- Bangladesh demand drives sharp rise in DRI bookings

- Higher global scrap prices shift metallic preference

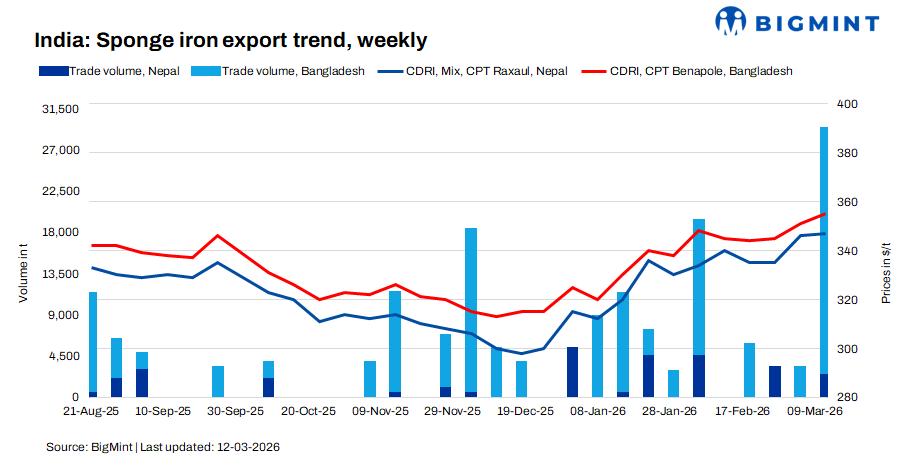

India’s sponge iron (DRI) export market recorded a sharp rise in bookings this week, supported by strong buying interest from Bangladesh as global scrap prices climbed, improving the competitiveness of Indian-origin sponge iron.

Market participants reported a noticeable shift in procurement strategies among Bangladeshi steelmakers, particularly induction furnace and re-rolling mills, as rising scrap prices pushed buyers to explore cost-effective metallic alternatives. Indian sponge iron emerged as a competitive option, allowing mills to optimise their raw material mix and manage steelmaking costs more effectively.

Export booking prices for sponge iron to Bangladesh were heard at around $350-355/t CPT Benapole, translating to roughly $365/t CFR Bangladesh depending on freight and logistics costs. Demand was primarily concentrated among secondary steelmakers seeking prompt shipments to maintain raw material availability.

Meanwhile, export offers to Nepal were reported at around $345-350/t CPT Raxaul for C-DRI(Mix) sponge iron. Demand from Nepal remained comparatively moderate, though a few bookings for pellet-based sponge iron from eastern India were concluded, indicating selective buying interest.

Overall export volumes to Bangladesh and Nepal were estimated at around 29,000 t during the week, marking a significant increase compared with average booking levels in recent weeks. The surge was largely attributed to Bangladesh’s sudden shift toward DRI imports as scrap prices strengthened.

Impact on Indian steel market

The increase in sponge iron exports will influence the domestic steel ecosystem in India, particularly in key sponge iron producing regions such as Raipur, Raigarh, Durgapur, and Rourkela. With higher export bookings absorbing a portion of the available sponge iron supply, domestic availability in some regions may tighten slightly in the short term. This could lead to firming up of sponge iron prices and support domestic market, especially if domestic steel production remains stable.

For induction furnace (IF)-based billet producers, sponge iron remains a critical metallic input. Any diversion of supply toward export markets can intensify procurement competition among domestic buyers. This may gradually push sponge iron prices upward, raising billet production costs and potentially influencing domestic billet and finished steel pricing trends.

Export trend comparison: CY’24 vs CY’25

India’s sponge iron exports recorded notable growth in calendar year 2025. Export volumes rose to 1.61 million tonnes (mnt) in CY’25 (Nepal 1.14 mnt and Bangladesh 0.34 mnt compared with 1.40 mnt in CY’24, reflecting an increase of around 15%.

The growth was supported by demand from neighbouring countries and select Southeast Asian markets, where Indian origin sponge iron remained competitive due to its consistent quality and logistical advantages. Periodic softness in domestic steel demand also encouraged producers to divert surplus material toward export markets, particularly during phases of weaker finished steel offtake.

The growing export momentum highlights the increasing integration of India’s sponge iron market with regional steelmaking supply chains. However, sustained export growth will depend on price competitiveness against alternative metallic inputs such as scrap, as well as steel demand conditions in key importing markets.

Scrap price surge drives demand shift

Imported scrap prices into Bangladesh increased sharply in recent weeks. HMS (80:20) from the UK and EU was heard at around $370-375/t CFR Chattogram, while shredded scrap was indicated at $390-395/t CFR. Plate and structural scrap (PNS) was reported at $400-408/t CFR, with US-origin busheling near $410/t CFR.

Containerised scrap offers rose by around $10-15/t week-on-week, while bulk cargo prices strengthened by approximately $15-30/t amid higher freight costs and tighter supply. The rise pushed average scrap landed costs in Bangladesh close to $400/t CFR, narrowing the cost gap with sponge iron and triggering a shift in raw material preference.

Near term outlook

Market participants believe that DRI export demand from Bangladesh may remain supportive in the near term, particularly if global scrap prices continue to firm up or remain volatile due to freight and supply constraints. However, sustained buying depends on steel demand conditions in Bangladesh and the price competitiveness of Indian sponge iron relative to scrap and other metallic inputs.

Leave a Reply