- Weak cargo demand, rising tonnage weigh on Asia-Pacific sentiment

- Limited vessel availability, firmer bunker prices lift Indonesian rates

Dry bulk coal freights displayed mixed movements this week, with rates for the Australia-India route softening, while those for South Africa-India and Indonesia-India increased due to shifting demand-supply dynamics. Overall trading activity remained muted, suggesting potential pressure on rates in the weeks ahead.

“Asia-Pacific Panamax freights eased as weak cargo replenishment and rising tonnage weighed on sentiment. Charterers reduced bids, while some owners resisted further declines, yet fundamentals pointed to the need for more cargo to clear prompt vessels. Freight derivatives extended losses during Asian hours, even as bunker prices rose,” a ship-broker observed.

Sources noted that market confidence weakened further despite firmer tonnage demand from rising cargo volumes. In the Pacific, operators and traders pointed to a notable pick-up in fresh coal cargoes.

Another source told BigMint, “Sentiment on the Indonesia-India coal route remained firm despite limited activity, while the Atlantic market held steady even as freight derivatives slipped during late Asian trading.”

However, trades remained subdued from South Africa and Indonesia, as participants deemed freights elevated, restricting purchases largely to need-based procurement. Cautious industrial demand further kept overall coal consumption moderate.

India’s portside thermal coal inventories declined by 5.4% w-o-w to 13 millon tonnes (mnt) in Week 35 from 13.78 mnt in Week 34, weighed down by weaker arrivals. High import offers, sluggish steel market conditions, and muted domestic demand limited fresh bookings.

Route-wise updates

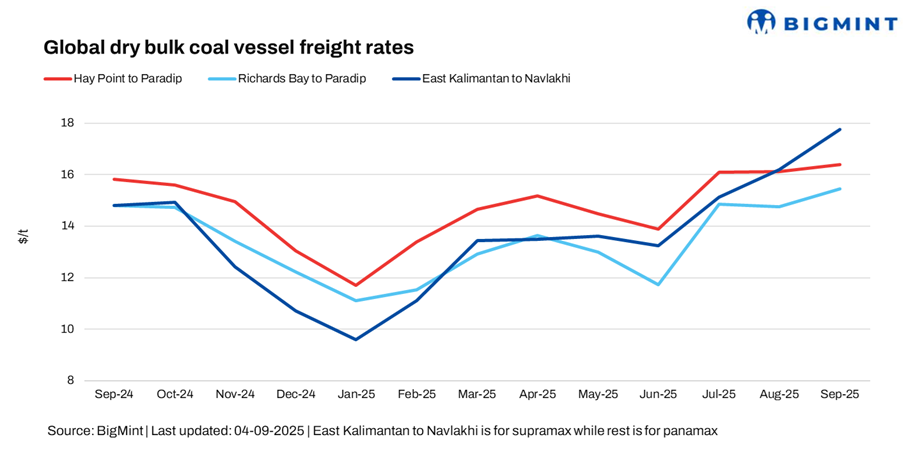

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India fell by around $0.16/dry metric tonne (dmt) w-o-w, with BigMint’s latest assessment placing the Hay Point-Paradip route at $16.38/dmt. Demand from Indian blast furnace operators continued to stay weak. Steel market sentiment stayed subdued on weak demand, with prices holding range-bound w-o-w and showing little momentum. Ongoing uncertainty kept both buyers and sellers from making significant moves.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa (Richards Bay) to India (Paradip) route increased w-o-w by $0.45/dmt to $15.45/dmt. South Africa-India coal freights remained firm as tighter tonnage in the Atlantic basin, and elevated bunker costs underpinned offers. Shipowners maintained a bullish stance, anticipating stronger returns, though charterers remained cautious, as rates were viewed on the higher side for long-haul shipments to Asia. On the South Africa-India route, a major source noted, “Market activity remained sluggish, with limited trades and weak buying interest during the rainy season. Nevertheless, elevated South African coal prices kept ocean freights firm, though overall sentiment stayed soft, with little near-term support anticipated.”

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia (East Kalimantan) to India (Navlakhi) route stood at $17.75/dmt, a significant increase of $0.8/dmt, w-o-w. Freights on the Indonesia-India route edged higher despite thin fixture activity, supported by limited vessel availability and firmer bunker prices. Owners resisted lower bids amid expectations of improved Indian coal demand, sources highlighted.

Market highlights

- Baltic index dropped w-o-w amid vessel rate pressure: The Baltic Exchange’s main dry bulk sea freight index fell on 4 September 2025 as individual vessel rates came under pressure. The overall index decreased sharply w-o-w by around 106 points to 1,940. Additionally, the Panamax segment also witnessed a significant downtrend of 155 points w-o-w to 1,719, while the Supramax segment increased by 20 points w-o-w to around 1,467, providing some support to the overall index.

- DCE coal futures stay flat w-o-w: DCE coking coal futures on the Dalian Commodity Exchange (DCE) for the January 2026 contract remained unchanged w-o-w at RMB 228/t ($32/t) on 4 September. DCE coking coal futures remained unchanged w-o-w as supply concerns from limited Mongolian inflows offset weak steel margins and subdued mill restocking demand. With market participants adopting a cautious, wait-and-watch stance, prices stayed under pressure.

Outlook

In the near term, dry bulk coal freights are likely to remain range-bound to slightly soft, with muted Asian demand and abundant vessel supply capping momentum. Firm bunker costs and occasional fixtures may offer limited support, but overall sentiment stays cautious. A Mumbai-based ship-broker noted, “The coal vessel freight market is softening, with excess vessel supply and limited cargo demand, particularly with elevated tonnage levels on India’s east coast for prompt positions.”

Leave a Reply