- Domestic prices face competition from cheaper imports

- China’s domestic, ZCE futures prices decline

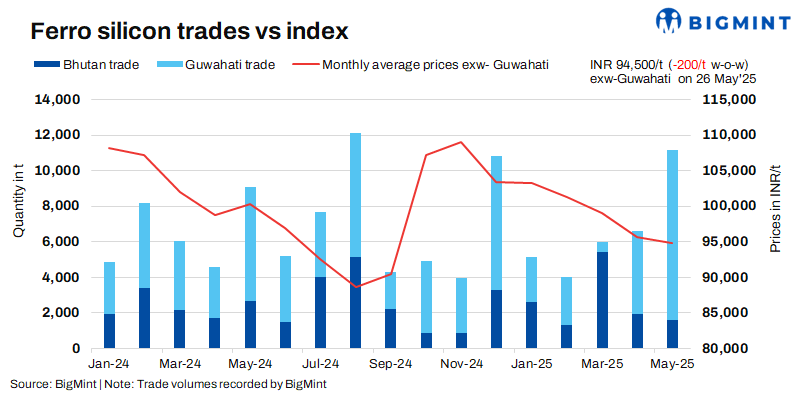

Indian ferro silicon (70%) prices remained largely stable last week, moving down slightly by INR 200/t ($2/t) in comparison to the assessment on 19 May 2025. Prices held steady as inquiries were limited and the majority of market players were looking forward to next month’s price announcement from Bhutan.

As per BigMint’s assessment on 26 May, ferro silicon prices in India were INR 94,500/t ($1,108/t) exw-Guwahati. In Bhutan, prices edged down by INR 300/t ($4/t) w-o-w to INR 95,000/t ($1,114/t) exw. Around 2,100 t of deals were concluded in both regions last week within the price bracket of INR 94,000-95,000/t ($1,102-1,114/t) exw.

Market recap (20-26 May 2025)

Cost-effective imports limiting domestic demand: A key domestic buyer with a monthly procurement of around 4,000 t, informed BigMint recently, “There is lot of material coming in from Russia nowadays and it is available in the domestic market at around INR 93,000-93,500/t ($1,090-1,096/t) exw levels.”

Despite this, sellers in both the North-east and Bhutan held on to their offers and discounts were offered mostly for bulk orders. Prices were also steady as many sellers were sold out for the month, which limited supplies.

South India’s price trends: Sellers in south India were offering primarily in the range of INR 95,000-96,000/t ($1,096-1,125/t) exw levels. Around 250 t of trades were also reported in that price range.

Decline in Chinese prices: Ferro silicon (Si:75%) prices in China inched down by RMB 130/t ($18/t) w-o-w to RMB 6,040/t ($838/t) exw-Inner Mongolia· Although demand recovery was slow, the market remained optimistic about an upcoming improvement in demand, backed by positive macroeconomic conditions.

Inventories continued to accumulate, prompting traders to adopt a cautious stance with controlled shipments and timely profit realisations. End-user demand gradually strengthened, supported by increased inquiries from downstream sectors. Overall, inventory levels were manageable, and the market was expected to remain stable.

On the Zhengzhou Commodity Exchange (ZCE), prices dropped by RMB 184/t ($26/t) w-o-w to RMB 5,506/t ($764/t) on 26 May for July deliveries.

Outlook

Prices are expected to stay rangebound in the days ahead with some variations. Bhutan’s offers for June are expected to be announced next week which will further determine the price trajectory.

Leave a Reply