- Northern auctions record the strongest month-on-month gains

- Western market sees mild corrections amid steady scrap flow

- Import parity weakens as domestic CR-busheling remains more competitive

November market overview

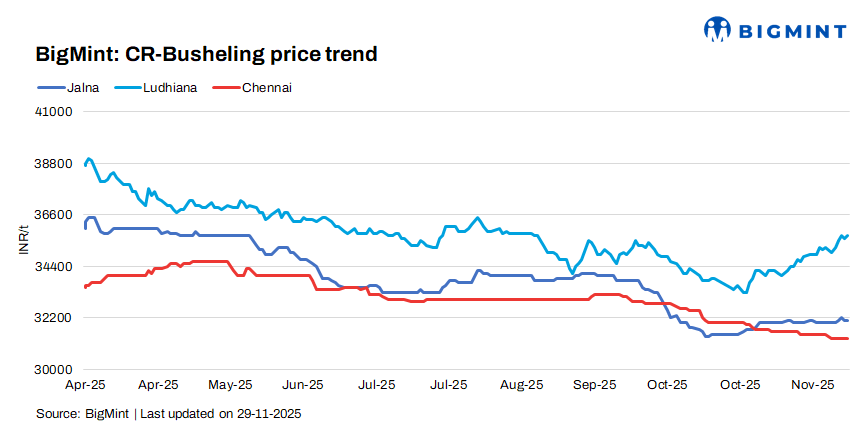

India’s CR-busheling auction markets were mixed in November 2025 as Western clusters faced marginal price corrections while Northern centres reported stronger month-end momentum. Auctions across Pune’s Chakan clusters fell between 1-5% amid comfortable prompt-scrap availability and cautious mill buying, although a few OEM lots achieved small premiums on stable downstream demand. Nasik prices softened as mills limited active bidding. In contrast, the Northern Region outperformed, driven by tighter supply and stronger procurement appetite, with Gurugram recording a month-on-month gain of 7.9% on higher generation from major four-wheeler OEMs.

How Western auction prices aligned with BigMint assessments

Pune and Nasik-key hubs for CR-busheling generation from automotive and white-goods manufacturing-continued to supply the bulk of prompt scrap to Kolhapur and Jalna. In Week 40, BigMint assessed Jalna’s CR-busheling average at INR 32,000/t DAP. During the same period, a major OEM in Pune closed 5,000-6,000 t of Mixed and Zn-coated CR-busheling auctions at INR 30,000-30,600/t ex-works. After adjusting for freight to Jalna at INR 1,100-1,300/t and supplier commission, the landed cost worked out to roughly INR 31,900/t, closely matching the assessed Jalna trade level.

Low-manganese, non-coated CR-busheling consumed in Kolhapur’s foundry belt traded around INR 35,000/t ex-works. Once freight, processing charges and commission were added, the landed cost rose to INR 37,500-38,000/t DAP. BigMint’s Kolhapur assessment at INR 39,000-39,500/t remained higher due to the prevalent 30-day credit terms, while immediate-payment deals continued to clear at INR 38,500-39,000/t.

Northern Region auctions command higher premiums

Two key auctions in the final week of November supported a stronger pricing trend. A leading OEM in Gurugram sold 7,100 t of low-manganese CR-busheling under a 45-day lifting window at INR 34,100/t ex-works, while another OEM in Uttarakhand closed 1,000 t at INR 33,500/t. Both lots recorded higher bids compared with October as mills in Ludhiana stepped up procurement.

With BigMint’s Ludhiana assessment at INR 35,500-36,000/t DAP, the auction-to-market parity remained tight. Factoring in freight and commission of about INR 1,700/t, the landed cost of auction material ranged between INR 35,200-35,700/t DAP, nearly matching regional index levels and indicating balanced demand.

Finished steel trends shape mill procurement behaviour

In Jalna, billet sales into the merchant market remained limited as most large producers focused on captive rolling. While billet offers strengthened marginally late in the month, rebar prices increased only INR 200-300/t, narrowing conversion margins and restricting mills from raising scrap bids.

Northern markets, especially Mandi Gobindgarh, witnessed stronger finished steel movement. Billet and TMT prices rose by INR 700-1,000/t as tighter melting scrap availability lifted production costs. Higher billet inflows from neighbouring states and a mild improvement in downstream demand further supported price gains, prompting mills to stay active in sourcing prime scrap.

Scrap supply outlook for December-January

CR-busheling availability is expected to remain stable through December as most OEM auctions for the month have concluded and lifting has commenced. However, scheduled maintenance shutdowns at select Tier-1 mills in the third week of December may reduce generation in early January, potentially tightening supply for a brief period.

Domestic scrap remains cheaper than imports

Imported CR-busheling arriving at Kandla and Mundra was offered at CNF $ 363-365/t, equivalent to INR 32,600-32,800/t. After adding duties and inland freight, the delivered cost to Ludhiana and Mandi rose to INR 36,500-37,000/t. With domestic material available around INR 36,000/t DAP, the import-to-domestic price spread kept import bookings limited. Mills continued to prefer domestic supply, reinforcing weak import demand into the prime-scrap segment.

Leave a Reply