- Baltic dry bulk index heads south

- Near-term outlook turns bearish

Dry bulk coal freights to India saw a w-o-w decline on the Australia and South Africa routes, while Supramax rates on the Indonesia-India corridor continued to hold firm.

Coal demand from operators in the Pacific remained muted, and minimal fresh cargoes entered the market and only a few shipments were cleared overnight, resulting in softer requirements. Trading activity during Asian hours was largely sluggish, sources told BigMint.

Additionally, persistent rainfall across parts of India continued to dampen thermal coal demand, leading to slower vessel booking activity. Most market participants stayed on the sidelines, waiting for either a correction in offers.

Adding to the weak demand sentiment, portside thermal coal inventories in India dropped by 5.3% w-o-w to 14.77 million tonnes (mnt) in Week 30 of 2025, from 15.60 mnt the previous week. The decline was driven by reduced vessel arrivals at major ports due to monsoon-related logistical disruptions.

“Activity remained largely muted in the Pacific basin, with very few fixtures reported. The market was under significant pressure, as several shipowners showed readiness to reduce their offers in order to secure trades, leading to a decline in freights,” a source informed BigMint.

Another source said, “Asia-Pacific Panamax freights eased due to weak market fundamentals, with freight derivatives and oil prices also declining during Asian trading hours, further weighing on sentiment. However, a rise in bunker prices from the previous session provided some support.”

Adding to the ongoing volatility, oil markets remained range-bound, as traders awaited clarity ahead of the 1 August deadline for new US tariffs. Brent crude futures for September eased by 18 cents d-o-d to $73.06 a barrel, while the more liquid October contract dropped 26 cents to $72.21.

Route-wise updates

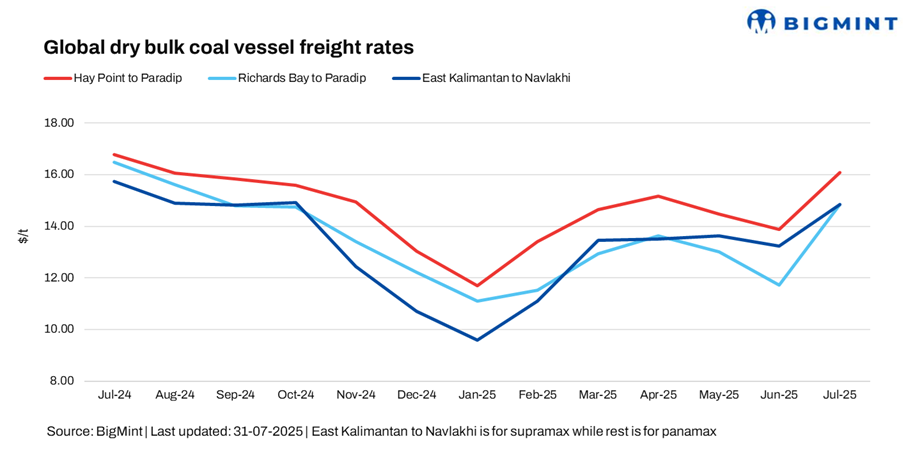

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India decreased by $0.52/dry metric tonne (dmt) w-o-w, with BigMint’s latest assessment placing the Hay Point-Paradip route at $16.30/dmt. Monsoon rains continued to impact several regions of India, disrupting port operations, delaying cargo handling, and tightening vessel turnaround times. The weather-related interruptions led to congestion at select ports, limited loading/discharging windows, and affected freights — particularly for coastal movements. “Indeed, the monsoon continues to play a significant role in shaping the market. Conditions are softening now, and from what I understand, coal imports have slowed due to both the ongoing rains and current import policies. Starting next week, import volumes are expected to decline further and remain low through the end of August,” added a source.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa (Richards Bay) to India (Paradip) route dropped by $0.63/dmt w-o-w to $15.70/dmt. The decline was mainly attributed to a few fixtures concluded at relatively lower offers earlier this week, which weighed on overall freight levels.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia (East Kalimantan) to India (Navlakhi) route rose by $0.23/dmt w-o-w to $16.14/dmt. The uptick was attributed to logistical challenges faced by miners in Kalimantan, stemming from declining water levels that impacted vessel movement, according to sources.

Market highlights

- Baltic dry bulk index heads south d-o-d: The Baltic Exchange’s main dry bulk sea freight index continued its downtrend as demand weakened across vessel segments. The Panamax index dropped by 30 points d-o-d to 1,659. Meanwhile, the Supramax index eased by 3 points d-o-d to 1,268.

- DCE coking coal futures decrease w-o-w: Coking coal futures on the Dalian Commodity Exchange (DCE) decreased significantly by RMB 134/t ($19/t) w-o-w to RMB 1,601/t ($223/t) on 31 July 2025. The slide in DCE coking coal futures reflects a classic surplus-demand mismatch, with ample supply clashing against lacklustre downstream demand and cautious buying.

Outlook

The near-term outlook for the coal freight market remains soft, with demand subdued due to seasonal and logistical factors. In India, ongoing monsoon conditions have slowed coal imports and vessel bookings, particularly on the Indonesia–India and South Africa–India routes. Port congestion and uneven cargo discharge are also contributing to delays, keeping overall freight activity muted.

Additionally, weak spot demand from major Asian buyers and falling Baltic indices are weighing on sentiment across the Panamax and Supramax segments. Although firm coal prices and occasional weather-related disruptions may offer some short-term support, a significant rebound in freight activity is unlikely until post-monsoon or a notable recovery in regional demand emerges.

Leave a Reply