- Firm outlook for scrap despite moderate demand

- Billet prices increase by INR 550/t w-o-w

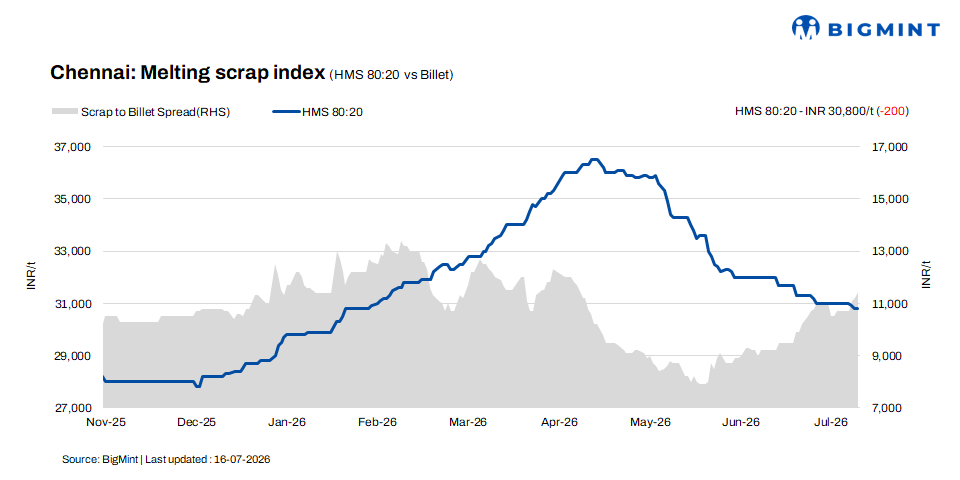

According to BigMint’s latest assessment, HMS (80:20) scrap prices in Chennai remained stable at INR 30,800/t, with no change on a d-o-d basis, although they declined by INR 200/t w-o-w. In the semi-finished segment, billet prices increased by INR 250/t d-o-d to INR 42,250/t, registering a weekly gain of INR 550/t.

Meanwhile, rebar prices also rose by INR 200/t to INR 46,000/t on both a daily and weekly basis. Despite the recovery in billet and rebar prices, finished steel demand remained average, while liquidity constraints continued to weigh on overall market sentiment and trading activity.

Imported and domestic price trends

According to market participants, Australia-origin shredded scrap was offered at $365–370/t CFR Chennai, while HMS (80:20) was quoted at $335–340/t CFR. However, buyers continued to quote bids around $20-25/t below prevailing offers, highlighting weak import demand. Despite shortage of domestic scrap, mills remained reluctant to book imported cargoes due to the wide bid-offer gap and cautious procurement amid subdued finished steel demand.

In the domestic market, HMS (80:20) scrap prices were quoted at INR 30,500–31,000/t for spot transactions, while credit-term deals were concluded at INR 31,000–31,500/t. Overall, trading activity remained concentrated within the INR 30,500–31,500/t range, supported by balanced supply conditions. However, subdued demand from the downstream steel sector kept buying sentiment cautious, with transaction prices primarily influenced by payment terms and mill-specific volume requirements.

Buyer-supplier sentiments

A mill representative shared with BigMint that sponge iron consumption has increased in recent weeks as mills seek to offset the impact of constrained domestic scrap availability. Although scrap supply remains tight, imported scrap continues to be priced above domestic material, making it unviable and limiting fresh import bookings.

The representative also noted that demand for billet and rebar has improved modestly supported by stronger trading activity and firm prices in neighbouring states. The improvement in regional steel prices has strengthened market sentiment, encouraging mills and suppliers to raise their offer prices, even as procurement continues on a cautious and requirement-based basis.

A scrap supplier told BigMint that HMS (80:20) scrap prices are currently ranging between INR 30,500–31,500/t, depending on payment terms and mill-specific requirements. Despite subdued sentiment in the steel sector, tight domestic scrap availability has prevented mills from significantly lowering their procurement prices.

The supplier added that higher imported scrap offer levels have curtailed fresh bookings, resulting in lower import arrivals and further tightening domestic supply. Consequently, the combination of restricted imports and limited local scrap availability continues to support domestic scrap prices despite weak finished steel demand.

Outlook

The Chennai scrap market is expected to remain stable-to-firm in the near term, supported by tight domestic scrap availability and limited imported scrap arrivals. However, mills are likely to continue need-based procurement amid only moderate finished steel demand. Any upside is expected to be capped by liquidity constraints, with price movements likely to remain within INR +/- 200-500/t.

Leave a Reply