- Slowdown post festive season, cyclone impact weigh on fixtures

- Brent crude oil futures climb higher, weigh on vessel demand

India’s seaborne coal freight market remained under pressure this week, with rates declining across the Pacific basin and holding steady in the Atlantic amid persistently weak sentiment. Panamax freights on the Australia-India corridor eased as fixtures were concluded at lower levels, while the South Africa-India route was largely stable due to limited inquiries. Supramax rates on the Indonesia-India route continued to soften amid subdued activity and weak cargo flow. Overall, market sentiment remained cautious, weighed down by sluggish post-festive industrial demand and adequate portside coal inventories at major Indian ports.

“Post-festive sluggishness, coupled with cyclone-related disruptions along India’s east coast, kept trade activity muted. With most buyers having restocked adequate material earlier, procurement remained cautious amid weak industrial consumption and limited near-term demand recovery,” a source said.

Coal freights on the Australia-India route declined, pressured by reduced fixture activity and charterers securing vessels at comparatively lower levels. Weaker cargo demand from Indian buyers, combined with ample tonnage availability, contributed to softer market conditions. Although overall vessel supply remained balanced, limited fresh inquiries and subdued industrial demand continued to weigh on freight sentiment across the corridor.

Freights on the South Africa-India route remained flat amid subdued market activity and limited inquiries on curtailed sponge iron output, keeping sentiment weak. Stable vessel availability and limited fixture interest added to the flat rate environment. Meanwhile, Indian demand for South African coal stayed sluggish, weighed down by a seven-month low in sponge iron production that reduced import requirements from industrial buyers.

Supramax freights on the Indonesia-India route continued to decline, pressured by weak market activity and a shortage of new coal cargo inquiries. “Supramax freights across the Pacific basin trended lower, while bunker prices registered a slight decline during the week,” a source informed BigMint.

Meanwhile, India’s portside thermal coal inventories declined 2.6% w-o-w to 12.98 million tonnes (mnt) in Week 44 (ending 02 November 2025) from 13.33 mnt in Week 43. The drop was mainly attributed to slower vessel arrivals and reduced offtake along the eastern coast following cyclone disruptions, while weak restocking activity kept inventories from recovering at western ports.

Route-wise updates

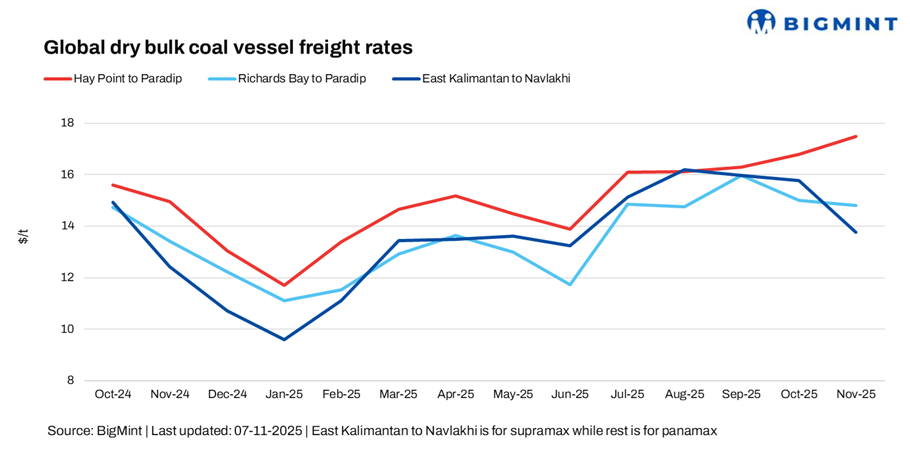

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India edged down by around 0.34/dmt to $17.32/dmt when compared to 30 October 2025.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route remained flat at $14.80/dmt as against 30 October 2025.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route stood at $13.73/dmt, a decrease of $0.7/dmt against 30 October 2025.

Why are dry bulk coal freights under pressure?

- Panamax, Supramax Baltic index falls w-o-w: The Baltic Exchange’s dry bulk index for Panamax and Supramax vessels declined this week, with the Panamax index falling 32 points w-o-w to 1,817 and the Supramax index slipping 24 points to 1,312. The drop was driven by weaker coal and grain demand, ample vessel supply, and limited fresh fixtures. Soft chartering activity and cautious sentiment in the Pacific basin further pressured Panamax and Supramax rates.

- Brent crude oil futures edge higher, weighing on vessel demand: Brent crude oil futures increased by about $0.33/barrel (bbl) w-o-w to $64.07/bbl on 7 November 2025. A modest uptick in oil prices was driven by short-term supply concerns and geopolitical risk, which briefly outweighed demand weakness. US crude inventories rose more than expected, but the market took encouragement from disruptions and tighter supply signals.

Outlook

In the near term, India’s dry bulk coal freight market is expected to remain range-bound, weighed by muted industrial demand and limited import momentum from the power and steel sectors. Although port operations and vessel availability are stable, subdued spot inquiries and cautious procurement are likely to keep rates under pressure, particularly across Indonesia-India and South Africa-India routes.

However, seasonal restocking ahead of winter and steady domestic demand from utilities could lend partial support. Any fluctuations in bunker prices or weather-related disruptions, especially along the east coast, may trigger short-term volatility, but overall sentiment is expected to stay soft through mid-November.

Leave a Reply