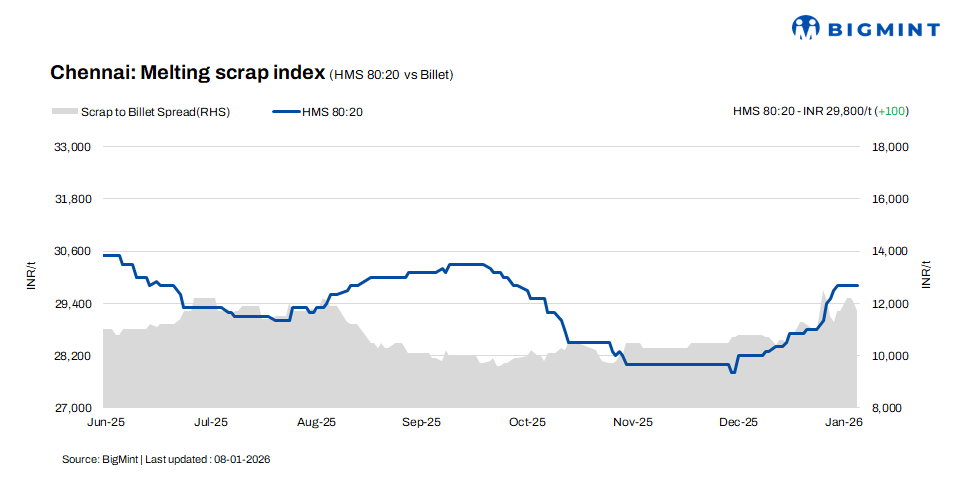

According to BigMint’s latest assessment, HMS (80:20) scrap prices in Chennai increased by INR 100/t w-o-w to INR 29,800/t, while remaining stable d-o-d. Billet prices witnessed a d-o-d correction of INR 300/t to INR 41,500/t, but recorded a w-o-w increase of INR 500/t. Rebar prices remained stable both d-o-d and w-o-w at INR 45,000/t.

Despite the upward price movement, trade activity remained moderate, as both buyers and suppliers continued to adopt a cautious approach.

Imported, domestic market trends

Market participants indicated that imported shredded scrap was offered at $340-342/t CFR Chennai, while HMS (80:20) scrap was quoted at $320-322/t. Buyers were bidding $5-7/t lower. Buying interest remained subdued, as domestic scrap prices continued to offer better cost viability than imported material, thereby limiting fresh bookings.

HMS (80:20) scrap prices in the domestic market were quoted at INR 29,500-30,000/t for spot deals with immediate payment. Transactions involving extended payment terms were concluded at higher levels of INR 30,000-30,500/t. Market activity remained largely concentrated within the INR 29,500-30,500/t band, with the majority of trades concluded at these levels.

Buyer-supplier sentiments

According to a mill source, the sponge iron merchant market is witnessing low participation, with a limited number of sellers present and muted buying interest. In the billet market, buyers remain cautious and are refraining from aggressive bookings, even as billet and rebar prices have risen in recent weeks. Demand conditions, however, continue to hover at moderate levels.

Rebar demand from infrastructure projects and the retail segment is also reported to be moderate. Inventory levels across mills stand in the range of 12-17 days, depending on current production levels.

A scrap supplier indicated that HMS (80:20) scrap prices are currently hovering in the range of INR 29,500-30,500/t, with variations primarily driven by payment terms and mill-specific volume requirements. With the Pongal festival scheduled for next week, market participants anticipate a slowdown in trade activity across the steel value chain.

Regional comparison

In the western India-based Jalna market, HMS (80:20) scrap prices edged down by INR 100/t to INR 30,400/t, while billet prices declined by INR 400/t to INR 42,500/t. Rebar offers also fell by INR 300/t to INR 49,300/t. The market witnessed a slowdown in finished steel demand compared with the previous week, which weighed on steel price offers. Additionally, mills currently hold scrap inventories aligned with operational requirements.

Outlook

According to market participants, domestic scrap prices are likely to trade within a narrow range in the short term, with fluctuations largely capped at INR +/-500/t. Persistent uncertainty in the finished steel segment has prompted a cautious approach from both buyers and sellers, dampening overall trade momentum. This subdued market environment is expected to keep scrap prices stable with limited volatility.

Leave a Reply