- Domestic premiums edge higher as primary prices rise

- US Fed rate cut strengthens global sentiment

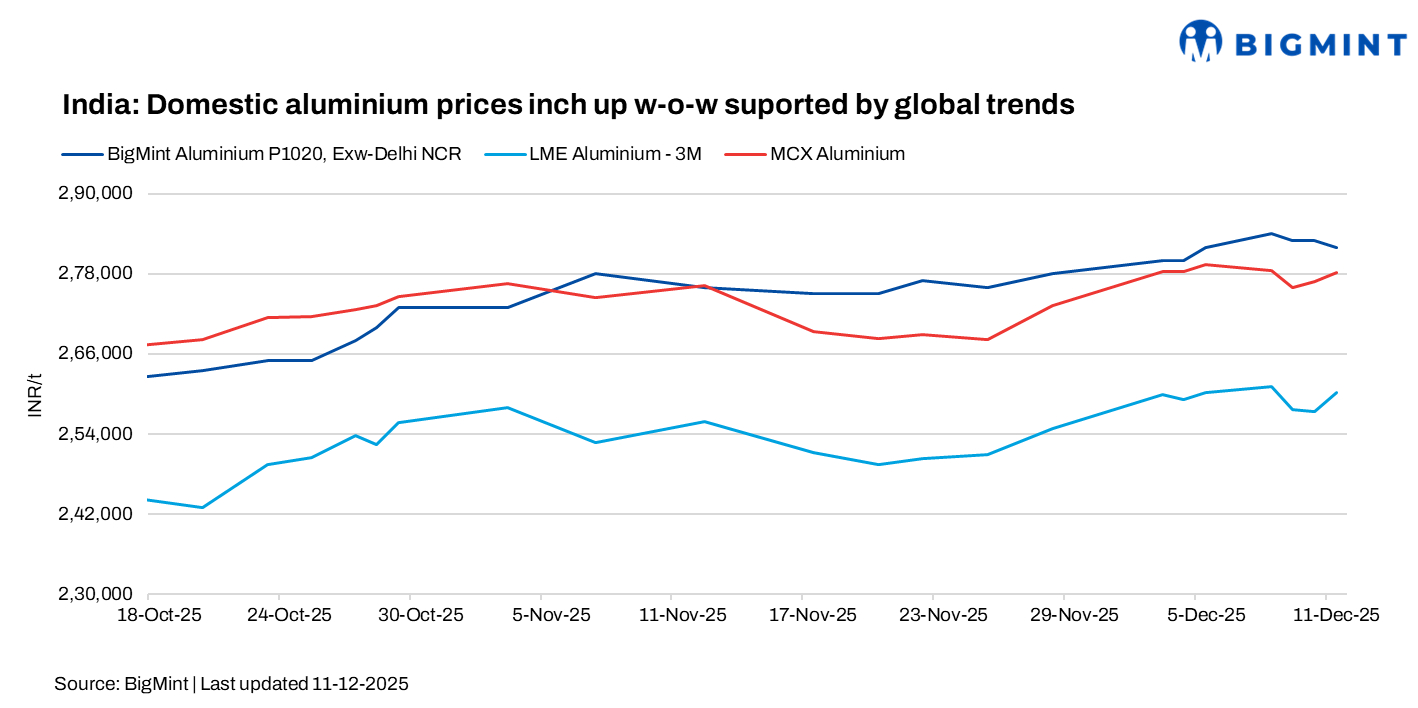

India’s domestic aluminium market posted mild gains w-o-w as primary producers adjusted prices in response to a stronger LME complex and renewed supply concerns abroad. The uptick came despite a well-supplied domestic market and only a gradual improvement in downstream demand.

BigMint’s assessment showed India’s domestic P1020 ingot (99.7%) prices rising by INR 2,000/t w-o-w to INR 282,000/t ex-Delhi NCR, while Mumbai ex-works prices eased by INR 2,000/t to INR 281,000/t, reflecting a mixed regional trend amid firm global market cues.

How did Indian and global exchanges perform?

Domestic futures on MCX held largely stable through the week, easing marginally from INR 278,400/t on 4 December to INR 278,150/t on 11 December. The steady trend indicated that the physical market, rather than the futures curve, drove most of the weekly sentiment.

On the LME, aluminium prices inched up by $10/t w-o-w to $2,875/t as tightening exchange inventories supported the forward curve. LME stocks fell by 7,600 t to 523,300 t, signalling a gradual drawdown that continues to underpin price expectations. A 25 bps US Fed rate cut further strengthened the global outlook by softening the dollar and improving risk appetite.

Domestic producers adjust prices amid steady output

The rise in domestic ingot prices aligned with upward revisions announced earlier in the week by Hindalco and BALCO. Hindalco raised its P1020 price by INR 2,500/t before rolling back INR 1,000/t by 11 December. BALCO increased its P1020 price by INR 1,750/t. NALCO left its published P1020 price unchanged at INR 296,000/t.

Market participants reported domestic premiums in Delhi NCR at $260-265/t above LME cash, up from last week’s $250-255/t. Traders attributed the marginal rise to firmer buying interest rather than any tightening of supply.

While demand is improving in pockets, the market remains comfortably supplied. One primary producer is holding sizeable inventories, which continues to keep domestic availability ample. The current upward trend therefore remains more aligned with global sentiment than with domestic consumption patterns. India’s primary aluminium output remained strong, rising 10 percent y-o-y to 3.44 mnt in 9MCY’25.

Global market sentiment firm despite seasonal slowdown

Across the US and Europe, demand held firm through November but is expected to moderate due to the year-end slowdown. Supply risks, however, remain elevated. The Iceland smelter closure and uncertainty over the Mozal smelter’s power arrangements continue to cloud the supply outlook, potentially tightening availability if disruptions extend.

Japanese premiums for Q1 2026 are forecast in the $140-203/t range, with current negotiations indicating offers of $190-203/t–significantly higher than the $86/t settled for Q4 2025. The steep rise reflects tighter global availability, higher overseas premiums, the Iceland outage, potential Mozal cutbacks, US tariffs, and stockpiling linked to the EU’s carbon-tax framework.

In the US, domestic premiums have surged to record highs, with last heard levels near $1,950/t above LME. The premium strength is driven by low domestic inventories, though weakening end-use demand may prompt adjustments through quotas or bilateral arrangements.

European premiums have rebounded, supported by pre-CBAM stockpiling and lingering supply concerns. Market levels recently hovered between $340-348/t over LME.

Outlook

Indian aluminium prices are expected to remain firm in December, supported by strong LME prices and elevated domestic premiums. Although demand is improving gradually, high inventories ensure a balanced market. Looking to 2026, persistent global supply risks may keep LME prices supported, though any resolution of outages and power-related disruptions could soften prices toward $2,500/t.

Leave a Reply