- Auction bids drop, market impact yet to show

- China’s tender prices steady amid weak demand

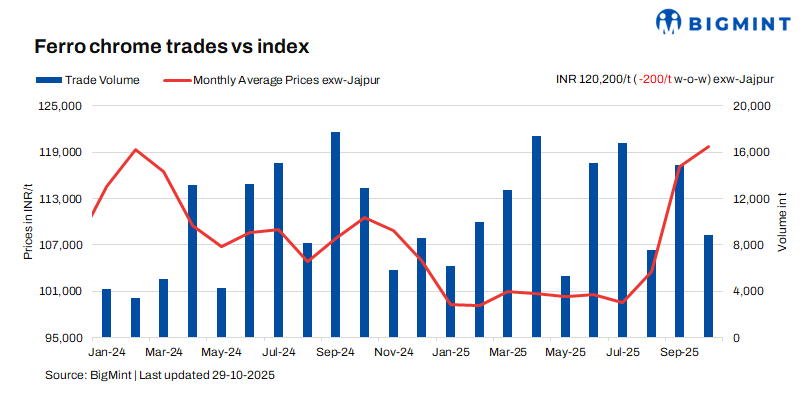

Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices stayed largely stable over the last week, moving down slightly by INR 200/t ($2/t) as against the previous assessment on 24 October. Routine trades in the domestic market kept prices relatively stable.

High-carbon ferro chrome (HC 60%, Si: 4%) prices in India were INR 120,200/t ($1,357/t) exw-Jajpur, as per BigMint’s assessment on 29 October. Around 2,000 t of deals were concluded last week in the price range of INR 118,500-120,500/t ($1,338-1,361/t) exw.

Low-silicon high-carbon ferro chrome prices dipped by INR 700/t ($8/t) w-o-w to INR 125,300/t ($1,415/t) exw-Jajpur. Approximately 900 t of deals were concluded for it in INR 124,500-125,000/t ($1,406-1,412/t) exw. Meanwhile, low-carbon ferro chrome (C:0.1%) prices edged up by INR 700/t ($8/t) w-o-w to INR 212,700/t ($2,402/t) exw-Durgapur.

Market recap (23-29 October)

Deals keeping prices steady: Ferro chrome trades were finalized in a steady range last week, keeping market prices largely unchanged. Out of around 2,000 t traded, nearly 1,800 t of deals were concluded in the INR 120,000–120,500/t ($1,355-1,361/t) exw range. With the market resuming post-holidays, buying interest stayed limited as most key buyers had already booked material for the month.

Meanwhile, in a ferro chrome auction held yesterday, bids for the larger 10–150 mm lot were INR 115,100/t ($1,300/t) exw, down by INR 5,700/t ($64/t) from the previous auction on 8 October, while the smaller lot received bids of INR 116,100/t ($1,311/t) exw. The auctioned material was of 52–54% grade, with bids on a 60% pro-rata basis, so the actual market impact remains to be seen in the coming days.

China’s domestic and tender prices stable: After TISCO, Tsingshan kept its ferro chrome tender prices stable m-o-m at RMB 8,495/t ($1,197/t) DAP, inclusive of taxes, for November deliveries.

Chinese HC60% prices edged down w-o-w by RMB 200/t ($28/t) to RMB 8,600/t ($1,211/t) exw-Inner Mongolia. Prices edged lower during the week amid weak demand from the stainless steel sector and cautious buying by steel mills. The chrome ore market stayed under pressure as labour disputes in South Africa tightened port inventories, but limited buying by ferro chrome producers made it hard for miners to sustain prices. Although regional price changes were minor, declining cost support further reduced producers’ margins. Sluggish stainless steel demand, slower growth in the new energy sector, and weaker high-end manufacturing consumption together kept overall market sentiment subdued.

Subdued end-user market: Stainless steel prices for 304 grade HRC edged down by INR 4,000/t ($45/t) w-o-w to INR 186,000/t ($2,101/t) exw-Mumbai. Demand for finished longs remained subdued with minimal trade activity and weak buying sentiment, particularly in Gujarat, where normal operations were yet to resume. Finished flats demand was stable, though prices showed little upward movement. Imports from Vietnam were active and priced higher than Chinese offers, which remained limited due to BIS certification issues. Overall, weak demand suggests continued near-term market softness.

Outlook

Ferro chrome prices are expected to undergo a downward correction in the coming days as seen in recent auctions and subdued demand from the stainless steel segment.

Leave a Reply