- Stronger participation for mid- and low-grade coal

- Firm bidding for G4 seen, sharp jump in G11-G13 allocations

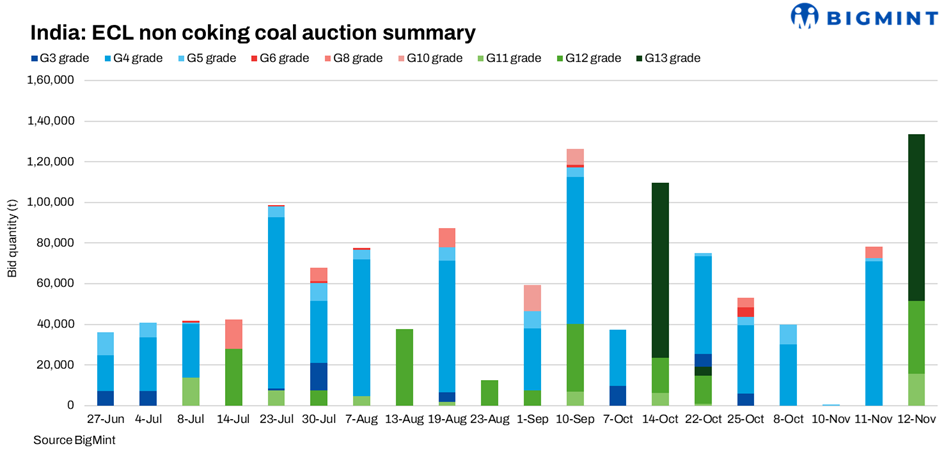

CIL subsidiary Eastern Coalfields Ltd (ECL) sold a combined 270,550 t of non-coking coal across four auctions held on 8, 10, 11 and 12 November 2025, reflecting active interest in G4, G5 and lower-grade (G9-G13) coal. Auctions on 8 and 11 November drew the strongest participation, while the 10 November event was limited to a small G5 parcel. Overall sentiment appeared firm for G4 and mixed for G5, while low-grade coal such as G11-G13 saw large allocations at lower bid levels.

8 Nov auction: Strongest activity, 39,850 t sold

The 8 November auction recorded 39,850 t of sales with active bidding for G4 from multiple underground (UG) and opencast (OC) mines including Jhanjra UG, Nakrakonda OC, Shyamsundarpur UG, Chitra OC and Khottadih OC.

G4 volumes dominated, often clearing at INR 4,437-4,737/t, with pockets touching INR 4,807/t.

Buyers: Neelkanth Sales & Logistics (6,000 t at INR 4,487/t), RCB Minerals (5,300 t at INR 4,512/t), Mark Trading Co. (2,500 t at INR 4,587/t), Iconic Coal Co., Vaishnavi Enterprises, Maa Bhawani Coal Trader, Laxmi Narayan Enterprises, Ranisati Coal Carriers, and several mid-sized regional buyers.

G5 grades (mainly from Amkola OC and Barmuri OC) saw higher bids in the INR 4,724-4,884/t range due to smaller parcels. Small allocations from various collieries indicate wide geographic distribution of supply.

10 Nov auction: Only 500 t sold

This was a small-volume auction comprising only 500 t of G5 from Gopinathpur MDO.

All buyers paid a uniform INR 4,084/t, with participation from several small traders (Ganpati Coal Traders, JPB Traders, Kashinath Enterprise, Uttam Kumar Mondal).

The small size reflects limited supply offering, but stable demand for G5.

11 Nov auction: 78,200 t sold

The auction on 11 Nov recorded one of the largest single-day sales: 78,200 t.

G4 dominated, led by a massive 65,000 t allocation from Sonepur Bazari OC, clearing at an average INR 4,601/t.

Other G4 supplies: Shankarpur UG (6,000 t at INR 5,445/t), Kumardihi A UG (100 t at INR 4,437/t), showing a wide variance in pricing depending on mine and demand pockets.

G5 grades (Bejdih UG, Rajpura OC, Khoodia UG, Shyampur B UG) cleared at INR 4,084-4,394/t.

G9 from G/Begunia OC saw significant volume (5,500 t) at INR 1,772/t, highlighting realistic pricing for lower-quality fuel.

Top buyers: Maharaja (9,600 t), Mark Trading Co. (8,000 t), Reet Sales (8,000 t), Neelkanth (7,000 t), Ranisati Coal Carriers (4,100 t).

12 November auction: 151,500 t sold

The 12 November auction delivered 151,500 t, the largest allocation across the four auctions.

This event was driven by huge G11-G13 supplies, especially from Rajmahal OC and Hura C OC.

Grade-wise highlights

G11: 15,750 t from Hura C OC at INR 2,151/t

G12: 35,850 t from Rajmahal OC at INR 2,068/t

G13: 81,850 t from Rajmahal OC at INR 1,713/t

G3: 7,700 t from Chitra OC at INR 4,638/t, reflecting strong demand for higher-grade material

G4: 3,350 t from Kumardihi B UG, Kalidaspur UG, Dhemo Pit UG at INR 4,437/t

G5: 4,650 t from Chora Block UG, Lakhimata UG etc. at INR 4,099-4,325/t

G6: 2,650 t from Badjna UG & Mohanpur OC at INR 3,024-3,780/t

Buyer activity

Adani Power Ltd booked the largest share: 75,000 t of G13 at INR 1,713/t

Sponge iron and thermal power buyers such as Sundaram Steels, Vision Sponge Iron also participated for G11-G12

Mixed participation observed across G3-G6 due to varying demand across industries

Market scenario

G4 remained the most actively traded medium-grade coal at all the auctions, clearing steadily at INR 4,437-4,737/t.

G5 demand stayed consistent at INR 4,084-4,884/t, especially when parcel sizes were small.

Low-grade coal (G9-G13) saw massive allocations, especially on 12 November, at INR 1,700-2,200/t, indicating strong demand from thermal power and cost-sensitive industrial users.

Large-volume buyers (Adani Power, Maharaja, Mark Trading, Reet Sales) dominated mid- and low-grade segments.

Pricing volatility across grades reflected mine-to-mine variation, parcel size, and buyer concentration.

Takeaway

In the four auctions ECL allocated 270,550 t, with strong demand visible for G4, stable interest for G5, and very heavy offtake of G11–G13 by power sector consumers. The auctions demonstrated broad-based participation from both large industrial buyers and regional traders, with prices closely aligned to grade quality and mine location.

Leave a Reply