- Bids drop by INR 1,200/t at FACOR’s auction

- Tsingshan’s tender price remains steady m-o-m

Indian high-carbon ferro chrome (HC60%, Si:4%) prices decreased slightly by INR 400/tonne (t) ($5/t) as compared to the assessment on 18 June. Prices fell following a drop in bids at major auctions last week by the Odisha Mining Corporation (OMC) for chrome ore and Vedanta-FACOR for ferro chrome.

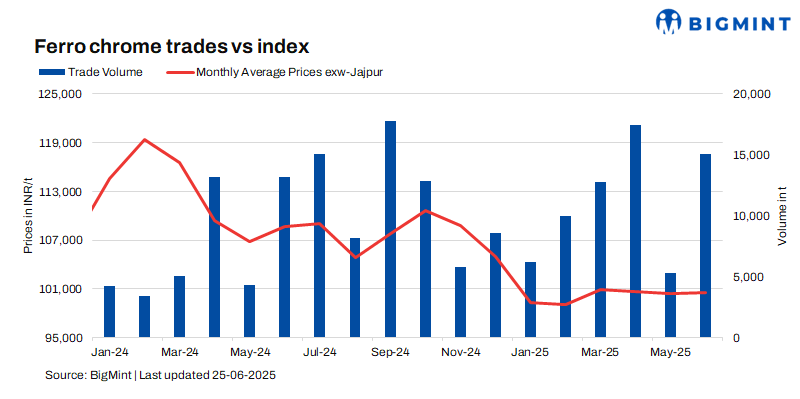

As per BigMint’s assessment on 25 June, high-carbon ferro chrome (HC60%, Si:4%) prices in India were at INR 100,000/t ($1,166/t) exw-Jajpur. Around 5,600 t of material were traded last week in the price bracket of INR 98,500-101,000/t ($1,149-1,178/t) exw.

For low-silicon high-carbon and low-carbon (C:0.1%) ferro chrome, prices fell too, by INR 800/t ($9/t) and INR 2,000/t ($23/t) w-o-w to INR 105,200/t ($1,227/t) exw-Jajpur and INR 200,000/t ($2,332/t) exw-Durgapur, respectively.

Market recap (19-25 June 2025)

Recent auctions see moderate response: At OMC’s chrome ore auction on 19 June, 50,500 t were booked out of the 76,000 t offered. Bids for Cr2O3 >48% grades (barring COBO, JK Road material) fell sharply by 21-32% (INR 5,658-11,027/t) m-o-m. Meanwhile, other grades saw a slight rise of 1-2% (INR 51-432/t).

A similar response was seen in Vedanta-FACOR’s ferro chrome auction on 24 June. In that, the bigger lot of 10-150 mm fetched an H1 price of INR 99,200/t ($1,157/t) exw, down by INR 1,200/t ($14/t) from the previous auction on 13 June.

Market sentiments, therefore, weakened, and buyers became reluctant towards higher offers. Commenting on this, a seller stated, “We are offering material at INR 101,000-102,000/t ($1,178-1,189/t) exw, but counters from buyers are at around INR 100,000/t ($1,166/t) exw or less.”

China sees steady tender prices: Tsingshan rolled over its tender price for July shipments at RMB 8,095/t ($1,128/t) DAP, including taxes. While spot prices in the Chinese market were lower w-o-w and chrome ore tags declined, market sentiments stabilised to a certain degree with the announcement of the steady tender price.

The domestic market faced pressure due to weak stainless steel demand and reduced bidding by major mills. Supply was also impacted by rising power costs in Inner Mongolia and cautious production strategies. Chrome ore prices remained volatile, with South African quotes under pressure and Turkish ores firm. Additionally, downstream stainless steel markets weakened further, with declining demand from China, Europe, and Southeast Asia, as buyers reduced inventories ahead of summer.

Indian stainless steel market remains stagnant: Prices of 304-grade stainless steel hot-rolled coils (HRCs) were unchanged w-o-w at INR 182,000/t ($2,122/t) exw-Mumbai. The market stayed under pressure due to weak demand, lack of infrastructure projects, and the onset of monsoon, which slowed down construction activities. Mills were also heard to be running at 60-70% of their capacity, and further production cuts may occur if demand does not recover. In the near term, stainless steel prices are expected to remain range-bound, considering current market conditions.

Outlook

Bid-offer gaps seem to be widening, which might prompt slight corrections in prices in the days ahead.

Leave a Reply