- Limited seller offers, tight supply help keep prices firm

- Stainless steel demand weak; possible revival post monsoon

Indian high-carbon ferro chrome (HC60%, Si:4%) prices were unchanged as compared to the previous assessment on 9 July. Prices held steady, as the market was mostly quiet ahead of the upcoming chrome auction by OMC on 19 July.

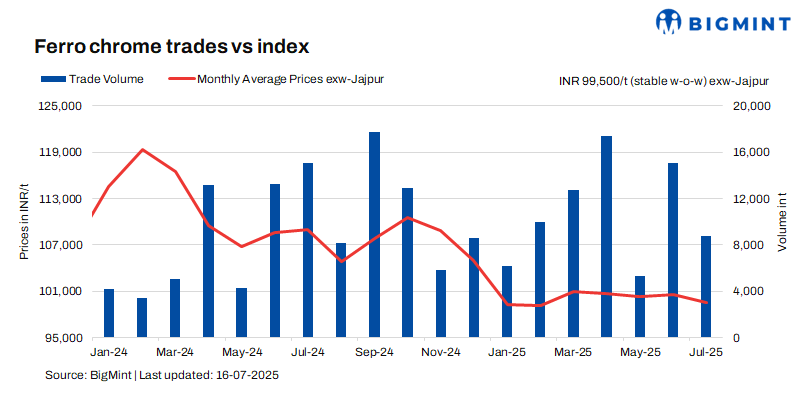

High-carbon ferro chrome (HC60%, Si:4%) prices in India were at INR 99,500/t ($1,158/t) exw-Jajpur, as per BigMint’s assessment on 16 July. Trades for approximately 2,000 t were reported last week in the price range of INR 99,500-100,000/t ($1,158-1,164/t) exw.

Prices of low-silicon high-carbon and low-carbon (C:0.1%) ferro chrome were stable as well, at INR 103,400/t ($1,203/t) exw-Jajpur and INR 198,300/t ($2,307/t) exw-Durgapur, respectively.

Market summary (10-16 July 2025)

Limited offers keep supplies tight: The ferro chrome market over the last week largely stayed silent, as most sellers were already booked. They also looked forward to the results of the Odisha Mining Corporation (OMC) chrome ore auction, as offers are usually revised based on the price trends seen there.

Due to this, supplies were slightly limited, but with firm offers, prices were supported. A seller recently informed BigMint, “Our bookings are almost done for this month. Additionally, there might be limited participation in the upcoming auction, as some have switched their furnaces to manganese alloys.”

Chinese prices remain stable: Ferro chrome (HC60%) prices in China were unchanged w-o-w at RMB 7,850/t ($1,093/t) exw-Inner Mongolia. Imports declined due to high inventories and reluctance from steel mills to pay high ore prices. Kazakhstan’s high-grade ferro chrome remained costly, pushing some mills towards local sourcing.

Real estate and machinery sectors remained sluggish, and rising anti-dumping tariffs had an impact on exports. In the near term, prices may stay range-bound as oversupply and weak demand might continue.

Stainless steel prices edge up: Prices of stainless steel 304-grade hot-rolled coils (HRCs) saw a slight uptick of INR 1,000/t ($12/t) w-o-w to INR 185,000/t ($2,153/t) exw-Mumbai. Finished flats showed mixed price trends, while longs held steady due to limited spot demand and no new project drivers. Buyers mostly adopted a wait-and-watch approach, expecting clearer pricing signals after the monsoons. The longs segment was supported by regular quarterly orders, but a lack of infrastructure-led demand capped any price rise.

Overall, demand is expected to stay weak through July, with a possible revival post-monsoon, depending on liquidity and raw material price trends.

Outlook

Prices in the coming days are likely to stay range-bound with slight variations. Trends will become clearer following OMC’s chrome auction on 19 July.

Leave a Reply