- CR busheling scrap prices surge in Jan 2026

- Raw material price hikes boosted auction bid prices

Prices in CR busheling scrap auctions climbed impressively across key markets in January, led by the western region’s standout performance driven by high OEM engagement a 6-10% hike m-o-m. Notable 7-8% m-o-m increases in eastern and northern region auctions highlight a thriving supply-demand balance for secondary steel makers.

Price trend

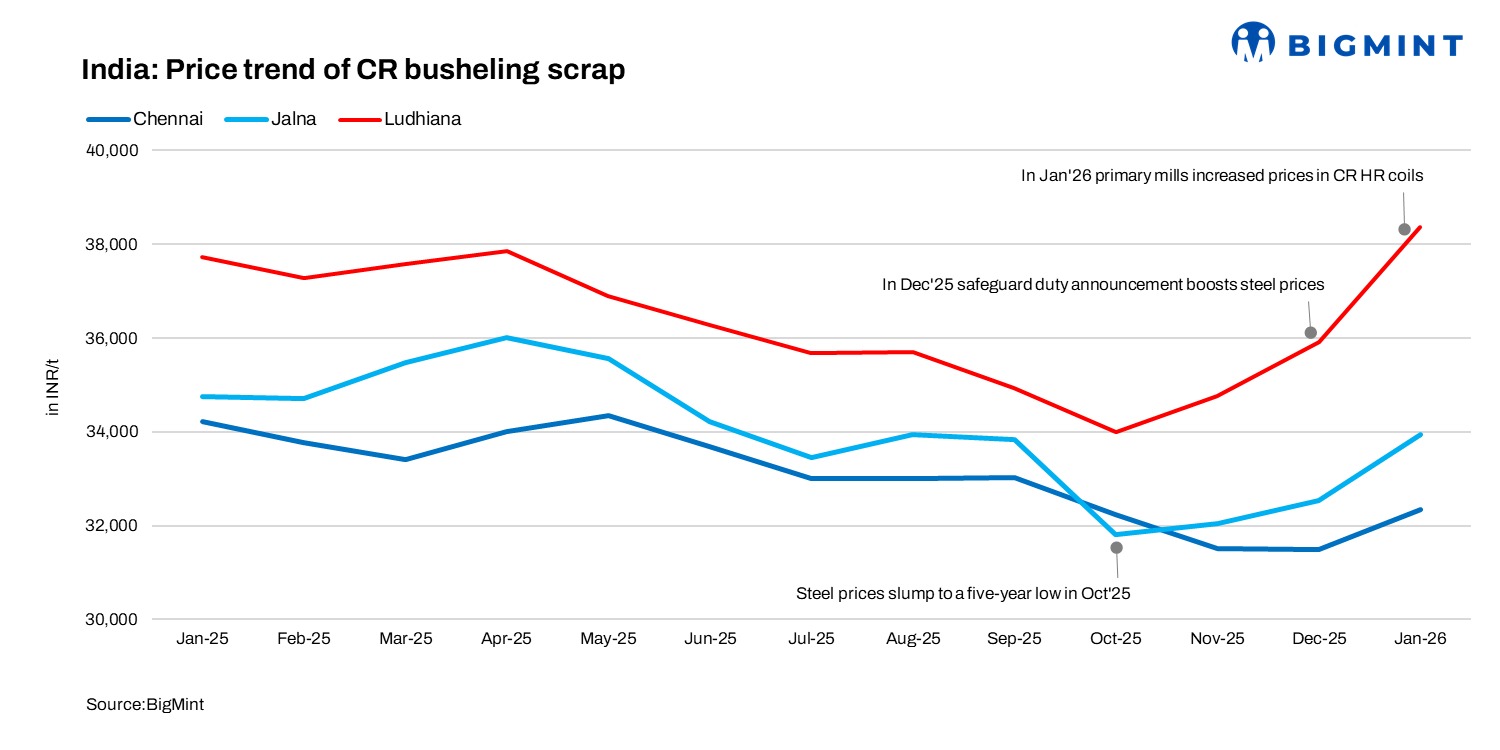

CR busheling scrap prices strengthened m-o-m across key Indian markets, driven by steady mill demand and higher raw material costs. In Ludhiana, Punjab, prices surged by INR 2,450/t to INR 38,369/t, while Jalna, Maharashtra, recorded a rise of INR 1,430/t to INR 33,950/t. Chennai, Tamil Nadu, also saw firm gains, with busheling prices up INR 850/t to INR 32,352/t DAP, reflecting resilient regional buying interest.

HRC, CRC trends

On a m-o-m basis, BigMint’s benchmark assessment for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) climbed by INR 4,900/t to INR 52,000/t in January 2026 against INR 47,100/t in December 2025. Similarly, monthly average of CRCs (IS2062, Gr E250, 2.5-8 mm/CTL) prices rose by INR 3,300/t to INR 57,800/t against INR 54,500/t in the same period. HRC trade-level prices rose m-o-m, driven by mill price hikes, higher raw material costs and tight supply, while demand remained steady.

Domestic Vs Imported scrap

Imported CR-busheling arriving at Kandla and Mundra was assessed at CFR $383-385/t, equivalent to INR 34,730-34,900/t. After adding duties and inland freight, the delivered cost to Ludhiana and Mandi rose to INR 38,730-38,900/t. With domestic material available around INR 38,300-38,700/t DAP, the import-to-domestic price spread kept import bookings limited. Mills continued to prefer domestic scrap, reinforcing weak import demand into the prime-scrap segment.

About foundry scrap market

Foundry scrap prices across India strengthened m-o-m, supported by steady end-user demand from automotive and engineering casting segments. The uptrend remained gradual and need-based, with buyers largely avoiding aggressive inventory build-up. Price momentum was more visible in western and southern India, in line with improving sentiment and controlled scrap availability, while the eastern markets stayed largely stable. Foundry scrap prices will likely stay firm short-term on sustained auto and agricultural demand. Gains are constrained without reduced availability or stronger orders, as buyers maintain tight inventories.

Upcoming scrap auctions

Scrap supply outlook for Feb-March

CR busheling availability is expected to remain stable through February and March 2026, supported by robust auction volumes from OEMs resuming routine schedules following late December 2025 maintenance shutdowns at select tier-1 mills. Post-budget in early February, auto sector demand continues to strengthen, driven by government policies offering up to 50% road tax discounts on new vehicles, which are attracting local consumers from January to February 2026. This momentum is projected to sustain robust demand in the coming months.

Leave a Reply