- Wide bid-offer spread, firm stances hinder trade activity

- Weakening FFA rates & demand expected to weigh on rates

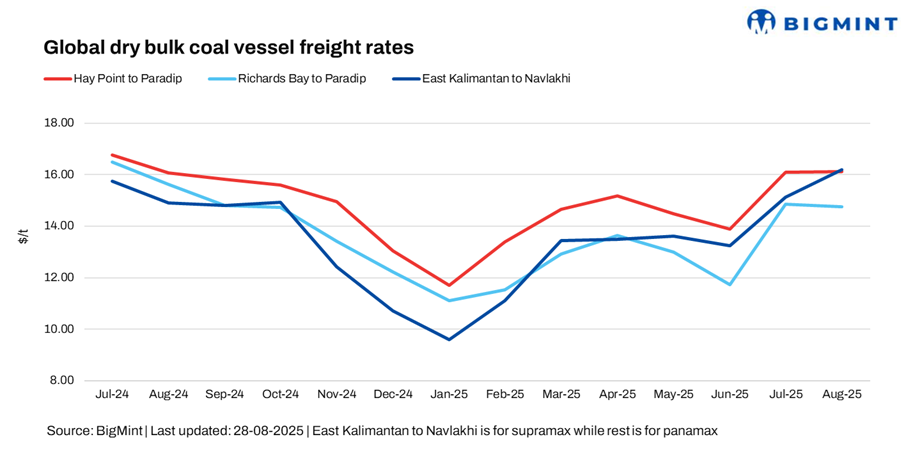

Dry bulk coal freights to India continued to remain firm w-o-w across all key routes – Australia, South Africa, and Indonesia – despite the absence of significant vessel trading activity.

“Asia-Pacific Panamax freight rates climbed, buoyed by sustained Pacific basin sentiment and support from a firm East Coast South America market”, a shipbroker mentioned.

However, trading was largely slow during Asian hours, with participants easing the pace amid bid-offer gaps through the week and showing little urgency to close deals, BigMint observed.

Market activity stayed muted, with buying restricted to need-based procurement. Comfortable stock levels at thermal power plants and stable domestic coal supply curbed the urgency for imports, while cautious industrial demand kept overall coal consumption moderate.

Meanwhile, India’s portside thermal coal inventories fell marginally by 0.6% w-o-w to 13.78 mnt in week 34 from 13.86 mnt in week 33, as weaker port arrivals offset gains at select western and eastern ports.

Route-wise updates

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India rose by around $0.54/dry metric tonne (dmt) w-o-w, with BigMint’s latest assessment placing the Hay Point-Paradip route at $16.54/dmt. Demand from Indian blast furnace operators softened this week, as seasonal monsoon disruptions and the slowdown ahead of upcoming festivals such as Ganesh Chaturthi weighed on trade activity. In the same line, one of the source mentioned, “The market remained firm, though fixtures were limited. Indian brokers and operators are expected to stay out of the market for up to two days during the Ganpati festival.”

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa (Richards Bay) to India (Paradip) route remained firm w-o-w at $15/dmt. Market sentiment stayed weak, with losses curbing trading interest. Uncertain offers and minimal portside bookings, coupled with subdued domestic coal demand, further dampened activity. One of the source told, “Freight derivatives recorded notable gains during Asian hours, while bunker prices held rangebound. From South Africa, fixing activity was largely limited through the session.”. On contrary, a shipbroker said, “Numbers remain high, but the market is slow out of South Africa.”

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia (East Kalimantan) to India (Navlakhi) route stood at $16.95/dmt, a significant increase of $1.02/dmt, w-o-w. “On the Indonesia-India coal route, time-charter rates held firm, though overall trading in the Indian Ocean stayed muted amid limited fresh cargo offerings“, another source mentioned to BigMint.

Market highlights

- Baltic index continue to rise d-o-d: Baltic Exchanges main dry bulk sea freight index continued to head north on 28 August as vessel rates strengthen across the segments. The overall index increased d-o-d by around 5 points to 2,046. Additionally, the Panamax segment also supported the overall index, rising significantly by 56 points d-o-d to 1,874 while the Supramax segment increased by 10 points to around 1,447, d-o-d.

- DCE coal futures up w-o-w: DCE coking coal futures on the Dalian Commodity Exchange (DCE) for the September 2025 contract witnessed uptrend w-o-w by RMB 8/t ($1/t)to RMB 228/t ($32/t) on 28 August. DCE coking coal futures rose this week mainly on improved demand prospects and tighter supply signals. Buying interest picked up as Chinese steel mills prepared to restock ahead of the September-October peak production season, while weather-related mining disruptions and import restrictions tightened availability. Together, these factors supported a firmer outlook and lifted market sentiment.

Outlook

In the near term, dry bulk coal freights are likely to stay range-bound or ease slightly, as muted Asian demand and ample vessel supply weigh on momentum. Market optimism from earlier sessions gradually faded through the week, with freight derivatives sliding during Asian hours and sentiment turning softer. In the Pacific, iron ore and coal demand from operators and traders was marginally lower, as a few cargoes were cleared in the prior session with limited fresh orders emerging.

Leave a Reply