- Vedanta-FACOR auction records nearly 2,000 t bookings

- Stainless steel demand stays muted across key markets

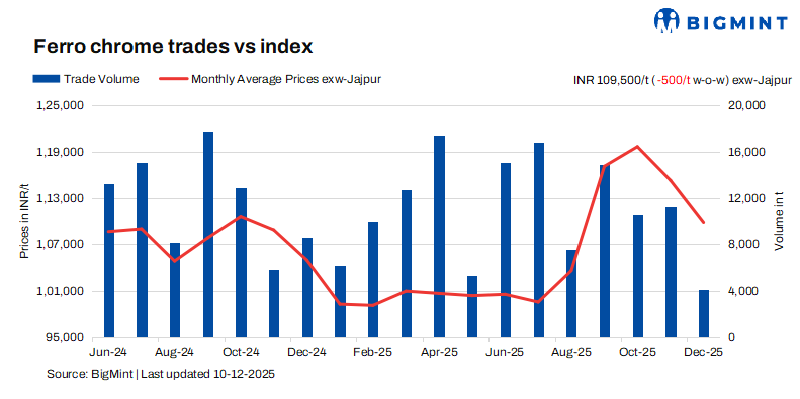

Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices fell by INR 500/t ($5/t) w-o-w on 10 December, in comparison to the assessment on 3 December. Prices stayed firm as sellers kept offers steady and buyers remained cautious, while weak end-user demand further weighed on market sentiment.

As per BigMint’s assessment on 3 December, high-carbon ferro chrome (HC 60%, Si 4%) prices in India stood at INR 109,500/t ($1,213/t) exw Jajpur. Around 1,700 t of deals were concluded last week within the price range of INR 108,000-109,000/t ($1,197–1,208/t) exw.

Prices for low-silicon high-carbon ferro chrome eased by INR 1,600/t ($17/t) w-o-w to INR 114,000/t ($1,263/t) exw Jajpur. Low-carbon ferro chrome (C:0.1%) also edged down by INR 200/t ($2/t) w-o-w to INR 208,000/t ($2,305/t) exw Durgapur. For low-silicon ferro chrome, around 660 t was traded last week within the range of INR 113,000–114,000/t ($1,252–1,263/t) exw.

Market summary (4 – 10 December)

Market sentiment muted on cautious buying: The domestic ferro chrome market remained quiet last week due to a bid-offer disparity. Sellers maintained firm offers and were unwilling to sell below INR 110,000/t ($1,218/t) exw. Meanwhile, buyers stayed cautious amid ample material availability in the market and adopted a wait-and-watch approach. This imbalance limited trading activity and kept overall market sentiment subdued.

In addition, Vedanta-FACOR’s ferro chrome auction on 10 December saw bookings of around 2,000 t. The larger lot (Cr 57% min, 10–150 mm) achieved an H1 price of INR 107,500/t ex-works, in line with the base price, while the smaller lot fetched INR 108,800/t,up INR 800/t from the base price.

Subdued market across end-user sector: India’s stainless steel prices for 304-grade HRC remained unchanged w-o-w at INR 180,000/t ($1,994/t) exw Mumbai. The market stayed muted this week, with soft demand and slow off-take keeping activity subdued across both flats and longs. Prices held within a narrow range as mills maintained limited raw material procurement, while active imports from Southeast Asia continued to pressure domestic offers.

Despite announcements of new capacities and improved sales at a few producers, overall sentiment remained weak. In the near term, the stainless steel market is expected to stay subdued due to weak end-user demand and year-end caution. Price pressure is likely to persist amid adequate inventories, import competition, and slow downstream off-take.

Chinese market remains stable w-o-w: Ferro chrome (HC60%) prices in China held steady w-o-w at RMB 8,300/t ($1,175/t) exw Inner Mongolia. With chromium ore supply remaining sufficient due to strong overseas shipments, although slow port inventory continued to weigh on prices. Producers remained cautious in ore procurement, purchasing only on a need basis, while stable coal prices had minimal impact on production costs.

Stable stainless steel production kept ferro chrome consumption steady, with alloy and tool steel sectors also maintaining consistent long-term buying. However, overall purchasing interest remained moderate, as downstream buyers stayed cautious and continued to adopt a wait-and-see approach.

Outlook

Ferro chrome prices are expected to remain largely unchanged over December, as soft stainless steel demand and sufficient material availability are likely to limit the scope for any significant price movement.

Leave a Reply