- OMC cuts base price by 6% for auction

- Stainless steel prices edge up slightly

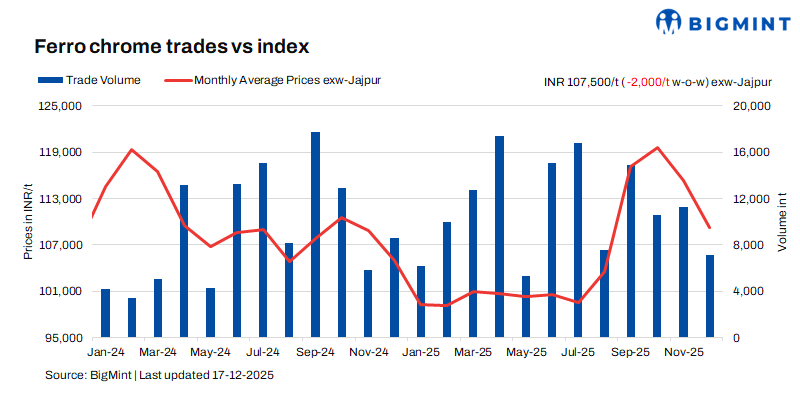

High-carbon ferro chrome (HC 60%, Si: 4%) prices in India witnessed a drop of INR 2,000/t ($22/t) as compared to the last assessment on 10 December. Prices fell as trading activity stayed limited ahead of the upcoming chrome ore auction by OMC.

High-carbon ferro chrome (HC 60%, Si: 4%) prices in India were INR 107,500/t ($1,192/t) exw-Jajpur, as per BigMint’s assessment on 17 December. Around 700 t of spot deals were concluded last week in the price range of INR 107,000-108,000/t ($1,187-1,198/t) exw.

Prices edged down for low-silicon high-carbon and low-carbon (C:0.1%) ferro chrome by INR 2,000/t ($22/t) and INR 500/t ($6/t) w-o-w to INR 112,000/t ($1,242/t) exw-Jajpur and INR 207,500/t ($2,301/t) exw-Durgapur, respectively.

Market recap (11-17 December)

Muted trades ahead of OMC’s chrome ore auction: Market activity remained largely muted last week as inquiries stayed limited and buyer bids were lower, resulting in very few trades. Weak buying interest exerted downward pressure on overall market rates. Key domestic producers preferred diverting material toward export markets, where realisations were comparatively better. The recent depreciation of the Indian rupee further supported export profitability, encouraging sellers to prioritise overseas shipments over domestic sales.

Another major factor contributing to subdued market sentiment was the wait-and-watch approach adopted by participants ahead of OMC’s upcoming chrome ore auction. The auction, scheduled for tomorrow, is for 106,800 t of material. Base prices for grades above 40% have been reduced by 6% m-o-m (INR 1,286-1,736/t), while below 40% grades have seen a marginal cut of around INR 30/t.

Mixed sentiments in stainless steel market: Stainless steel prices for 304 grade HRC saw a slight uptick of INR 2,000/t ($22/t) w-o-w to INR 182,000/t ($2,019/t) exw-Mumbai following a hike announced by a leading producer. Additional support came from a $30/t price increase by Tsingshan and expectations around China’s new export licence regime effective from January. Tight raw material availability, global cost pressures, and selective price hikes by domestic mills supported flat products, despite cautious sentiment amid year-end slowdown and global trade uncertainties.

In contrast, stainless steel longs weakened due to sluggish downstream demand, lower buying interest, and mills focusing on inventory clearance. Adequate scrap availability and cost-effective grade conversion further weighed on prices. Overall, the market is expected to stay subdued until demand improves after mid-January.

China market scenario: Ferro chrome (HC60%) prices in China moved up by RMB 300/t ($43/t) w-o-w to RMB 8,600/t ($1,221/t) exw-Inner Mongolia. Prices edged higher over the week on rising cost pressures from chrome ore and volatile coke prices, along with expectations of tighter export policies from South Africa. However, demand remained mixed as buyers adopted a cautious procurement approach, keeping overall sentiment stable.

In the downstream segment, stainless steel producers continued operating at high levels, sustaining demand, though off-season consumption limited buying enthusiasm. Increased inquiries from the special steel and new energy sectors offered selective support, particularly for low-carbon ferro chrome. Despite these factors, buyer activity stayed measured, and prices are likely to remain rangebound in the near term.

Outlook

With the OMC’s chrome ore auction scheduled for tomorrow, ferro chrome price trends are expected to become clearer next week.

Leave a Reply