- Australia, South Africa rates remain firm; Indonesia declines

- Need-based cargo demand, ample vessel supply keep trade slow

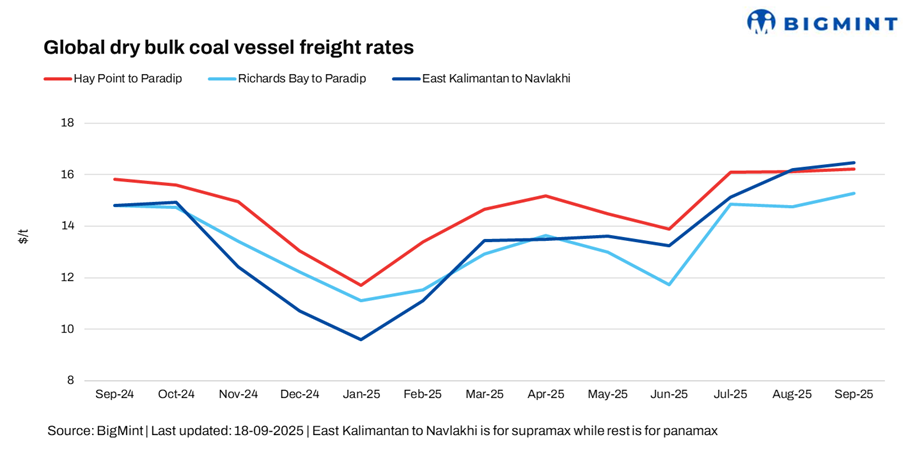

Dry bulk coal freights continued to display mixed movements this week, with rates for the Indonesia-India route softening, while those for South Africa-India and Australia-India remained unchanged. Overall trading activity stayed muted, with the Australia-India route emerging as the only active lane, though marked by volatile rates that point to possible downside pressure in the coming weeks.

“Asia-Pacific Panamax freights held stable to slightly softer as sentiment stayed cautious amid prevailing market uncertainties, with trading activity remaining sluggish through the week. However, freight derivatives gained during Asian hours and bunker prices moved notably higher, offering a measure of optimism,” a source told BigMint.

Meanwhile, with market fundamentals largely favouring sellers, shipowners were initially quoting elevated offers and holding firm against fixing closer to charterers’ bids.

Another source told BigMint, “Asia-Pacific Supramax freights held largely steady to softer, with the trading week opening on a subdued note across regions.”

Trades from South Africa and Indonesia stayed muted as participants considered freights still elevated, limiting purchases mainly to need-based requirements. Additionally, cautious industrial demand kept overall coal consumption moderate.

India’s portside thermal coal inventories dipped 1.8% w-o-w to 11.88 million tonnes (mnt) in Week 37 from 12.10 mnt in Week 36, marking a six-month low, provisional BigMint data showed. Sluggish arrivals, coupled with muted demand from steel and sponge iron producers, curbed fresh bookings, while elevated import offers and weak trading activity further limited portside replenishment.

Route-wise updates

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India remained stable at $16.12/dry metric tonne (dmt). SAIL was actively fixing vessels this week, but construction and infrastructure activity in India has slowed under the impact of heavy monsoons, labour shortages, and logistics challenges. Procurement stayed minimal, as overall market sentiment remained weak.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa (Richards Bay) to India (Paradip) route also remained unchanged at $15.20/dmt. “South Africa saw no fresh coal inquiries or fixtures during Asian trading hours,” observed a charterer. Another charterer said, “South Africa’s coal freights remain high despite limited fixtures, driven by structural factors. The long South Africa–China route ties up vessels, while scarce tonnage and costly ballast voyages from the Pacific support rates. Ongoing rail and port bottlenecks add risk premiums, and with few fixtures, even small deals can keep headline rates firm.“

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia (East Kalimantan) to India (Navlakhi) route stood at $15.71/dmt, a decrease of $0.25/dmt w-o-w. The drop in Indonesia–India vessel freights this week was mainly due to oversupply of ships and softer export demand, which increased competition among carriers. Economic factors such as fluctuating fuel costs also added pressure, leading to the observed decline in rates.

Market highlights

- Baltic index hits 2-month high on vessel gains: The Baltic Exchange’s main dry bulk sea freight index increased on 18 September 2025 as individual vessel rates witnessed a w-o-w increase. The overall index rose sharply by around 240 points w-o-w to 2,180. Additionally, the Panamax segment also witnessed a significant uptrend of 204 points w-o-w to 1,923, while the Supramax segment increased by 25 points w-o-w to around 1,492, providing further support to the overall index.

- DCE coal futures drop w-o-w: DCE coking coal futures on the Dalian Commodity Exchange (DCE) for the January 2026 contract decreased by RMB 13/t ($2/t) w-o-w to RMB 215/t ($30/t) on 18 September. DCE coking coal futures dropped this week due to a mix of profit-taking after recent gains, stricter trading limits imposed by the exchange to curb speculation, and concerns of oversupply amid weaker demand from downstream coking plants.

Outlook

The near-term outlook for dry bulk coal vessel freight to India from Australia, South Africa, and Indonesia is expected to remain soft to range-bound. Freights are likely to face pressure from moderate import demand, ongoing competition among exporters, and relatively ample vessel availability, which limits upside for charterers.

However, occasional spikes in demand –– driven by seasonal power generation needs or opportunistic cargoes — could provide brief support to rates. Overall, market sentiment is likely to stay cautious, with small fluctuations rather than sustained moves in either direction.

Leave a Reply