- Market slows due to Deepawali, monsoon

- Billet, rebar prices fall by INR 300/t w-o-w

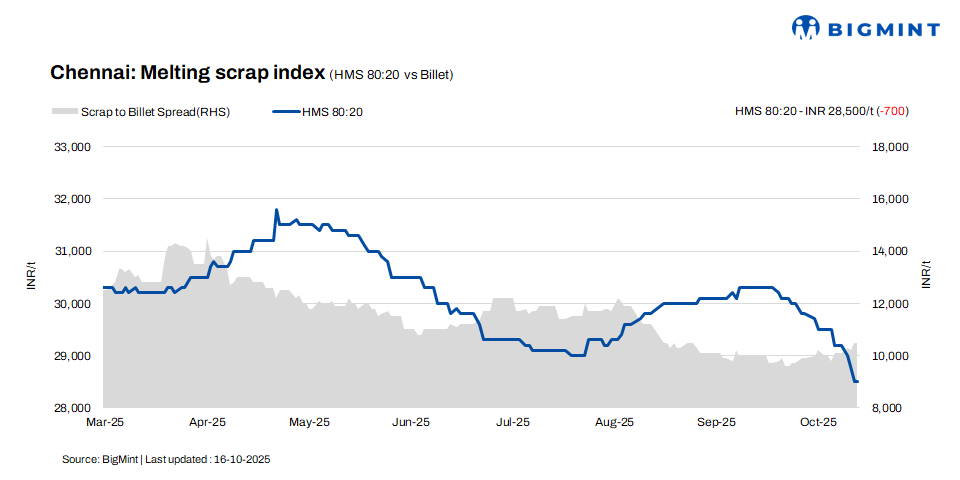

As per BigMint’s latest assessment, HMS (80:20) prices in Chennai remained steady at INR 28,500/t, with no d-o-d variation, though they declined by INR 700/t on a w-o-w basis. Similarly, billet prices decreased by INR 300/t w-o-w, settling at INR 39,000/t, while d-o-d, tags remained stable. Rebar prices also saw a w-o-w drop of INR 300/t, reaching INR 43,500/t, while remaining firm on a d-o-d basis.

Imported, domestic market trends

According to a scrap trader, imported shredded offers were quoted at $350-355/t, while buyers bid lower at $340-345/t. HMS (80:20) offers stood at $335-340/t, with bids ranging between $325-330/t, leading to a $5-10/t bid-offer gap. Market sentiment remained weak amid the ongoing monsoon season and sluggish demand from the finished steel segment.

In the domestic market, HMS 80:20 prices ranged between INR 28,500-29,000/t for buyers offering payment within seven days. Some buyers pushed to lower levels to INR 28,000-28,500/t, attributing their stance to reduced demand for finished materials. For extended payment periods, prices climbed to INR 29,000-29,500/t. Most offers remained steady at INR 28,500-29,500/t, with transactions largely taking place in this range.

Buyer-supplier sentiments

A mill owner stated that steel trade activity has slowed ahead of the Deepawali festival, resulting in limited market movement. He expects a marginal decline in finished steel prices in the near term. Additionally, the onset of the monsoon season dampened market sentiment, affecting both logistics and construction demand. According to sources, mills in Chennai held around 15-20 days of finished steel inventory, reflecting cautious buying and slower offtake in the region.

A leading scrap supplier highlighted that HMS (80:20) was traded in the range of INR 28,500-29,500/t, depending on payment terms. Liquidity constraints kept trading activity muted in recent weeks, while weak billet and rebar demand prompted mills to reduce scrap procurement prices to manage conversion costs. With the Deepawali festival approaching and the monsoon setting in, market participants expect further softness in steel prices in the near term.

Regional comparison

In the western India-focused Jalna market, billet, rebar, and HMS (80:20) prices remained stable d-o-d at INR 39,300/t, INR 43,500/t, and INR 30,800/t, respectively. Trading activity in finished steel was limited, with buyers largely inactive ahead of the Deepawali festival. Market sources revealed that some mills have either halted production or implemented production cuts amid weak demand. Although scrap arrivals have slowed and offers are slightly lower, current supply levels remain adequate to support ongoing mill operations.

Outlook

Market participants expect scrap prices to hold steady or register a slight dip of nearly INR 200-500/t in the coming days. With the Deepawali holidays ahead, reduced trading in finished steel is expected to keep overall market sentiment subdued and may exert mild downward pressure on prices.

Leave a Reply