- Coal freights into India remain under pressure amid thin fixtures and ample tonnage

- Falling bunkers and weak FFAs reinforce bearish freight sentiment

Dry bulk coal freight markets into India opened CY’26 on a weak footing, with rates across key import corridors coming under sustained pressure amid sluggish trading activity and a lack of demand support. Sparse fixing volumes, cautious chartering sentiment, and an overhang of prompt tonnage continued to weigh on freight levels, while falling bunker prices and softer FFA markets further reinforced the bearish tone. As a result, both Panamax and Supramax segments struggled to find a floor during the week, setting a subdued tone for the early part of the year.

Coal freight rates on the Australia-India, South Africa-India, and Indonesia-India routes remained under pressure, as the market grappled with a near-complete absence of fresh fixtures and subdued participation from charterers. Weak cargo enquiry, coupled with ample prompt tonnage, intensified competition among shipowners, forcing further rate concessions across both the Panamax and Supramax segments. The lack of early-year demand recovery kept sentiment bearish, with indices drifting lower and offering little support for a near-term rebound in coal freight markets.

Falling bunker prices and weaker FFA levels added further downside pressure to the dry bulk freight market during the week. The decline in fuel costs reduced voyage expenses, enabling owners to accept lower freight rates, while softer FFAs reinforced bearish sentiment and curtailed resistance to rate erosion. Together, the pullback in bunkers and paper markets weakened pricing support across key coal corridors, keeping spot rates under pressure and limiting any near-term upside.

“The Asia-Pacific Panamax freight market remained weak amid subdued trading activity, as limited cargo enquiry kept fixing volumes thin. Out of Australia, fixture visibility was particularly poor, with minimal fresh business reported, reflecting cautious chartering appetite and a lack of demand support. The muted activity weighed on sentiment, leaving owners with little pricing leverage and keeping rates under sustained pressure”, a source informed BigMint.

Coal freights on the Australia-India route remained subdued, with the market struggling to find a floor amid limited fixing activity and ample prompt tonnage. Spot enquiries stayed thin, and the absence of fresh cargo stems prevented any recovery from recent lows. Despite some owners attempting to hold offers steady, strong vessel competition and cautious chartering interest kept rates capped, while weak steel demand and comfortable inventories in India continued to weigh on sentiment.

Freights on the South Africa-India route followed the suite and remained weak this week amid persistently thin cargo volumes and an oversupply of available tonnage. Fixing activity was minimal, as charterers stayed largely on the sidelines due to cautious buying sentiment. The imbalance between supply and demand kept rates under pressure. “Out of South Africa, no fresh fixtures were heard”, said a ship broker.

Similarly, Supramax freights on the Indonesia-India route slipped further this week as fixing activity remained muted and enquiry levels failed to improve. Selective chartering interest from India, combined with ample open tonnage in the region, intensified competition among owners and forced further rate concessions. With no meaningful pickup in cargo volumes and limited near-term visibility, downward pressure persisted, leaving the market vulnerable to additional softness.

Soft crude benchmarks and muted demand keep bunker prices under pressure

Bunker prices continued to ease this week, extending recent declines in line with softer crude oil benchmarks and comfortable fuel availability across major bunkering hubs. Demand from the shipping sector remained muted amid subdued trading activity, limiting any recovery in fuel prices. While lower bunker costs provided some marginal relief on voyage expenses, the benefit was largely offset by weak freight market conditions, with thin cargo volumes and ample vessel supply continuing to pressure overall earnings and sentiment.

Route-wise updates

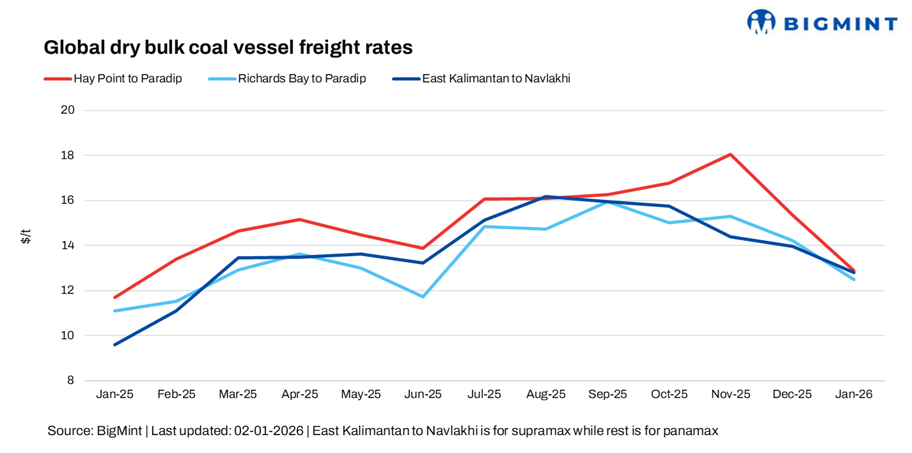

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India edged up marginally by around 0.2/dry metric tonne (dmt) w-o-w to $12.9/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route moved increased slightly by $0.42/dmt w-o-w to $12.5/dmt.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route stood at $12.8/dmt, a decrease of $0.11/dmt w-o-w.

Outlook

The near-term outlook for dry bulk coal freight into India remains bearish, as limited cargo enquiry, comfortable inventory levels, and subdued buying interest continue to weigh on demand. An overhang of prompt tonnage across key origins – including Australia, South Africa, and Indonesia – is intensifying competition among owners and keeping rates under pressure across both Panamax and Supramax segments. While lower bunker costs provide some marginal cost support, this is unlikely to translate into firmer freight levels in the absence of a clear pickup in coal imports from the power and steel sectors. As a result, freight markets are expected to remain rangebound to weaker in the near term, with any recovery dependent on a visible improvement in cargo volumes or seasonal demand.

Leave a Reply