- Wide bid-offer disparities impact trading

- Bids firm at FACOR’s ferro chrome auction

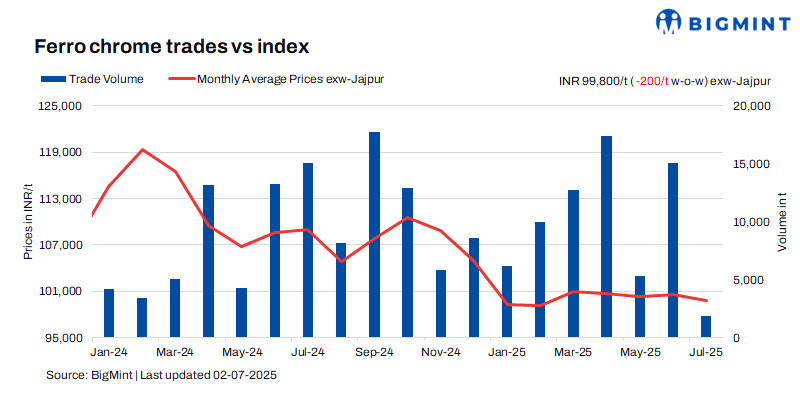

Indian high-carbon ferro chrome (HC60%, Si:4%) prices edged down by INR 200/tonne (t) ($2/t) w-o-w to INR 99,800/t ($1,167/t) exw-Jajpur on 2 July — reaching their lowest point in over four months, last seen on 21 February 2025, as per data maintained with BigMint.

Prices edged down amid cautious buying, stemming from widening bid-offer disparities. Trades for around 2,000 t were concluded last week within the price range of INR 99,500-100,000/t ($1,164-1,170/t) exw.

For low-silicon high-carbon and low-carbon (C:0.1%) ferro chrome, prices fell too, by INR 900/t ($11/t) and INR 1,000/t ($12/t) w-o-w to INR 104,300/t ($1,220/t) exw-Jajpur and INR 199,000/t ($2,328/t) exw-Durgapur, respectively. For low-silicon high-carbon ferro chrome, trades for 700 t were recorded within INR 104,000-104,500/t ($1,216-1,222/t) exw-Jajpur.

Market summary (26 June – 2 July 2025)

Cautious sentiments dominate market: Most buyers expected further price drops, but sellers stood firm on their offers. Bids were at INR 99,000/t ($1,160/t) or less, while offers stood at above INR 100,000/t ($1,172/t). The same sentiment was echoed at yesterday’s ferro chrome auction by Vedanta-FACOR. In that, the bigger lot of 10-150 mm fetched an H1 price of INR 99,200/t ($1,159/t) exw, slightly above the base price of INR 99,000/t ($1,157/t) exw. Bids were steady as against the previous auction on 23 June.

A key domestic seller recently informed BigMint, “Ferro chrome prices might remain supported as chrome ore mining will be lower during monsoons. There is a possibility of more aggressive bidding at the upcoming chrome ore auction by OMC.”

TISCO’s tender price sees slight drop: China’s Taiyuan Iron and Steel Corporation (TISCO) reduced its July ferro chrome tender price by RMB 50/t ($7/t) m-o-m to RMB 7,845/t ($1,095/t) DAP, including taxes.

The Chinese domestic market remained mostly stable, supported by firm raw material costs and controlled inventories, despite sluggish demand in the off-season. Supply rose as some plants resumed operations, but output remained cautious to match weak demand from stainless steel mills. Stable chrome ore prices and limited high-grade ore imports from Zimbabwe provided cost support.

The market is expected to remain range-bound, with firm costs limiting downside but soft demand capping any significant price gains.

European benchmark price rises q-o-q: Samchrome recently announced its European benchmark price at 145 cents/lb for Q3CY’25, up by 5 cents/lb from the previous quarter.

Slight uptick in stainless steel prices: Prices of 304-grade stainless steel hot-rolled coils (HRCs) edged up by INR 2,000/t ($23/t) w-o-w to INR 184,000/t ($2,157/t) exw-Mumbai. Overall demand remained weak, with secondary mills operating at 60-70% of their capacity. Infrastructure activity also progressed slowly, limiting market recovery. With weak buying activity and limited movement expected until August, stainless steel prices are likely to remain range-bound, though sentiment may improve post-monsoon.

Outlook

A slight correction in prices might be seen in the days ahead, considering ongoing bid-offer gaps in the market.

Leave a Reply