- South Africa-India rates plunge $2/dmt w-o-w on thin activity

- Spot fixing activity expected to remain weak until early Jan’26

Global dry bulk coal freight markets extended their downward trajectory in the week ended 26 December 2025, as rates on key routes into India remained under sustained pressure amid declining cargo volumes, ample tonnage availability, and increasingly cautious buying sentiment ahead of the year-end period.

Freights on the Australia-India, South Africa-India, and Indonesia-India corridors continued their weak run, with limited fresh fixing activity and growing competition among shipowners. This softness weighed on both Panamax and Supramax segments, dragging indices to lower levels and reinforcing the bearish near-term outlook for coal freight markets.

“Asia-Pacific Panamax freights moved within a narrow range, with limited positive movement observed across the region. Out of Australia, fixture activity remained scarce, as muted cargo availability and cautious chartering interest constrained fresh enquiries. With ample tonnage open and few new stems emerging, rates showed little impetus to move higher, keeping the market broadly steady,” a source informed BigMint.

Another ship-broker said, “Market sentiment remains slightly bearish amid the ongoing holiday period, with activity expected to thin out further in the near term. Freights could face additional marginal pressure as alternate cargo supply becomes available and fixing remains limited. While many owners are likely to re-enter the market more actively after 1 January, near-term support appears thin unless charterers require prompt spot tonnage, in which case isolated fixtures may still emerge.”

Coal freights on the Australia-India route remained under pressure this week, with the market struggling to find a floor amid persistently weak fixing activity and abundant open tonnage. Spot enquiries stayed limited, and the absence of fresh cargo stems prevented any meaningful rebound from last week’s six-month lows. While some owners attempted to hold offers steady, competition among vessels and cautious chartering interest continued to cap rates. Muted demand from India’s steel sector, coupled with comfortable inventories and subdued price expectations, further dampened sentiment, leaving the route vulnerable to additional downside in the absence of a clear demand trigger.

Freights on the South Africa-India route remained weak this week, consolidating near recent lows, as cargo volumes stayed thin, and vessel availability continued to outpace demand. Fixing activity was very thin, with charterers largely stepping back amid cautious buying sentiment, while owners faced sustained competition from readily available tonnage.

Similarly, Supramax freights on the Indonesia-India route stayed under pressure this week, hovering near recent lows as fixing activity remained subdued and enquiry levels showed minimal improvement. Chartering interest from India continued to be selective, while ample open tonnage in the region kept competition among owners elevated. With no meaningful pick-up in cargo volumes and limited near-term visibility, rate ideas struggled to gain traction, leaving the market vulnerable to further softness in the absence of renewed demand.

Lower fuel costs offer limited relief as freight markets stay soft

Bunker prices remained under pressure this week, tracking continued softness in crude oil benchmarks and steady fuel availability across major global bunkering hubs. Demand from the shipping sector stayed muted amid limited trading activity and year-end slowdowns, preventing any meaningful recovery in bunker pricing. While lower fuel costs offered some marginal cost relief to owners, the impact was largely negated by persistently weak freight markets, with subdued cargo volumes and ample vessel supply continuing to weigh on overall earnings and sentiment.

Supply-heavy market maintains pressure on freights

The freight market remained tilted in favour of charterers this week, as vessel availability stayed elevated, and cargo inflows showed little sign of improvement. In the Pacific, open tonnage lists continued to lengthen, with limited fresh stems from Australia and Indonesia preventing any tightening in prompt positions. Meanwhile, the Atlantic basin remained subdued, as slower export flows and comfortable vessel supply kept owners on the defensive. With fixing activity staying patchy across basins, rate recovery remained elusive, reinforcing the softer near-term outlook.

Route-wise updates

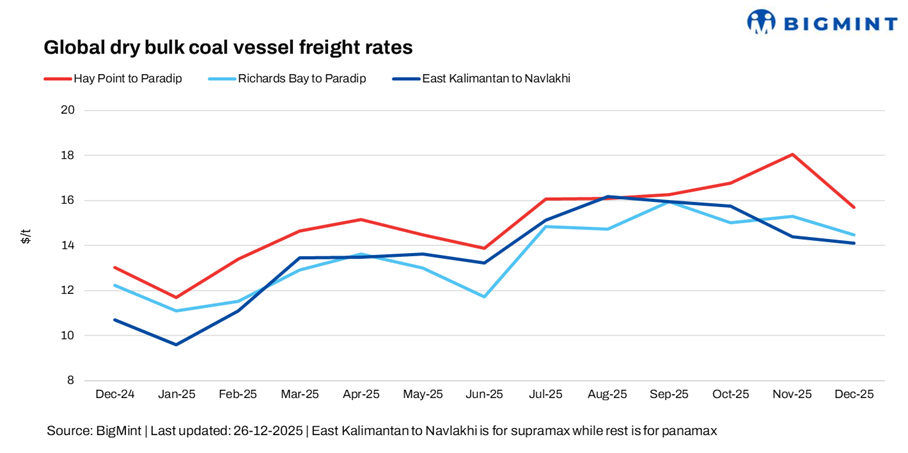

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India fell by around 1.7/dry metric tonne (dmt) w-o-w to $12.70/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route moved down sharply by $2.22/dmt w-o-w to $12.08/dmt.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route stood at $12.91/dmt, a decrease of $0.85/dmt w-o-w.

Meanwhile, the Baltic Exchange’s dry bulk index for Panamax and Supramax vessels witnessed a significant fall this week, with the Panamax index falling sharply by around 122 points w-o-w to 1,267 and the Supramax index decreasing by 114 points to 1,144. The decline in the Panamax and Supramax indices was driven by a year-end slowdown in cargo activity, weak coal demand, and ample vessel availability across basins. Limited fresh stems and thin holiday-period fixing forced owners to concede on rates, pushing indices lower.

Outlook

The near-term outlook for India-bound dry bulk coal freights remains soft, as the year-end slowdown, limited cargo enquiries, and ample vessel availability continue to weigh on rates across major routes from Australia, Indonesia, and South Africa. Panamax and Supramax segments are likely to face continued pressure, with charterers maintaining the upper hand amid muted downstream demand from India’s steel and power sectors. Spot fixing activity is expected to remain thin until early January, limiting any meaningful upward momentum.

Looking ahead into early 2026, freights may find tentative support as owners return after the holidays and charterers resume regular cargo programs. However, with high inventories in India and subdued seasonal demand, any recovery is expected to be gradual, and the market is likely to remain largely stable or slightly soft unless there is a sudden surge in cargo volumes or disruption to tonnage availability.

Leave a Reply