- Scrap prices range-bound amid weak liquidity

- Billet and rebar prices fall by INR 200/t d-o-d

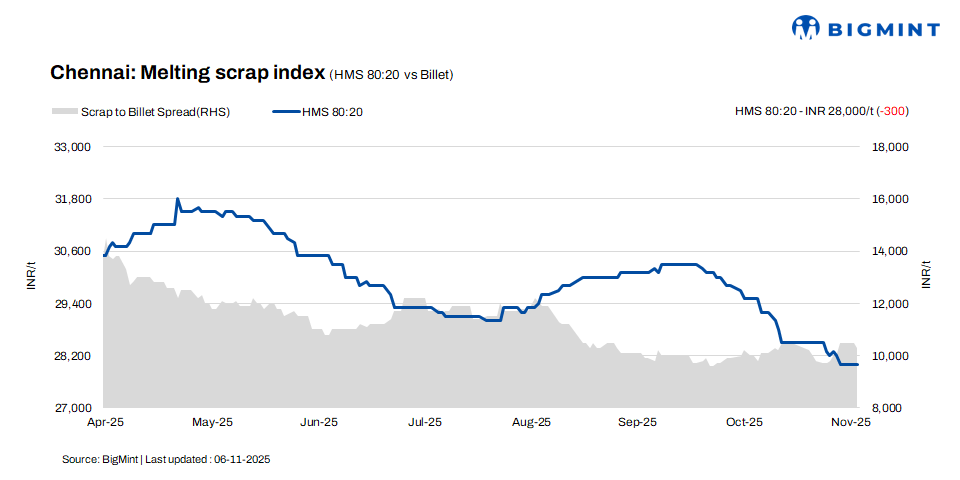

According to BigMint’s latest assessment, HMS (80:20) scrap prices declined by INR 300/t w-o-w to INR 28,000/t in Chennai, while remaining unchanged d-o-d. Billet prices held steady at INR 38,300/t on a weekly basis but slipped by INR 200/t d-o-d. Similarly, rebar prices dropped by INR 200/t to INR 43,000/t d-o-d, while remaining stable w-o-w.

The market continues to face pressure from liquidity constraints, with billet and rebar demand at average levels, reflecting a cautious buying trend across regions.

Imported, domestic scrap market trends

Imported shredded scrap offers were reported in the range of $355-360/t CFR Chennai, while buyers’ bids were slightly lower at $345-348/t, maintaining a $5-10/t bid-offer spread. HMS (80:20) scrap was quoted at $330-335/t, with bids around $325-328/t.Market participants reported a deal for Israel-origin HMS (80:20) at $322/t CFR Chennai and another deal for PNS scrap at $343/t CFR Chennai.

In the domestic market, HMS (80:20) scrap prices were reported in the range of INR 28,000-28,500/t for buyers opting for immediate payments, while extended payment terms fetched slightly higher offers of INR 28,500-29,000/t, highlighting a steady pricing environment.

Market sentiment remains cautious as traders focus on liquidity management and flexible payment structures, with both buyers and suppliers maintaining a balanced stance amid subdued but stable trading activity.

Buyer-supplier sentiments

Market participants reported that even though sponge iron prices have softened, overall trade volumes remain low as mills and buyers increasingly opt for scrap, which currently offers better cost efficiency. Large producers are channelling billets into finished steel production instead of selling them in the open market, as direct billet sales are offering limited margins. Finished steel demand remains sluggish in the retail segment, though moderate buying interest has been observed from the project sector.

According to a leading scrap supplier, HMS (80:20) scrap traded within the range of INR 28,000-29,000/t, with realizations varying based on payment terms. Persistent liquidity constraints continue to weigh on market sentiment, keeping trade volumes moderate. With the onset of the monsoon season in the region, buyers are exercising caution in fresh bookings, particularly for finished steel, as uncertain weather and transportation challenges add to near-term market hesitancy.

Regional comparison

In the western India-based Jalna market, rebar, and HMS (80:20) scrap prices remained unchanged at INR 42,500/t, and INR 29,000/t, respectively. While billet prices rose by INR 100/t to INR 37,100/t. Trade activity witnessed a mild slowdown in recent sessions, though scrap availability at mills remains stable. Market sources suggest a stable outlook for the region, with limited near-term volatility expected as supply-demand dynamics indicate a continuation of range-bound pricing.

Outlook

Market participants expect domestic scrap prices to remain largely stable in the near term, as suppliers resist offering material at lower rates. Imported scrap and sponge prices continue to trade at a premium compared to domestic levels, providing cost support to local suppliers. The market may witness minor fluctuations of INR 200-500/t in the short term.

Leave a Reply