- Domestic aluminium prices rise despite ample supply

- Mozal smelter shutdown tightens global aluminium supply

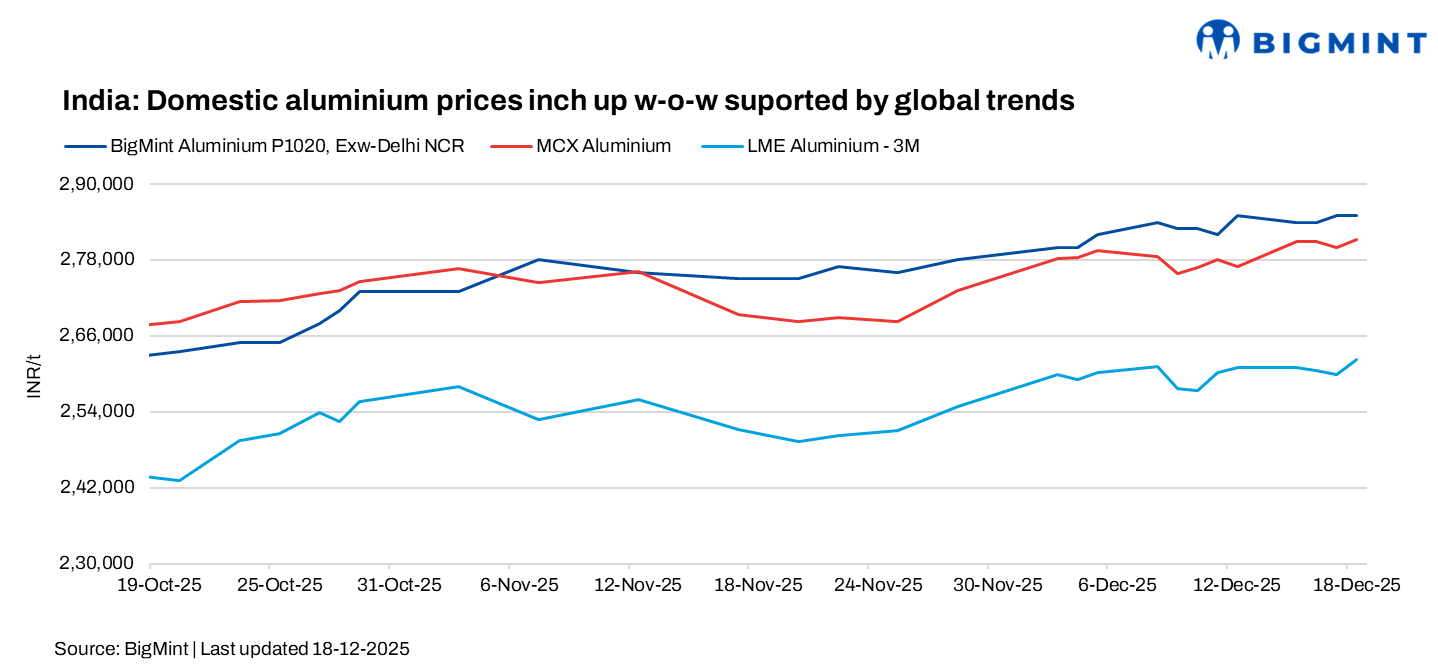

India’s domestic aluminium market recorded modest week-on-week gains, driven by price revisions from primary producers in line with a firmer LME price and renewed global supply concerns. The increase came despite comfortable domestic availability and only a gradual pickup in downstream demand, indicating that global cues played a larger role in shaping prices during the week.

BigMint’s assessment showed India’s domestic P1020 ingot (99.7%) prices rising by INR 3,000/t w-o-w to INR 285,000/t ex-Delhi NCR, while Mumbai ex-works prices gained by INR 4,000/t to INR 286,000/t amid firm global market cues.

How did Indian and global exchanges perform?

Domestic aluminium futures on the MCX gained momentum during the week, rising from INR 278,150/t on 11 December to INR 281,400/t on 18 December, a gain of INR 3,250/t (around 1%). The uptrend reflected firmer underlying physical market conditions, with improved spot demand and higher regional prices lending support rather than speculative positioning alone.

On the global front, LME aluminium prices rose by $20/t w-o-w to $2,905/t, supported by a positive macro backdrop and sustained buying interest. LME warehouse stocks edged up marginally by 850 t to 519,600 t, but inventories remain relatively low in a broader context, continuing to underpin prices. Firm domestic spot prices and positive international cues together drove the weekly gains on MCX, keeping aluminium prices on a firmer footing through the week.

Domestic aluminium prices revise prices amid firm sentiment, steady production

The rise in domestic ingot prices mirrored the price revisions announced by primary producers during the week. BALCO lowered its P1020 price from INR 306,000/t on 12 December to INR 304,250/t on 13 December, while Hindalco reduced prices from INR 304,500/t on 12 December to INR 303,000/t on 13 December, before raising them back to INR 304,500/t by 17 December, reflecting a cautious but firm pricing approach amid improving market sentiment. NALCO left its published P1020 price unchanged at INR 296,000/t.

Market participants reported domestic premiums in the Delhi NCR region at $250-260/t above LME cash largely steady compared to last week.

Although demand has begun to pick up in select segments, the domestic market remains well supplied. A key primary producer continues to hold substantial inventory levels, ensuring ample material availability across the market. As a result, the recent price firmness appears to be driven more by supportive global cues than by a broad-based improvement in domestic consumption.

Despite raw material volatility, India’s primary aluminium production remained strong. Output in 9MCY’25 increased by 10% y-o-y to 3.44 mnt, up from 3.13 mnt in the same period last year.

Global aluminium sentiment improves amid tightening supply

Japan aluminium premiums under the P1020A QMJP CIF Japan are expected to rebound sharply in Q1 2026 from Q4 lows, with settlements likely in the $150-175/t range, centered around $160-165/t, driven by tightening Asian supply and inventory drawdowns. Upside may be capped toward late Q1 due to Japan’s fiscal year-end constraints, but structural tightness could support further gains in Q2.

Meanwhile, South32’s planned care-and-maintenance of the Mozal smelter from March 2026 is set to tighten global supply especially in Europe pushing premiums higher and increasing competition for Asian units. This is expected to lend additional support to Japanese premiums, reinforcing a firmer premium environment despite mixed demand signals.

Outlook

India’s aluminium prices are expected to remain supported through the course of December, backed by firm LME prices, tightening global supply conditions, and steady domestic premiums. While demand is improving gradually, comfortable inventories are likely to keep the market broadly balanced. Looking ahead into 2026, ongoing risks from smelter disruptions and power-related constraints may continue to underpin prices, although the return of curtailed capacity and easing supply-side issues could limit upside and keep prices rangebound over the medium term.

Leave a Reply