- UG-origin G4 triggered extreme premiums, distorting overall auction price structure

- Lower offer quantity tightened competition for cleaner high-CV parcels

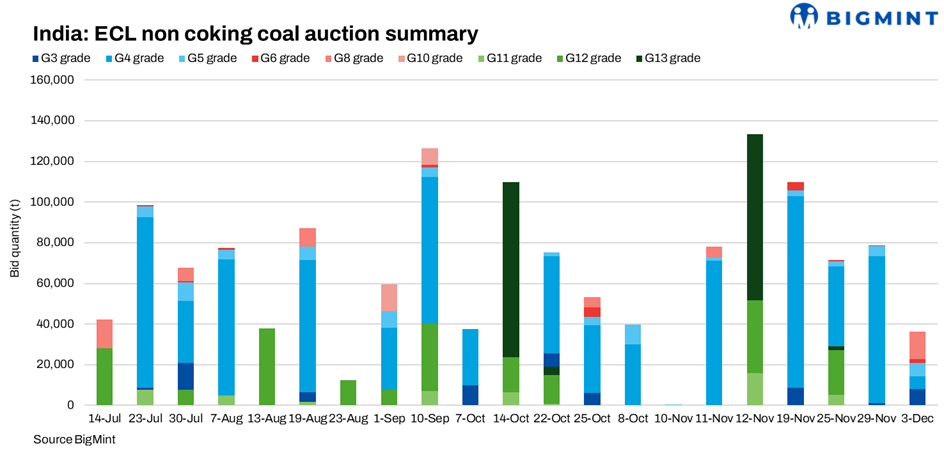

Eastern Coalfields Ltd (ECL) sold 36,300 t of non-coking coal in its 3 December 2025 auction, much lower than 78,800 t sold on 29 November. Despite the smaller volume, the auction witnessed extreme premium volatility, driven mainly by rare UG-origin G4 parcels. The market also stayed alert ahead of ECL’s next auction on 16 December, offering 1,019,700 t across G3, G4, G5, G6, G12, G13.

Grade-wise performance: G4 premium skyrockets; G9 leads volumes

G9 (4,600-4,900 GCV) formed the bulk of the sale with 13,550 t at INR 1,772/t, reflecting steady mid-low CV demand.

G3 (6,400-6,700 GCV) supply increased from 900 t on 29 Nov to 8,000 t, but cleared at a much lower INR 4,638/t, compared to INR 4,674/t earlier, reinforcing balanced but cautious demand for high-CV grades.

The most striking development was in G4 (6,100-6,400 GCV)-although only 6,200 t were offered, one UG-source parcel fetched an extraordinary INR 10,840/t, sharply above last auction’s stable levels of INR 4,510-4,486/t. This single premium outlier lifted the overall grade average to INR 6,794/t, distorting the price structure and signaling extreme scarcity for superior UG-origin lots.

G5 (5,800-6,100 GCV) recorded 6,800 t at INR 4,087/t, softer than last auction’s INR 5,213/t, as more OC-origin supply tempered bid aggression.

G6 (5,500-5,800 GCV) cleared 1,750 t at INR 3,780/t, broadly aligned with the 29 Nov outcomes.

Mine-wise allocations: UG-origin parcels drive unprecedented price spikes

Supply this round was dominated by OC mines such as G/Begunia OC (13,550 t of G9 at INR 1,772/t) and Chitra OC (8,000 t of G3 at INR 4,638/t).

However, UG mines shaped the auction narrative:

Nimcha UG delivered a 1,500 t G4 parcel at INR 10,840/t – the highest price seen across the past two auction cycles.

Narsamuda UG cleared 3,000 t G4 at INR 5,193/t, well above typical OC ranges.

Smaller UG parcels from Shyamsundarpur, Methani and others fetched INR 4,437-4,447/t, underscoring consistent preference for low-ash output.

Compared with the previous auction, UG-origin influence grew disproportionately, pushing certain G4 premiums far above normalised levels.

Buyer-wise allocations: selective procurement amid volatile premiums

GREENOSPHERE RENEWABLE ENERGY emerged as the top buyer with 4,000 t of G9, highlighting continued appetite for mid-CV economical grades.

SS Enterprises secured 1,850 t at INR 4,526/t, staying active across premium segments similar to prior rounds.

Other buyers such as Grasim Industries, Ranisati Coal Carriers, and Vaishnavi Enterprises selectively targeted high-CV parcels, with Vaishnavi booking small but high-priced volumes at INR 5,177/t.

Participation remained diversified but cautious, especially after sharp premium volatility observed in G4.

Market scenario: sharp premium divergence; UG-origin scarcity dominates sentiment

The latest auction revealed:

Stronger premiums for select UG-origin parcels, most dramatically in G4, distorting typical CV-based pricing.

Mid-CV grades (G5, G6) corrected slightly versus 29 Nov as OC-sourced supply improved.

High-CV (G3) demand stayed firm but rational, avoiding the extreme premiums witnessed in late November.

Lower offer quantity (36,300 t vs 78,800 t earlier) intensified bidding competition for cleaner UG lots.

Compared with the 29 November auction, this round showed a far more uneven premium structure, driven almost entirely by the extremely limited and high-quality UG-origin G4 parcels.

Note: All prices mentioned above are exclusive of GST, additional statutory taxes, and freight charges.

Leave a Reply