- High bunker prices kept freight rates firm

- However, weak enquiries kept fixing activity limited

Dry bulk coal freight rates to India recorded mixed trends in the week, with marginal rate improvements on select routes supported by firmer bunker prices and stronger sentiment in parts of the Pacific basin. Market direction was largely influenced by vessel positioning, fuel cost trends, and broader dry bulk trade sentiment across key coal export corridors.

Asia-Pacific Panamax freight rates increased w-o-w, supported by improved sentiment in the Pacific basin. The uptick was driven by firmer freight derivatives and stronger charterer bidding to secure vessels ahead of the Lunar New Year holidays, while bunker prices continued to rise d-o-d.

However, activity in the Indian Ocean remained largely subdued, with limited fresh cargo enquiries and weak fixture momentum. Market participation stayed muted as both charterers and owners maintained a cautious approach amid uncertain demand visibility, with only the Australia-India route witnessing three reported vessel fixtures.

Factors supporting coal freight rates:

- Panamax and Supramax segments drive overall Baltic index gains: The Baltic Dry Index rose sharply by 159 points w-o-w to 2,095 as of 12 February 2026, supported by improved cargo demand and stronger fixture activity across key routes. Gains were led by the Panamax segment, which increased by 107 points to 1,766, driven by firmer coal and grain movements, while the Supramax segment climbed 63 points to 1,165, supported by steady minor bulk cargo demand and improved vessel utilisation.

- Higher fuel costs lend support to freight rate sentiment: Rising bunker prices during the week increased overall voyage costs for shipowners, providing underlying support to freight rates across key dry bulk segments. Higher fuel expenses encouraged owners to maintain firmer rate expectations to protect voyage margins, even as fresh cargo enquiries remained moderate. This cost pressure was particularly visible on longer-haul routes, where elevated bunker costs reduced charterers’ willingness to fix vessels aggressively, resulting in cautious negotiations and helping prevent sharp declines in freight rates.

Why coal freight rates might come under pressure?

- Brent crude oil futures drop marginally w-o-w: Brent crude oil futures eased around $0.07/bbl w-o-w to $66.91/bbl for May 2026 contract on 12 February. Crude oil futures edged lower w-o-w mainly due to concerns over softer global oil demand outlook and ample supply availability in the market. Cautious sentiment was also influenced by mixed economic signals from major consuming regions and expectations of stable-to-higher output from key oil-producing countries, which together limited upward price momentum.

- DCE coke futures fall w-o-w: DCE coke coal futures for May 2026 contract fell w-o-w by RMB 16.5/t ($2.39/t) to stand at around RMB 1,698.50/t ($243.75/t). Futures declined w-o-w mainly due to softening downstream steel demand, which reduced procurement appetite for coke. Additionally, adequate coke supply and stable plant operating rates kept market availability comfortable, limiting upward price support. Cautious sentiment in the steel value chain and weak margins at some mills also weighed on prices at the Dalian Commodity Exchange.

Route-wise updates

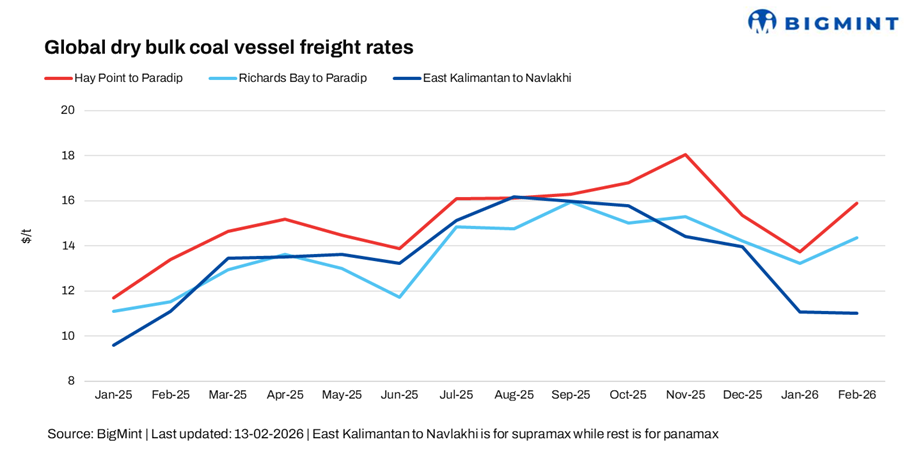

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India edged up marginally by around 0.4/dry metric tonne (dmt) w-o-w to $15.5/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route stood at $14.4/dmt, an increase of around $0.2/dmt, w-o-w.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India continued to remain flat w-o-w at $11/dmt.

Outlook

Coal freight rates to India are expected to remain muted in the near term, supported by firm bunker prices and balanced vessel availability. However, subdued cargo enquiries and cautious procurement by buyers may continue to limit strong upward momentum, keeping fixing activity selective and freight movements dependent mainly on scheduled cargo programmes rather than aggressive spot demand.

Leave a Reply