- Molybdenum supply constrained by China, Chile mine disruptions

- Low deals in India seen as buyers remain price-sensitive

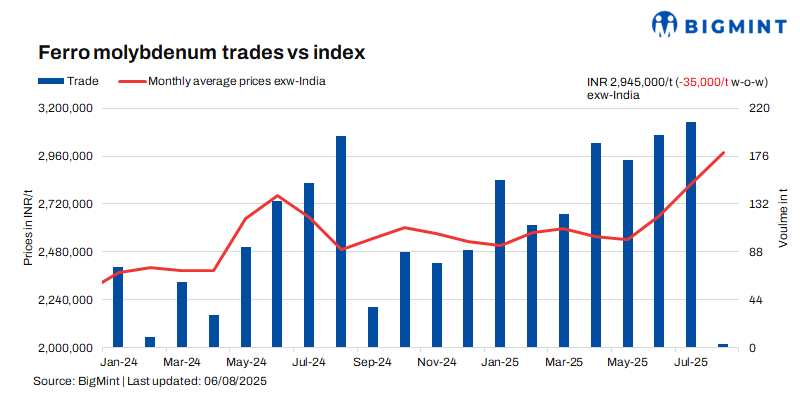

Indian ferro molybdenum prices stayed largely rangebound last week, moving down slightly by INR 35,000/t ($399/t) compared to the last assessment on 30 July 2025. Tight supplies in the domestic market along with good demand kept prices supported.

Ferro molybdenum prices in India stood at INR 2,945,000/t ($33,588/t) exw-India, as per BigMint’s assessment on 6 August. Approximately 15 t of deals were reported to BigMint last week in the price range of INR 2,900,000-3,016,000/t ($33,074-34,397/t) exw.

Market highlights (31 July-5 August)

Raw material supply constraints: The supply of molybdenum concentrates remained constrained on and has been tightening steadily since late June 2025, driven by rising demand across Asia and unchanged production levels. Reliable sources indicated recent accidents at mining sites in China and Chile, leading to full or partial shutdowns, further strengthening market expectations of continued short-term tightness in the spot market.

Global market trends: Ferro molybdenum (Mo:60%) prices in China declined by RMB 7,000/t ($974/t) w-o-w to RMB 268,500/t ($37,374/t) exw-Inner Mongolia. Prices dipped slightly despite growing demand from sectors like construction, military, and new energy vehicles. While steel companies showed increased purchasing interest, fluctuating molybdenum prices made downstream users more price-sensitive, resulting in cautious buying. The market remained largely steady, with major steel mills making purchases, but overall demand was weak.

In the US and Europe (Mo:70%), prices edged up by $2/t w-o-w to $57/kg and $56/kg, respectively.

On the London Metal Exchange (LME) as well, molybdenum futures contract prices inched up marginally by $0.52/lb w-o-w to $23.96/lb on 5 August.

Limited supplies supporting Indian prices: With the molybdenum oxide shortage persisting in the domestic Indian market as well, offers from sellers were largely steady. The usual negotiations and supply-demand dynamics caused some fluctuations but overall market was largely rangebound.

Buyers, however stayed cautious in procuring material leading to lesser deals in the last week.

Outlook

Prices in the coming days are expected to stay supported as there is no sign of easing raw material supplies, both in the global and domestic market.

Leave a Reply