- LME aluminium climbed amid supply-side disruptions

- Delhi NCR premiums steady at $240-250/t

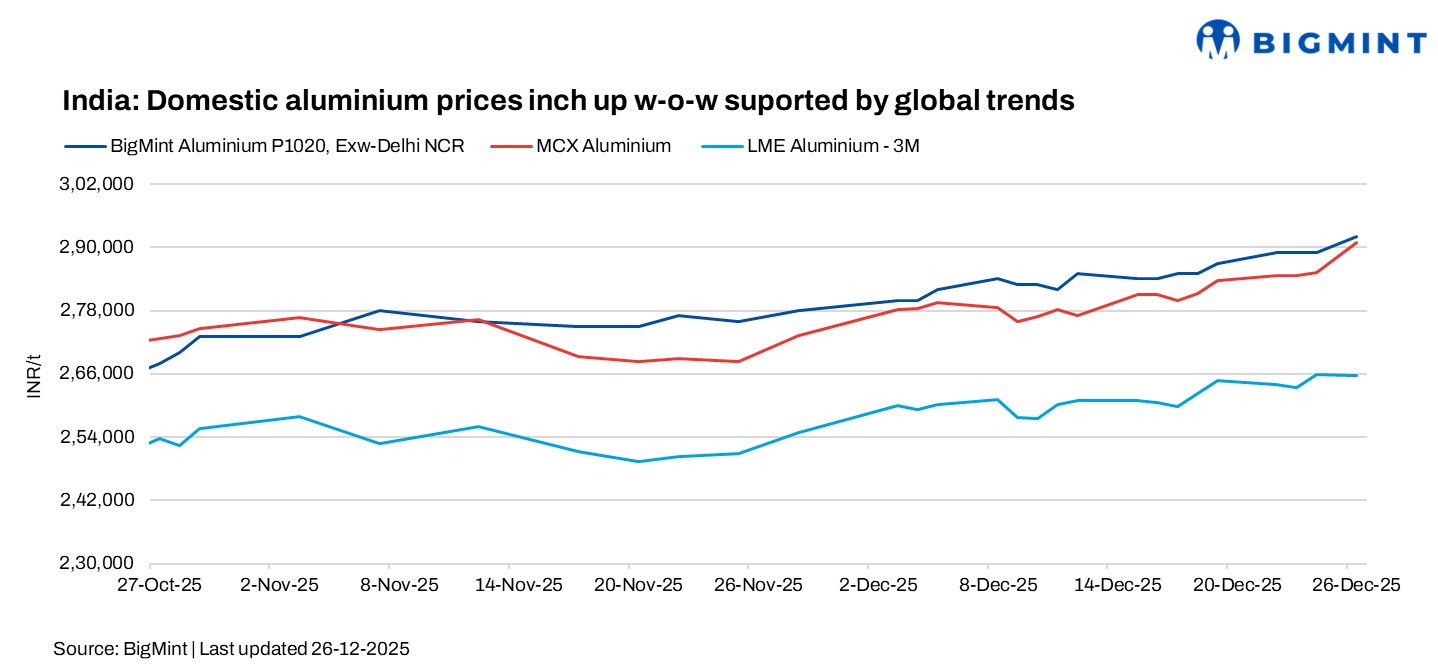

India’s domestic aluminium prices recorded notable week-on-week gains, supported by upward price revisions from primary producers following a rise in LME and MCX aluminium prices and renewed global supply concerns. The increase came despite comfortable domestic availability and only a gradual improvement in downstream demand, underscoring the dominant influence of global market cues on prices during the week.

BigMint’s assessment showed India’s domestic P1020 ingot (99.7%) prices rising by INR 5,000/t w-o-w to INR 292,000/t ex-Delhi NCR, while Mumbai ex-works prices gained by INR 12,000/t to INR 301,000/t amid firm global market cues.

How did Indian and global exchanges perform?

Domestic aluminium futures on the MCX strengthened through the week, rising from INR 283,700/t on 19 December to INR 290,900/t on 26 December, a gain of INR 7,200/t (around 2.5%). The uptrend reflected firmer underlying physical market conditions, with steady spot demand and higher regional prices providing support rather than speculative positioning alone.

On the global front, LME aluminium 3-month prices rose by around 2.2%, climbing from about $2,896/t on 18 December to $2961/t on 23 December, underpinned by tight supply concerns and robust buying interest. The upward momentum was driven largely by global supply-side disruptions, including the confirmed plan to place Mozambique’s Mozal aluminium smelter under care and maintenance by March 2026 due to unresolved power supply issues — a development expected to tighten global output and exacerbate supply constraints.

Additional production setbacks at key facilities, such as equipment failures at European smelters and broader energy-related challenges, have further intensified supply pressure and supported elevated prices.

Meanwhile, LME warehouse stocks remained relatively stable at around 519,600 t, but in the broader context inventories are viewed as tight, continuing to underpin prices. Together, firm domestic spot trends and sustained global supply concerns helped keep MCX aluminium prices on a strong footing through the week.

Domestic aluminium prices revised upward amid firm market sentiment

The rise in domestic ingot prices reflected successive price revisions by primary producers during the week. BALCO raised its P1020 price from INR 307,000/t on 20 December to INR 308,750/t on 24 December, before further increasing it to INR 314,000/t on 25 December, indicating a firmer pricing stance. Hindalco adjusted prices more gradually, lowering its P1020 price from INR 309,250/t on 20 December to INR 307,250/t on 23 December, before hiking it to INR 310,750/t on 24 December and INR 312,500/t on 25 December, reflecting a cautious but supportive approach amid improving market sentiment.

Market participants reported domestic premiums in the Delhi NCR region at $240-250/t above LME cash, largely steady compared to the previous week.

Buying activity has shown a slight slowdown as the year draws to a close, with market participants adopting a cautious approach amid the typical year-end uncertainties. Seasonal factors, including inventory adjustments, accounting closures, and reduced trading volumes, have contributed to more restrained purchasing, even as underlying demand fundamentals remain intact.

Global aluminium premiums rise as supply tightens and China’s imports dip

Global aluminium producers have proposed higher Q1 premiums for shipments to Japanese buyers, offering around $190-$203/t over the LME cash price for January-March, up roughly 120-135% from the previous quarter’s agreed premium of about $86/t. Japan’s quarterly premium is a key regional benchmark, and the sharp rise in offers reflects tightening supply expectations and stronger demand signals in the Asian market.

China’s net primary aluminium imports fell below 100,000 t in November, dropping to around 94,000 t, a 58.1% month-on-month and 28.9% year-on-year decline. Primary aluminium imports were down sharply while exports jumped to a three‑year high, reflecting weaker import margins and high ingot premiums in Europe and the US that attracted flows away from China. The data suggests that China’s net import levels may remain subdued in the near term compared with earlier months of 2025.

Outlook

India’s aluminium prices are expected to stay supported in the near term, driven by firm LME and MCX prices, tightening global supply, and steady domestic premiums. While domestic demand is gradually improving, healthy inventories should keep the market broadly balanced. Looking into early 2026, ongoing risks from smelter shutdowns, energy constraints, and global supply disruptions are likely to underpin prices, although the resumption of curtailed capacity and easing supply-side pressures may temper gains and keep prices relatively rangebound over the medium term.

Leave a Reply