- Ample tonnage supply, limited enquiries pressure freights

- Rising bunkers lift voyage costs, squeezing shipowners’ margins

Dry bulk coal freight markets into India remained under sustained pressure during the week, as weak demand fundamentals and ample vessel availability continued to overshadow any supportive cues. Sparse fixing activity across major origins, coupled with cautious chartering interest, kept rates on a downward trajectory. Rising bunker prices and softer paper market signals further strained owner margins, reinforcing bearish sentiment and contributing to lower rates across Panamax and Supramax segments.

The absence of a meaningful early-year demand recovery kept market sentiment bearish, with the market facing heightened pressure during the week as multiple macro and market signals turned unfavourable. An increase in bunker prices, due to a hike in crude oil futures, increased voyage costs, squeezed shipowners’ margins. At the same time, weaker FFA curves and the Baltic index sliding to a six-month low reinforced negative sentiment and reduced confidence in a near-term recovery. The combined weakness across physical and paper markets eroded pricing discipline on key coal routes, keeping spot rates depressed and capping any upside potential.

“Asia-Pacific Supramax freights largely trended lower amid persistently muted activity in the Pacific basin, with demand towards India remaining particularly subdued. The Indian Ocean market also stayed quiet, as growing tonnage availability along the Indian coast weighed on fundamentals. Meanwhile, bunker prices continued to edge higher, extending gains from the previous session, though this offered limited support to freight levels,” a source informed BigMint.

Another ship-operator noted, “Market conditions remained largely stagnant through the week, with little indication of any near-term improvement in freights.”

Freights on the Australia-India coal routes stayed under pressure as subdued fixing activity and an oversupply of prompt vessels prevented the market from stabilising. Ongoing weakness in India’s steel sector, coupled with comfortable inventory levels, further dampened market sentiment.

In the same vein, Supramax rates on the Indonesia-India route and Panamax freights on the South Africa-India route edged lower over the week, weighed down by limited cargo availability and abundant open tonnage. Fixture activity remained scarce as charterers adopted a wait-and-watch approach.

Rising bunkers squeeze margins, adding strain to weak freight market

Bunker prices moved higher this week, supported by a rebound in crude oil futures and firmer energy market sentiment. The rise in fuel costs pushed up voyage expenses for owners, adding pressure to an already weak dry bulk freight environment. With cargo volumes remaining thin and vessel supply ample, owners found it difficult to pass on higher bunker costs, resulting in further margin compression. Elevated bunkers, combined with subdued fixing activity and cautious chartering interest, weighed on overall sentiment and limited any recovery in vessel freights.

Route-wise updates

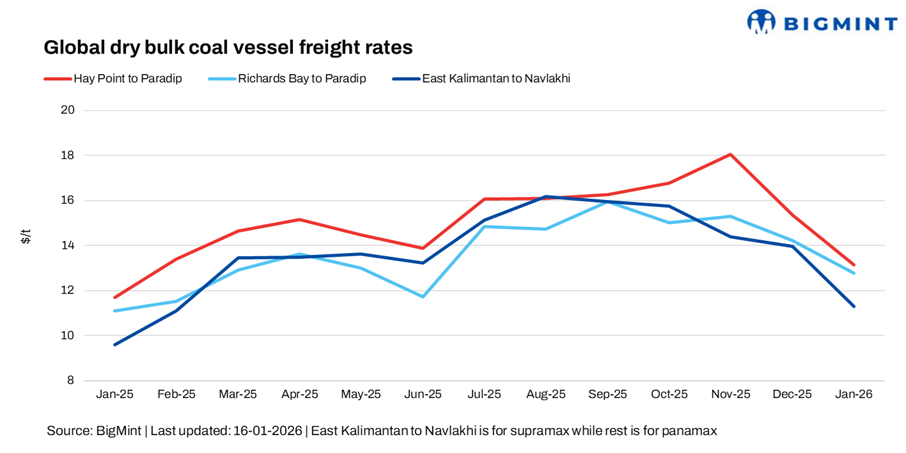

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India edged down marginally by around 0.35/dry metric tonne (dmt) w-o-w to $12.9/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route decreased by $0.36/dmt w-o-w to $12.4/dmt.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route stood at $10.8/dmt, a decrease of $0.21/dmt w-o-w.

Outlook

In the near term, dry bulk coal freights into India are expected to remain under pressure as subdued cargo enquiries, ample vessel availability, and cautious chartering sentiment continue to dominate market fundamentals. Limited fixing activity across the Australia-India, South Africa-India, and Indonesia-India routes suggests the market is still struggling to establish a floor, with comfortable coal inventories and weak downstream demand in India offering little support for a rebound.

While some seasonal improvement in buying interest cannot be ruled out, any recovery is likely to be gradual and uneven. Rising bunker costs may add to owners’ cost burdens, but in the absence of a meaningful pick-up in cargo volumes or disruption to tonnage supply, freights are likely to stay range-bound to soft in the coming weeks, with upside capped and sentiment remaining cautious.

Leave a Reply