- Scrap prices fall, market activity slows

- Steel prices dip as market remains cautious

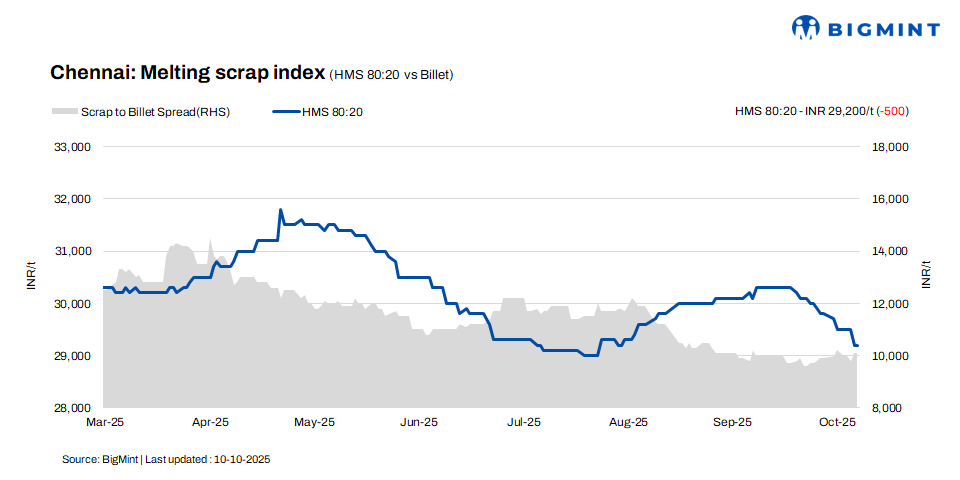

According to BigMint’s latest assessment, HMS (80:20) scrap prices have dropped by INR 500/t w-o-w, bringing the cost down to INR 29,200/t in Chennai. However, prices remained unchanged d-o-d. Similarly, billet prices experienced a decrease of INR 400/t, settling at INR 39,300/t w-o-w, while d-o-d prices remained stable. Rebar prices also saw a drop of INR 200/t, reaching INR 43,800/t w-o-w, while remained firm on daily basis.

Market sentiment remains cautious as trade activity continues at an average pace, reflecting limited buying interest amid ongoing demand uncertainty in the regional steel sector.

Imported, domestic market trends

According to a scrap trader, imported shredded scrap offers are currently quoted at $350-355/t, while buyers are bidding lower at $340-345/t. HMS (80:20) scrap offers are reported at $325-330/t, with bids around $320-325/t, maintaining a $5-10/t bid-offer gap. The overall market sentiment remains weak, pressured by the ongoing monsoon season and subdued demand expectations from the finished steel segment, which continues to dampen near-term trading activity and price momentum.

In the domestic market, prices for HMS 80:20 scrap were recorded between INR 29,000-29,500/t for buyers who were offering payment within seven days. For extended payment terms, prices rose to INR 29,500-30,000/t. The majority of offers remained stable within the INR 29,000-30,000/t range, and transactions predominantly occurred within this pricing range. Market participants are adopting a cautious stance, with bids being aligned according to liquidity conditions and payment schedules.

Buyer-supplier sentiments

A mill representative informed BigMint that mills in Chennai, operating at around 80% capacity, are currently able to sell just over 50% of their finished steel output. This has led to an accumulation of inventories at mill yards. With the monsoon season nearing, buyers remain hesitant to make fresh bookings. As Chennai’s coastal geography makes it prone to heavy rains and cyclones, both construction activity and transportation are expected to face disruptions in the coming weeks.

A scrap supplier reported that HMS (80:20) scrap prices in Chennai are currently ranging between INR 29,000-30,000/t, depending on payment terms. The slowdown in finished steel demand has weighed on overall trade activity. Additionally, a labor shortage has emerged as many workers from northern India are on leave since the Navratri festival and are expected to return only after Deepawali, further constraining operations and affecting material movement in the local market.

Regional comparison

In the western India–based Jalna market, HMS (80:20) scrap prices declined by INR 200/t to INR 28,700/t, while billet and rebar offers remained stable at INR 37,300/t and INR 42,700/t, respectively. According to market sources, several mills have initiated production cuts due to sluggish finished steel demand. Mills are currently holding around 15-20 days of finished steel inventory, and with the upcoming Deepawali festival expected to slow construction activity further, market participants anticipate limited improvement in steel demand in the near term.

Outlook

Market sources indicate that scrap prices should hold stable in the immediate term, with potential movement confined to INR 200-300/t. The forthcoming Deepawali holiday period is expected to reduce trading activity in finished steel, leading to subdued market sentiment. As demand temporarily eases, a mild adjustment in scrap prices is possible, though broader market fundamentals suggest continued short-term price stability.

Leave a Reply